Net Worth Update - March 2014

While cash flow is more important when it comes to financial independence, it's still good to look at the balance sheet too, which is why I provide these net worth updates. The S&P 500 was essentially flat for the month with just a 0.6% increase. Since more and more of my net worth is tied to the markets, there's a larger between my net worth and the markets. As a dividend growth investor I'm not overly concerned with the short-term gyrations as long as the dividend stream remains in tact, but the markets' effect is noticeable. I had just over $7,000 in after-tax savings from my paycheck (although only $5k is directly earmarked for savings), around $1,100 in ESPP contributions, and just over $800 in 401k contributions counting the employer match. The rest of the changes were due to dividends received and changes in the stock market. All in all March saw a $9,537.14 increase in my net worth.

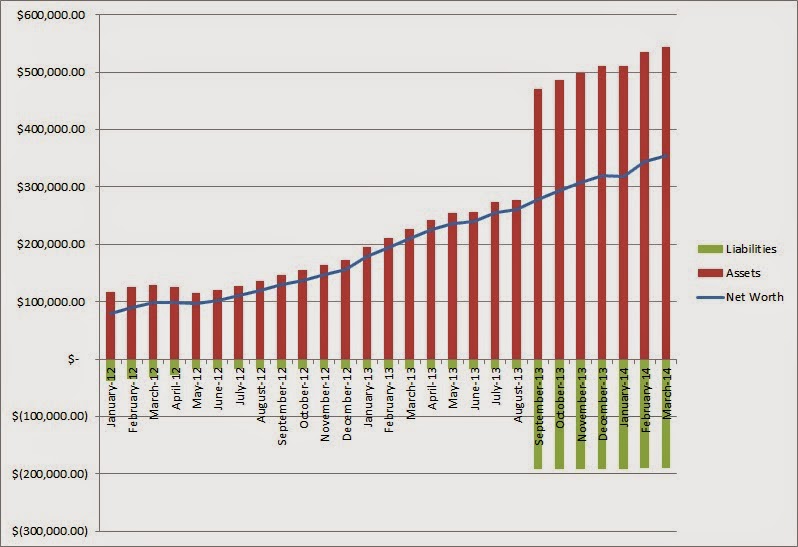

Current Assets: $544,686.37

Curent Liquid Assets: $170,272.80

Current Debts: -$190,442.76

Net Worth: $354,243.61

My monthly changes have been all over the place to start the year with a decline in January followed by a $25k+ increase in February. Well, March ended up in the middle and around where I'd expect most months to end up, although a bit on the low side. It's pretty crazy to see that my assets are approaching $550k, especially since they were only around $120k back in January 2012. I know that our house has something to do with the big jump in assets, but the liquid assets, i.e. investments, have made a big improvement over that time as well. Liabilities mainly consist of the mortgage on our house so very little progress gets made in decreasing the total liabilities. For now I don't see the point in paying extra on the mortgage given our relatively low interest rate. I think we'll come out much further ahead investing the difference and then once we're close to FI make the decision of whether to aggressively pay down the mortgage to be completely debt free. We now have 20.61% equity in our house.

March's increase came in at a 2.77% improvement over February and year-to-date I've had an increase of $34,129.39 for a 10.66% improvement. My goal for the year is to have a $125,000 increase in my net worth, and so far I'm 27% of the way towards my goal and on track to get there. Of course, there's no telling what the investment assets will do towards my progress towards that goal.

I've changed the chart for my net worth to better reflect our situation now that there's significant debt on the books with our mortgage. The chart will now show both assets and liabilities as well as the net worth.

My after-tax savings rate for March came in at 54.46% which is over my goal of 50%, so I'll be looking to increase that target during my quarterly review post. This is a big drop-off from 2013's 81.31% rate, but that's because I changed the way I calculate my savings rate. It's now just savings from my after-tax income that is specifically marked for investment. I think this gives a purer savings rate since it's only true savings/investment capital.

It's great to see a new trend forming in my liquid assets expense coverage after the 3 month decline towards the end of 2013. I've got a new streak going with 2 consecutive months of increases and I hope to keep that up throughout the rest of the year. As expenses hopefully head lower and savings move higher this ratio should continue to increase in most months. Based on my expenses from March, my liquid savings would last for 5.33 years.

I've updated my Progress page to reflect March's changes.

Also, I'm starting a newsletter and I hope to get the first edition out over the next week or two so go on and sign up to receive new posts to your email and newsletter! Also you'll be the first to hear about new things that I have in store for the blog.

How did your net worth do in March?

Current Assets: $544,686.37

Curent Liquid Assets: $170,272.80

Current Debts: -$190,442.76

Net Worth: $354,243.61

My monthly changes have been all over the place to start the year with a decline in January followed by a $25k+ increase in February. Well, March ended up in the middle and around where I'd expect most months to end up, although a bit on the low side. It's pretty crazy to see that my assets are approaching $550k, especially since they were only around $120k back in January 2012. I know that our house has something to do with the big jump in assets, but the liquid assets, i.e. investments, have made a big improvement over that time as well. Liabilities mainly consist of the mortgage on our house so very little progress gets made in decreasing the total liabilities. For now I don't see the point in paying extra on the mortgage given our relatively low interest rate. I think we'll come out much further ahead investing the difference and then once we're close to FI make the decision of whether to aggressively pay down the mortgage to be completely debt free. We now have 20.61% equity in our house.

March's increase came in at a 2.77% improvement over February and year-to-date I've had an increase of $34,129.39 for a 10.66% improvement. My goal for the year is to have a $125,000 increase in my net worth, and so far I'm 27% of the way towards my goal and on track to get there. Of course, there's no telling what the investment assets will do towards my progress towards that goal.

I've changed the chart for my net worth to better reflect our situation now that there's significant debt on the books with our mortgage. The chart will now show both assets and liabilities as well as the net worth.

My after-tax savings rate for March came in at 54.46% which is over my goal of 50%, so I'll be looking to increase that target during my quarterly review post. This is a big drop-off from 2013's 81.31% rate, but that's because I changed the way I calculate my savings rate. It's now just savings from my after-tax income that is specifically marked for investment. I think this gives a purer savings rate since it's only true savings/investment capital.

It's great to see a new trend forming in my liquid assets expense coverage after the 3 month decline towards the end of 2013. I've got a new streak going with 2 consecutive months of increases and I hope to keep that up throughout the rest of the year. As expenses hopefully head lower and savings move higher this ratio should continue to increase in most months. Based on my expenses from March, my liquid savings would last for 5.33 years.

Also, I'm starting a newsletter and I hope to get the first edition out over the next week or two so go on and sign up to receive new posts to your email and newsletter! Also you'll be the first to hear about new things that I have in store for the blog.

How did your net worth do in March?

Nice work - the UK markets were down in March so I took a little bit of a beating in comparison - my first negative month work almost a year!

ReplyDeleteI agree with overpaying the mortgage. Any interest payments below 4% would be covered by dividend income, meaning any long term gains in the market would effectively be profit.

Good to see your progress against the annual goal - keep it up!!

moneystepper,

DeleteThe markets were essentially flat here but since I save a good amount each month I can counteract, at least partially, some of the downward movements. Our rate on our mortgage isn't quite that good but it's still at a point where I don't see an overwhelming need to pay it down as quickly as possible.

Thanks for stopping by!

Good stuff, JC. Thats a great savings rate for the month. I am approximately at the same rate myself.

ReplyDeleteLooking forward to reading your newsletter.

best wishes

Roadmap,

DeleteI really hope to get the savings rate increased up a bit from here and once some of the travel dies down I should really start to hit my stride. Especially if I can couple that with lowering my expenses some. I've got a trip to Vegas coming up next month, then most likely a road trip somewhere with my wife in July. We're not quite sure where we're wanting to go yet but we were thinking possibly making the drive from SF to Portland to get a view of the west coast. I've never been over there but that drive is supposed to be pretty awesome.

Thanks for stopping by!

Pursuit,

ReplyDeleteWhat can I say? You're a machine, my man!

Keep it up. Your pursuit for passive income is a real pleasure to watch, and I know I'm inspired!

Best regards!

DM,

DeleteI just try to do my part which is continually save a large percentage of my income. The investments will take care of themselves over the long-run so I don't ever get worried about lower than normal net worth growth or gasp, even a decline.

Thanks for stopping by and for the kind words!

Looks great Pursuit...I feel your pain with the mortgage debt. Our family owes approx. $350K but our net worth is near $900K. And even though our net worth is almost triple our mortgage, I still wished it didn't exist. :)

ReplyDeleteA Frugal Family's Journey,

DeleteIf I could I'd get rid of the mortgage but I just don't see the benefit right now. It'd only free up an extra $1k in capital to invest once the mortgage was paid off and our interest rate is low enough that over 5-7 years we should be able to easily beat that rate from dividends/capital gains. We're still far enough away from FI that that remains our main priority. Plus if we build up our passive income stream enough to cover the mortgage as well and then pay off the mortgage that's an extra $1k per month in income we can use.

Thanks for stopping by!