Phillip Morris (PM) Dividend Stock Analysis

I'm surprised I haven't posted an analysis on Phillip Morris yet, but somehow it's slipped through the cracks. Phillip Morris is only a dividend challenger, but going back to the days of being part of the beast that included Kraft and Altria, the culture of increasing dividends is in place. And we can't really fault them for increasing the dividend every year since being spun off in 2008. Phillip Morris closed trading on June 26th at $87.54.

Company Background (sourced from Yahoo! Finance):

Philip Morris International Inc., through its subsidiaries, manufactures and sells cigarettes and other tobacco products. The company’s portfolio of international and local brands include Marlboro, Merit, Parliament, Virginia Slims, L&M, Chesterfield, Bond Street, Lark, Muratti, Next, Philip Morris, and Red & White. It also owns various local cigarette brands, such as Sampoerna, Dji Sam Soe, and U Mild in Indonesia; Fortune, Champion, and Hope in the Philippines; Diana in Italy; Optima and Apollo-Soyuz in Russia; Morven Gold in Pakistan; Boston in Colombia; Belmont, Canadian Classics, and Number 7 in Canada; Best and Classic in Serbia; f6 in Germany; Delicados in Mexico; Assos in Greece; and Petra in the Czech Republic and Slovakia. The company sells its products in approximately 180 countries in the European Union, Eastern Europe, the Middle East, Africa, Asia, Latin America, and Canada.

DCF Valuation:

Analysts expect Phillip Morris to grow earnings 11.23% per year for the next five years and I've assumed they can continue to grow at 3.50% per year thereafter. Running these numbers through a two stage DCF analysis with a 10% discount rate yields a fair value price of $116.97. This means the shares are trading at a 25.2% discount to the DCF.

Graham Number:

The Graham Number valuation method offers no value in Phillip Morris' case since the book value per share is negative. Due to this I will just ignore the Graham Number in my calculations, although it is something to keep in mind.

Average High Dividend Yield:

Phillip Morris' average high dividend yield for the past 3 years is 4.50% and for the past 6 years is 4.97%. This gives target prices of $75.53 and $68.40 respectively based on the current annual dividend of $3.40. I think the average high dividend yield will continue to drop and level out around the 4.25% level, but for the sake of being conservative I'll use the 3 year average of 4.50%. Phillip Morris is currently trading at a 15.9% premium to the average high dividend yield valuation.

Average Low PE Ratio:

Phillip Morris' average low PE ratio for the past 3 years is 13.80 and for the past 6 years is 12.40. This corresponds to a price per share of $77.15 and $69.30 respectively based off the analyst estimate of $5.59 per share for fiscal year 2013. Both are relatively close given the short history, but I feel the 3 year average is closer to what you'll actually see. Phillip Morris is currently trading at a 13.5% premium to the 3 year low PE ratio.

Average Low P/S Ratio:

Phillip Morris' average low PS ratio for the past 3 years is 1.55 and for the past 6 years is 1.34. This corresponds to a price per share of $78.42 and $67.68 respectively based off the analyst estimate for revenue growth from FY 2012 to FY 2013. Currently, their current PS ratio is 1.73 on a trailing twelve months basis. Both ratios are relatively close so I'll use the 6 year ratio just to be conservative. Phillip Morris is currently trading at a 29.3% premium to this price.

Dividend Discount Model:

For the DDM, I assumed that Phillip Morris will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, or 4 year growth rates. In this case that would be 13.09%. After that I assumed they can continue to raise dividends for 3 years at 75% of 13.09% or 9.82% and in perpetuity at 3.50%. The dividend growth rates are based off fiscal year payouts and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on the DDM, Phillip Morris is worth $87.26, meaning it's fairly valued.

PE Ratios:

Phillip Morris's trailing PE is 16.83 and it's forward PE is 14.07. The PE3 based on the average earnings for the last 3 years is 17.93. I like to see the PE3 be less than 15 which PM is currently over by a bit. Although to me this is because they are still experiencing solid growth leading to larger changes in the EPS values. Compared to it's industry, Phillip Morris seems to be fairly valued versus BTI (16.83). All industry comparisons are on a TTM basis. PM's PEG for the next 5 years is currently at 1.38 while BTI is at 1.63. Based on the PEG ratio, Phillip Morris is undervalued versus BTI. A lower PEG ratio is better because you're paying less for the growth of the company.

Fundamentals:

Phillip Morris' gross margins for FY 2011 and FY 2012 were 27.9% and 28.2% respectively. They have averaged a 27.4% gross profit margin since becoming an independent company in 2008, with a low of 27.0% in FY 2008. Their net income margin for the same years were 11.6% and 11.8%. Since 2008 their net income margin has averaged 11.2% with a low of 10.6% in FY 2009. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. Phillip Morris is under my gross margin levels, but their net income is still above the 10% threshhold. Since each industry is different and allows for different margins, I feel it's prudent to compare PM to its industry. For FY 2012, Phillip Morris captured only 73.2% of the gross margin for the industry and 88.7% of the net income margin. I was actually surprised to see that PM is doing worse that the industry on the margins. My guess is that's because they are still a young independent company and due to the growth of the company the margins have suffered some.

Share Buyback:

Phillip Morris' has committed to buying back shares as a way to return cash to shareholders. Since FY 2008, they've purchased 18.6% of their shares outstanding for an average annualized decrease of 5.0%. Buybacks are great as long as they are purchasing shares at a value price point, otherwise they are reducing shareholder value through the buyback program. Looking at the historical data, the increased buyback program coincides with better value prices available in the market. By repurchasing shares, Phillip Morris is able to increase EPS and management can return cash to shareholders this way by increasing the ownership stake of the company for all the outstanding shares.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

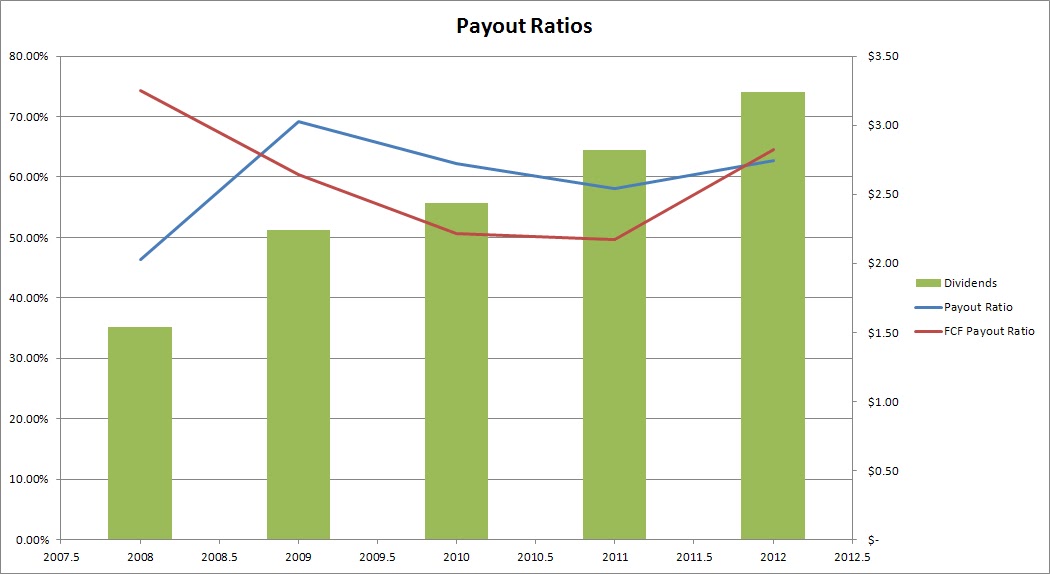

Phillip Morris is a dividend challenger with 5 consecutive years of dividend increases. Of course we can't fault them for that since they've only been around since 2008 as an independent company. They have increased the dividend at a 14.89%, 13.09%, and 16.04% rate for the last 1,3, and 4 year periods. Not only have they been growing the dividend at a great rate, the current yield is at a solid 3.88% level currently. Their payout ratio based off EPS has increased since FY 2008 which has allowed the dividend to increase faster than EPS have grown. I expect it to track closer to EPS growth going forward. Since FY 2008 the payout ratio has increased from 46.4% to 62.7% and has averaged 59.7% over that time.

Phillip Morris is a cash generating machine. Their free cash flow has grown fro $6.836B in 2008 to $8.365B in 2012, good for a 5.2% annualized increase. The free cash flow payout ratio has averaged only 59.9% since FY 2008, which is right around the payout based on earnings. Annual total shareholder return when accounting for buybacks plus dividends has averaged 129.3% of FCF since FY 2008 so it will have to come down or management. This has been made possible due to the increase of debt. While I don't like the companies I own to have a significant amount of debt, PM was able to borrow at rates lower than the dividend yield and used the debt to buyback shares. Essentially they have been practicing interest rate arbitrage and in effect been capitalizing on the low interest rate environment of the last few years. Eventually this will have to stop but as long as they are watchful of the debt levels this can prove to be successful.

Return on Equity and Return on Capital Invested:

Phillip Morris' equity stake is actually negative now thanks to all of the debt that has been added in the last few years. I'm not overly concerned yet but would like to see the increase of debt at least slow down a bit. Their ROCI has averaged a 48.0% rate since 2008 and has grown from 36.5% in 2008 to 65.2% in 2012. I don't necessarily look for any absolute values, rather I like to see stable to increasing levels over the long term because it shows the consistency that management is able to invest in growing the business.

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how Phillip Morris has done on that front. Their revenue growth since 2008 has been solid with a 5.01% annual increase and their net income has been growing at a 7.36% rate. Since their net income has been growing faster than revenue, their net income margin has increased from 10.8% to 11.8% between FY 2008 and FY 2012. Analysts expect only meager revenue growth in 2013 of 2.50% but 5.30% in 2014.

Forecast:

The chart shows the historical high and low prices since 2008 and the forecast based on the average PE ratios and the expected EPS values. I have also included a forecast based off a PE ratio that is only 75% of the average low PE ratio. I like to the look to buy at the 75% Low PE price or lower to provide for a large margin of safety, although this price doesn't usually come around very often. In the case of Phillip Morris, the target low PE is 13.10 and the 0.75 * PE is 9.82. This corresponds to an entry price of $83.84 based off the expected earnings for FY 2013 of $5.59, with a 75% target price of $54.92. Currently Phillip Morris is trading at a $32.62 premium to the 75% low PE target price and a $3.70 premium to the average PE price. If you believe the analyst estimates are pretty close, then Phillip Morris is trading right around it's fair value range.

Conclusion:

The average of all the valuation models gives a target entry price of $84.92 which means that Phillip Morris is currently trading at a 3.1% premium to the target entry price. I've also calculated it with the highest and lowest valuation methods thrown out. In this case, the DCF and average high dividend valuations are removed and the new average is $79.98. Phillip Morris is trading at a 9.5% premium to this price as well.

Assuming that Phillip Morris can grow their earnings and dividends at the rates that I assumed, you're looking at solid returns over the next 10 years. In 2023, EPS would be $10.93 and slapping an average PE of 15.00 gives a price of $163.85. Over the next 10 years you'd also receive $65.33 in dividends for a total return of 261.81% which is good for a 10.10% annualized rate if you purchase at the current price. If you purchase at my target entry price of $84.92, your projected 10 year total return jumps to 269.88% for an annualized return of 10.44%.

According to Yahoo! Finance the 1 year target estimate is at $99.07 suggesting plenty of room for capital gains at current price levels. Morningstar has PM rated as a 3 star stock meaning it's a hold. I recently added to my position in Phillip Morris right around current price levels. I like Phillip Morris' potential for growth of both the company and the dividend going forward. They are essentially the international arm of Altria (MO) which I think is the better place to be. International regulations on cigarettes and tobacco products are much more relaxed and the market is actually growing rather than declining like in the United States. The big driver of growth in the tobacco business is going to be the international markets, especially the emerging markets. Granted China has a ridiculous number of people, but China smokes approximately 2.163 Trillion cigarettes each year, compared to 331 Billion in the United States. If Phillip Morris can just get a 15% market share in China alone, that's essentially equal to the entire market in the United States. So in other words there's plenty of room for Phillip Morris to grow their business since we only looked at one country and not the other emerging markets such as Indonesia, Vietnam, Brazil, India and the rest.

Laws here in the United States don't necessarily reflect what will happen across the globe. But it will be interesting to see whether the recent marijuana law changes will continue to spread through other states and eventually lead to the Federal government to allow the production/consumption of marijuana much like tobacco. If that does happen then I expect the major domestic tobacco companies to reap the benefit of that as well as Phillip Morris should it spread internationally as well.

To check out more reports check out my Stock Analysis page.

What do you think about Phillip Morris as a DG investment at today's prices? How do you think the long-term dividend growth prospects are?

Company Background (sourced from Yahoo! Finance):

Philip Morris International Inc., through its subsidiaries, manufactures and sells cigarettes and other tobacco products. The company’s portfolio of international and local brands include Marlboro, Merit, Parliament, Virginia Slims, L&M, Chesterfield, Bond Street, Lark, Muratti, Next, Philip Morris, and Red & White. It also owns various local cigarette brands, such as Sampoerna, Dji Sam Soe, and U Mild in Indonesia; Fortune, Champion, and Hope in the Philippines; Diana in Italy; Optima and Apollo-Soyuz in Russia; Morven Gold in Pakistan; Boston in Colombia; Belmont, Canadian Classics, and Number 7 in Canada; Best and Classic in Serbia; f6 in Germany; Delicados in Mexico; Assos in Greece; and Petra in the Czech Republic and Slovakia. The company sells its products in approximately 180 countries in the European Union, Eastern Europe, the Middle East, Africa, Asia, Latin America, and Canada.

DCF Valuation:

Analysts expect Phillip Morris to grow earnings 11.23% per year for the next five years and I've assumed they can continue to grow at 3.50% per year thereafter. Running these numbers through a two stage DCF analysis with a 10% discount rate yields a fair value price of $116.97. This means the shares are trading at a 25.2% discount to the DCF.

Graham Number:

The Graham Number valuation method offers no value in Phillip Morris' case since the book value per share is negative. Due to this I will just ignore the Graham Number in my calculations, although it is something to keep in mind.

Average High Dividend Yield:

Phillip Morris' average high dividend yield for the past 3 years is 4.50% and for the past 6 years is 4.97%. This gives target prices of $75.53 and $68.40 respectively based on the current annual dividend of $3.40. I think the average high dividend yield will continue to drop and level out around the 4.25% level, but for the sake of being conservative I'll use the 3 year average of 4.50%. Phillip Morris is currently trading at a 15.9% premium to the average high dividend yield valuation.

Phillip Morris' average low PE ratio for the past 3 years is 13.80 and for the past 6 years is 12.40. This corresponds to a price per share of $77.15 and $69.30 respectively based off the analyst estimate of $5.59 per share for fiscal year 2013. Both are relatively close given the short history, but I feel the 3 year average is closer to what you'll actually see. Phillip Morris is currently trading at a 13.5% premium to the 3 year low PE ratio.

Average Low P/S Ratio:

Phillip Morris' average low PS ratio for the past 3 years is 1.55 and for the past 6 years is 1.34. This corresponds to a price per share of $78.42 and $67.68 respectively based off the analyst estimate for revenue growth from FY 2012 to FY 2013. Currently, their current PS ratio is 1.73 on a trailing twelve months basis. Both ratios are relatively close so I'll use the 6 year ratio just to be conservative. Phillip Morris is currently trading at a 29.3% premium to this price.

Dividend Discount Model:

For the DDM, I assumed that Phillip Morris will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, or 4 year growth rates. In this case that would be 13.09%. After that I assumed they can continue to raise dividends for 3 years at 75% of 13.09% or 9.82% and in perpetuity at 3.50%. The dividend growth rates are based off fiscal year payouts and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on the DDM, Phillip Morris is worth $87.26, meaning it's fairly valued.

PE Ratios:

Phillip Morris's trailing PE is 16.83 and it's forward PE is 14.07. The PE3 based on the average earnings for the last 3 years is 17.93. I like to see the PE3 be less than 15 which PM is currently over by a bit. Although to me this is because they are still experiencing solid growth leading to larger changes in the EPS values. Compared to it's industry, Phillip Morris seems to be fairly valued versus BTI (16.83). All industry comparisons are on a TTM basis. PM's PEG for the next 5 years is currently at 1.38 while BTI is at 1.63. Based on the PEG ratio, Phillip Morris is undervalued versus BTI. A lower PEG ratio is better because you're paying less for the growth of the company.

Fundamentals:

Phillip Morris' gross margins for FY 2011 and FY 2012 were 27.9% and 28.2% respectively. They have averaged a 27.4% gross profit margin since becoming an independent company in 2008, with a low of 27.0% in FY 2008. Their net income margin for the same years were 11.6% and 11.8%. Since 2008 their net income margin has averaged 11.2% with a low of 10.6% in FY 2009. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. Phillip Morris is under my gross margin levels, but their net income is still above the 10% threshhold. Since each industry is different and allows for different margins, I feel it's prudent to compare PM to its industry. For FY 2012, Phillip Morris captured only 73.2% of the gross margin for the industry and 88.7% of the net income margin. I was actually surprised to see that PM is doing worse that the industry on the margins. My guess is that's because they are still a young independent company and due to the growth of the company the margins have suffered some.

Share Buyback:

Phillip Morris' has committed to buying back shares as a way to return cash to shareholders. Since FY 2008, they've purchased 18.6% of their shares outstanding for an average annualized decrease of 5.0%. Buybacks are great as long as they are purchasing shares at a value price point, otherwise they are reducing shareholder value through the buyback program. Looking at the historical data, the increased buyback program coincides with better value prices available in the market. By repurchasing shares, Phillip Morris is able to increase EPS and management can return cash to shareholders this way by increasing the ownership stake of the company for all the outstanding shares.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Phillip Morris is a dividend challenger with 5 consecutive years of dividend increases. Of course we can't fault them for that since they've only been around since 2008 as an independent company. They have increased the dividend at a 14.89%, 13.09%, and 16.04% rate for the last 1,3, and 4 year periods. Not only have they been growing the dividend at a great rate, the current yield is at a solid 3.88% level currently. Their payout ratio based off EPS has increased since FY 2008 which has allowed the dividend to increase faster than EPS have grown. I expect it to track closer to EPS growth going forward. Since FY 2008 the payout ratio has increased from 46.4% to 62.7% and has averaged 59.7% over that time.

Phillip Morris is a cash generating machine. Their free cash flow has grown fro $6.836B in 2008 to $8.365B in 2012, good for a 5.2% annualized increase. The free cash flow payout ratio has averaged only 59.9% since FY 2008, which is right around the payout based on earnings. Annual total shareholder return when accounting for buybacks plus dividends has averaged 129.3% of FCF since FY 2008 so it will have to come down or management. This has been made possible due to the increase of debt. While I don't like the companies I own to have a significant amount of debt, PM was able to borrow at rates lower than the dividend yield and used the debt to buyback shares. Essentially they have been practicing interest rate arbitrage and in effect been capitalizing on the low interest rate environment of the last few years. Eventually this will have to stop but as long as they are watchful of the debt levels this can prove to be successful.

Return on Equity and Return on Capital Invested:

Phillip Morris' equity stake is actually negative now thanks to all of the debt that has been added in the last few years. I'm not overly concerned yet but would like to see the increase of debt at least slow down a bit. Their ROCI has averaged a 48.0% rate since 2008 and has grown from 36.5% in 2008 to 65.2% in 2012. I don't necessarily look for any absolute values, rather I like to see stable to increasing levels over the long term because it shows the consistency that management is able to invest in growing the business.

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how Phillip Morris has done on that front. Their revenue growth since 2008 has been solid with a 5.01% annual increase and their net income has been growing at a 7.36% rate. Since their net income has been growing faster than revenue, their net income margin has increased from 10.8% to 11.8% between FY 2008 and FY 2012. Analysts expect only meager revenue growth in 2013 of 2.50% but 5.30% in 2014.

Forecast:

Conclusion:

The average of all the valuation models gives a target entry price of $84.92 which means that Phillip Morris is currently trading at a 3.1% premium to the target entry price. I've also calculated it with the highest and lowest valuation methods thrown out. In this case, the DCF and average high dividend valuations are removed and the new average is $79.98. Phillip Morris is trading at a 9.5% premium to this price as well.

Assuming that Phillip Morris can grow their earnings and dividends at the rates that I assumed, you're looking at solid returns over the next 10 years. In 2023, EPS would be $10.93 and slapping an average PE of 15.00 gives a price of $163.85. Over the next 10 years you'd also receive $65.33 in dividends for a total return of 261.81% which is good for a 10.10% annualized rate if you purchase at the current price. If you purchase at my target entry price of $84.92, your projected 10 year total return jumps to 269.88% for an annualized return of 10.44%.

According to Yahoo! Finance the 1 year target estimate is at $99.07 suggesting plenty of room for capital gains at current price levels. Morningstar has PM rated as a 3 star stock meaning it's a hold. I recently added to my position in Phillip Morris right around current price levels. I like Phillip Morris' potential for growth of both the company and the dividend going forward. They are essentially the international arm of Altria (MO) which I think is the better place to be. International regulations on cigarettes and tobacco products are much more relaxed and the market is actually growing rather than declining like in the United States. The big driver of growth in the tobacco business is going to be the international markets, especially the emerging markets. Granted China has a ridiculous number of people, but China smokes approximately 2.163 Trillion cigarettes each year, compared to 331 Billion in the United States. If Phillip Morris can just get a 15% market share in China alone, that's essentially equal to the entire market in the United States. So in other words there's plenty of room for Phillip Morris to grow their business since we only looked at one country and not the other emerging markets such as Indonesia, Vietnam, Brazil, India and the rest.

Laws here in the United States don't necessarily reflect what will happen across the globe. But it will be interesting to see whether the recent marijuana law changes will continue to spread through other states and eventually lead to the Federal government to allow the production/consumption of marijuana much like tobacco. If that does happen then I expect the major domestic tobacco companies to reap the benefit of that as well as Phillip Morris should it spread internationally as well.

To check out more reports check out my Stock Analysis page.

What do you think about Phillip Morris as a DG investment at today's prices? How do you think the long-term dividend growth prospects are?

I like PM and am looking to get in a position with around a 4% yield. Like you I like that the company is international. The other big tobacco players (MO, LO and RAI) are all domestic which doesn't leave much room for growth plus they continue to face increasing pressures from fed and state regulations. I think the international aspect of PM provides a little safety as different local governments try to regulate tobacco. Also, if you've ever been overseas, it seems like practically everyone is smoking! Guess they didn't get the memo that smoking is bad for you.

ReplyDeleteDGSI,

DeleteI've got a decent sized position in PM right now and combined with my LO position I have about as much tobacco exposure as I'd like at the moment. I think PM has the best prospects going forward due to the fact that other governments are no where near as harsh on tobacco products as the United States. Plus it doesn't hurt that the tobacco market is growing and growing quite fast I might internationally. As you mentioned so many people smoke in other countries. The China statistic was pretty amazing to me. Over 2 trillion cigarettes smoked each year. In one country! So there's plenty of growth available as long as you can get penetration. As an attempting to quit smoker, I have to admit the stickiness of the product and the recurring purchase is great for business, although not necessarily for health.

Thanks for stopping by!

You many want to look at UVV. They are a world wide tobacco supplier that has tentacles in many countries including the largest growth area of Eastern Europe.

DeleteDGSI - PM has a yield of 3.93% as of todays close. And it is due for a increase, which will likely push it well, above 4%.

ReplyDeleteMan, PM is my favorite dividend growth stock of them all! It has appreciated a lot since my last purchase (almost 2 years ago, holy crap!) to the point where it is the highest weighting in my portfolio. Even though I am in love with the company I am not willing to rely excessively on any single business. I decided to increase my tobacco exposure a while back by purchasing LO instead, even though I view it as second rate to PM.

ReplyDeleteI think PM is about fairly valued right now, and that alone is enough reason to buy. There are a lot of positives here. I believe we have a dividend contender in the making, I'd say fair value is fine for Philip Morris!

I've noticed that tobacco stocks do get spooked by new or potentially new regulations from time to time. That is the perfect spot to pick up some shares. I haven't read anything negative in a while though.

Bottom Line: If PM wasn't my #1 holding, I'd be a buyin!

CI,

DeleteI think PM is best of breed if only because they aren't subject to US regulations. I wouldn't say it's a steal but $84-86 has me really interested. I wish I could have picked some up a few years back but it seemed to always slip through my fingers.

LO took a big hit when rumors of the FDA no longer allowing menthol flavored cigarettes came out. Personally I don't expect any game-changing regulations to come through against tobacco because there's just too much money involved between lobbying and tax revenue. Although those rumors sure do offer some nice opportunities.

Thanks for stopping by!