Dividend Growth Checkup - 2022 #Dividend #DividendGrowth

As the calendar turns to the new year it's a time of both reflection and planning. While this is a very much a historical analysis, it helps to put things in context around where our portfolio has been in order to formulate a game plan for where we want it to go as well as how we want to get there.

While 2022 could have been a bit better on the dividend growth front, complaints are largely meaningless as we still had solid organic dividend growth even if it was a slight step back from 2021.

The majority of my investments are in what would be considered as dividend growth stocks. Companies that have consistently paid and grown their dividend payment to shareholders over time. The strategy appealed to me because it helps to keep me focused on the underlying business as well as my expectations moving forward rather that what Mr. Market is willing to buy or sell shares at today.

It's been scary at times as there's a lot of unknowns and the last few years alone have brought about a global pandemic, a supply chain crisis, war in Europe, a spike in inflation, and countless other issues. However, I sleep well at night as my dividends continue to churn higher, sometimes slower than I'd like, year after year as the businesses I own navigate the crisis du jour and hopefully come out stronger on the other side.

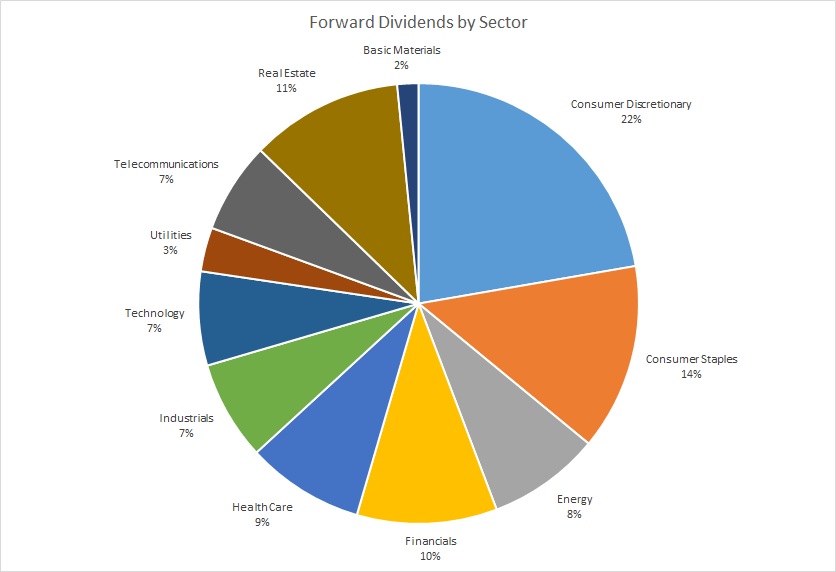

Forward Dividends by Sector

I don't have a strict sector weighting plan; rather I keep more of a rough guideline in the back of my mind. However, instead of selling to reduce exposure to overweight sectors I prefer to tackle the sector exposure issue through additional savings and investments.

Compared to the end of 2021 my forward dividends for this account ended up 18.5% higher compared. This was a modest step back from 2021's year-over-year growth of 22.9% although I'm still quite happy with the results.

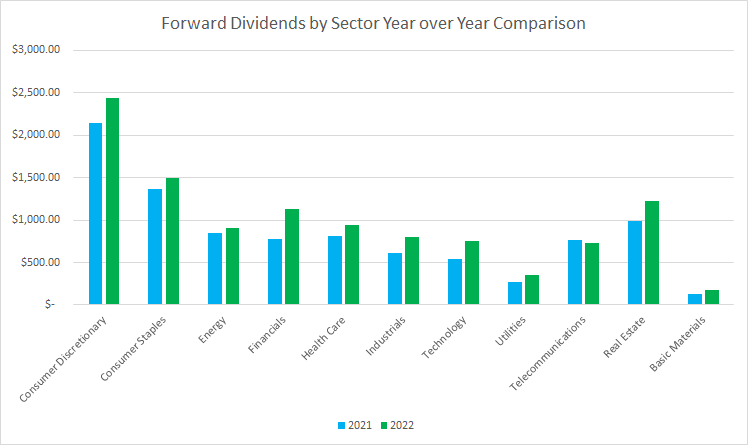

Forward Dividends by Sector Year over Year (Author)

Every sector except for telecommunications saw an increase in 2022 which was dragged lower by the dividend cut/right-sizing from AT&T (T). The financials sector saw the largest increase in both dollar and percentage terms.

Forward Dividends by Sector (Author)

The sector weightings aren't uber critical to me as many businesses fall into several categories. For example does Realty Income (O) fall under real estate or consumer discretionary or consumer staples, arguably it could be divided into all three. Same thing with Visa (V): is that financials or technology?

While the financials sector saw the largest year-over-year increase, those weren't due to banks rather financial adjacent companies like Visa (V), Intercontinental Exchange (ICE), Blackrock (BLK), and CME Group (CME) being increase positions or new positions added throughout the year.

The consumer staples sector is the only one that I feel is really out of sorts for me; however, that's largely due to the premium that is typically placed on companies in those sectors.

Dividend Clubs

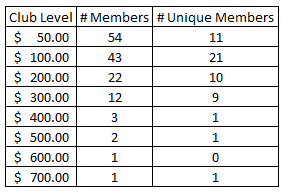

Each year I like to examine my holdings to see how many provide different thresholds of annual dividends. I consider each level as its own "Dividend Club" based on the milestone level of dividends. In order to join one of the Dividend Clubs, the position needs to provide at least that level of forward dividends with the unique members being those that are capped out within that level.

The total members represents the total number of positions that I own that pay at least that level of annual dividends. While the unique members are those companies that pay annual dividends between that level and the next level higher.

One of my goals for 2022 was to focus more on building up the size of positions and I believe I did an adequate job of that throughout the year.

The $50 Club increased by 9 members compared to 2021 and now sits at 54 total members and 11 unique members.

The $100 Club rose by 9 members as well with 43 total members and 21 unique members.

The $200 Club saw a modest increase of just 2 members throughout 2022 with 22 total members and 10 unique members.

The $300 Club saw a sizable increase gaining 4 members during the year and bringing the total count to 12 with the unique members rising to 9.

Even though there's not a large member count in the next 4 levels it's encouraging to see what time, patience, and consistency has brought.

The $400 Club is up to 3 total members, an increase of 1 compared to 2021, with the unique member count at 1.

The $500 Club increased by 1 and now has 2 total members with a unique member count of 1.

There's no unique members in the $600 Club; however, the $700 Club was opened during 2022 with continued investment and dividend growth from Altria (MO).

Looking ahead to 2023 assuming modest dividend growth and reinvestment yields, I would expect the $400 Club to gain 2 members, the $300 Club to gain 2 members, and the $200 Club to gain 1 member.

Each year I like to examine my holdings to see how many provide different thresholds of annual dividends. I consider each level as its own "Dividend Club" based on the milestone level of dividends. In order to join one of the Dividend Clubs, the position needs to provide at least that level of forward dividends with the unique members being those that are capped out within that level.

The total members represents the total number of positions that I own that pay at least that level of annual dividends. While the unique members are those companies that pay annual dividends between that level and the next level higher.

One of my goals for 2022 was to focus more on building up the size of positions and I believe I did an adequate job of that throughout the year.

The $50 Club increased by 9 members compared to 2021 and now sits at 54 total members and 11 unique members.

The $100 Club rose by 9 members as well with 43 total members and 21 unique members.

The $200 Club saw a modest increase of just 2 members throughout 2022 with 22 total members and 10 unique members.

The $300 Club saw a sizable increase gaining 4 members during the year and bringing the total count to 12 with the unique members rising to 9.

Even though there's not a large member count in the next 4 levels it's encouraging to see what time, patience, and consistency has brought.

The $400 Club is up to 3 total members, an increase of 1 compared to 2021, with the unique member count at 1.

The $500 Club increased by 1 and now has 2 total members with a unique member count of 1.

There's no unique members in the $600 Club; however, the $700 Club was opened during 2022 with continued investment and dividend growth from Altria (MO).

Looking ahead to 2023 assuming modest dividend growth and reinvestment yields, I would expect the $400 Club to gain 2 members, the $300 Club to gain 2 members, and the $200 Club to gain 1 member.

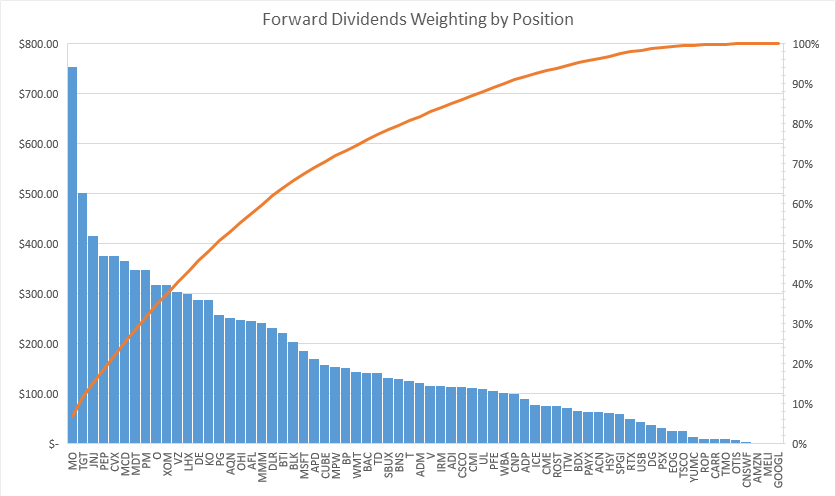

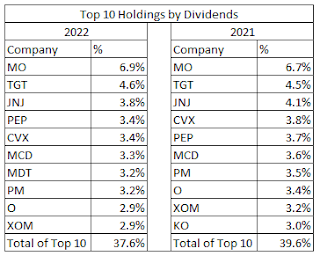

Top 10 Holdings by Forward Dividends

My forward dividends are heavily weighted towards a handful of positions. That's partly by design and also due to many of the companies I'm invested in carrying meager dividend yields but that come with the potential for much faster dividend growth and capital gain potential. My top fifteen positions, by forward dividends, account for right around 50% of my expected 2023 dividends.

Forward Dividends by Position (Author)

The Top 10 holdings by dividends account for 37.6% of my forward dividends at end of year 2022. That continues the trend of broader diversification where the top ten were at 42.6% in 2020 and 39.6% in 2021. That also goes along with my goal mentioned above about aiming to build up my smaller positions so they pack a bigger punch.

There was some minor shuffling among the top 10 constituents. However, the big change was that Coca-Cola (KO) dropped from the top 10 with Medtronic (MDT) replacing them. That was due to Medtronic getting more capital allocated to it throughout the year as the share price pulled back spiking the yield to what I considered very attractive levels.

Dividend Growth

My goal for 2022, as it was for 2021, was to at least maintain the number of holdings. That didn't quite work out as I ended 2022 with 68 holdings versus 67 at the end of 2021.

Going into 2022 I didn't have a hard set plan to reduce the number of positions and with the general downtrend in the markets throughout the year that also sucked a lot of the overvaluation out of the share prices.

While the total count rose by just one company, there was a lot more going on under the surface. I had sold out of three positions during the year: Honeywell (HON), Leggett & Platt (LEG), and Twilio (TWLO). One of these things is not like the other am I right? S&P Global (SPGI) also completed their acquisition of IHS Markit (INFO) which led to a total reduction of four companies.

That means that I added five positions during 2022: Illinois Tool Works (ITW), CME Group (CME), Cummins (CMI), Thermo Fisher Scientific (TMO), and Tractor Supply Company (TSCO). Outside of those five, new capital was invested only within the existing companies in my portfolio.

My goal for 2022, as it was for 2021, was to at least maintain the number of holdings. That didn't quite work out as I ended 2022 with 68 holdings versus 67 at the end of 2021.

Going into 2022 I didn't have a hard set plan to reduce the number of positions and with the general downtrend in the markets throughout the year that also sucked a lot of the overvaluation out of the share prices.

While the total count rose by just one company, there was a lot more going on under the surface. I had sold out of three positions during the year: Honeywell (HON), Leggett & Platt (LEG), and Twilio (TWLO). One of these things is not like the other am I right? S&P Global (SPGI) also completed their acquisition of IHS Markit (INFO) which led to a total reduction of four companies.

That means that I added five positions during 2022: Illinois Tool Works (ITW), CME Group (CME), Cummins (CMI), Thermo Fisher Scientific (TMO), and Tractor Supply Company (TSCO). Outside of those five, new capital was invested only within the existing companies in my portfolio.

During 2022, 59 of my 68 holdings raised their dividends last year while 5 maintained their dividend. There was 1 dividend cut, from AT&T (T), and 3 of my holdings do not currently pay a dividend.

Let's start with the companies that froze their dividend payment. The 5 freezers include Constellation Software (OTCPK:CNSWF), Iron Mountain (IRM), Omega Healthcare Investors (OHI), Unilever plc (UL), and Yum China (YUMC).

All of those are repeat offenders except for Unilever which decided to freeze its payout during the year.

In 2021, Constellation Software announced they will be forgoing dividend increases to preserve more capital for Mark Leonard and his team to devote to more acquisitions. Considering their prudent capital allocation approach and results, I'm just fine with that, and if they wanted to take back the meager $1 dividend, I wouldn't complain.

Iron Mountain had previously announced that dividend raises wouldn't be coming until their leverage was reduced and the payout ratio brought in line. Well, they've reached that point so if there's no raise in 2023 then I'll have a decision to make.

Omega Healthcare Investors (OHI) has been in limbo the last several years as their business was hit especially hard during COVID and had stumbles in prior years. I didn't expect a raise from them in 2022 so I wasn't disappointed with the lack of an increase. Thank goodness for low expectations! Of course a dividend yield that's been greater than 7% for the last few years helps to make up for that.

YUM China continues to be a head scratcher. They have room to increase their dividend in terms of payout ratio, but have failed to give a raise since late 2018. They've been through the wringer the last few years with China's zero-COVID policy although restrictions appear to be loosening which should benefit YUM China. I'll still continue to hold them, but if a dividend increase doesn't come over the next year or two it might be time to allocate this capital elsewhere.

Unilever was the only surprise freezer. Part of that is likely due to the more aggressive payout ratio which still sits in the 70%+ area. I'll be watching them closely throughout 2023 and hope to see a return to dividend growth even if it's modest.

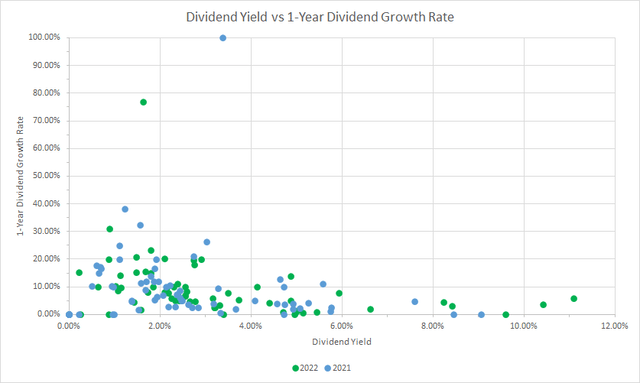

Dividend Yield vs Dividend Growth Rate

As a dividend growth investor that's relatively young, I aim to strike a balance between higher-yielding, but slower-growing companies with lower-yielding, but faster-growing businesses. While I love seeing those dividends hitting my account I realize that I'm not following this strategy to create the most income in the next 5 years; rather it's an attempt to set up a very rewarding portfolio 10-20 years down the line.

Ideally, I want the bulk of my investments in what I consider the "sweet spot" which is somewhere around a 2.5% to 4.0% current yield with 5.0% to 10.0% annual dividend growth. In my opinion, that strikes a solid balance between adequate current dividend yield along with future dividend growth.

Dividend Yield vs Growth Rate (Author)

With the overall pullback in the markets throughout the year I'd have expected to see a larger shift towards higher yields and while that played out among some of my holdings it doesn't appear to be a broad trend. Of course it helps that a large chunk of my portfolio did not suffer the drawdown experienced by the markets in general.

Compared to 2021, 2022 looks fairly similar in terms of distribution between yields and growth rate.

As a dividend growth investor that's relatively young, I aim to strike a balance between higher-yielding, but slower-growing companies with lower-yielding, but faster-growing businesses. While I love seeing those dividends hitting my account I realize that I'm not following this strategy to create the most income in the next 5 years; rather it's an attempt to set up a very rewarding portfolio 10-20 years down the line.

Ideally, I want the bulk of my investments in what I consider the "sweet spot" which is somewhere around a 2.5% to 4.0% current yield with 5.0% to 10.0% annual dividend growth. In my opinion, that strikes a solid balance between adequate current dividend yield along with future dividend growth.

Dividend Yield vs Growth Rate (Author)

With the overall pullback in the markets throughout the year I'd have expected to see a larger shift towards higher yields and while that played out among some of my holdings it doesn't appear to be a broad trend. Of course it helps that a large chunk of my portfolio did not suffer the drawdown experienced by the markets in general.

Compared to 2021, 2022 looks fairly similar in terms of distribution between yields and growth rate.

Portfolio-Wide Dividend Growth

Dividend growth from my holdings pulled back during 2022 compared to 2021. However, I believe 2021 was a bit of an outlier year as many companies held back on dividend growth in 2020 and thus had more capacity to raise it in 2021 as things stabilized. Unfortunately, inflation reared its head in 2022 with many companies seeing their margins squeezed as a result and calls for a recession grew louder as the year went on.

The average increase for 2022 came to 8.5% while the average of just those that announced raises came to 10.2%. The previous years results were 10.5% and 11.4%, respectively.

For 2022, the median raise for just the growers came to 7.9%. Surprisingly the median didn't drop all that much when looking at the entire portfolio. Including the five companies that didn't increase and the one cut from AT&T, the median dropped to just 7.4%.

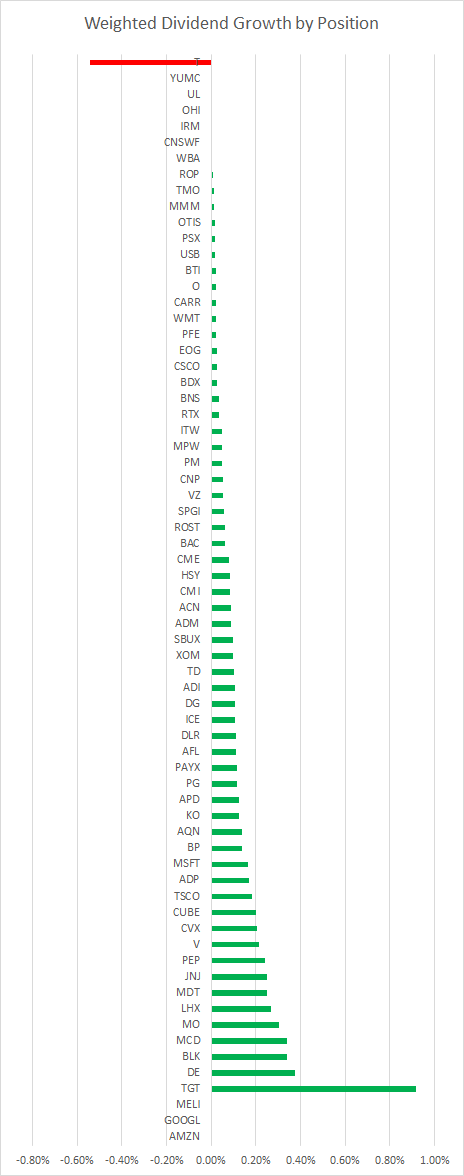

In order to calculate the weighted dividend growth rate, I use the 1-year dividend growth rate for Position X multiplied by the Dividends for Position X divided by the Total Dividends for the portfolio. I then repeat that for each position that I own and add them together to get the weighted dividend growth rate for the portfolio. The reason I do this is because the weighted dividend growth rate better reflects the organic dividend growth that you achieve across the portfolio.

Assume that you have a portfolio with just two holdings: Company A pays a 5.0% dividend yield with a 4.0% 1-year growth rate while Company B pays a 1.0% dividend yield with a 20.0% dividend growth rate. We'll assume at the start of the year you invest $10k in each company such that your starting dividends are $600 total. At the end of the year, each company raises its dividend by the respective growth rate, and your forward dividends at the end of the year are now $645.

The average dividend growth rate between those two companies is 12.5%; however, the weighted dividend growth rate is 7.5%. The weighted dividend growth rate is dragged lower due to Company A's outsized proportion of the provided dividends.

Dividend growth from my holdings pulled back during 2022 compared to 2021. However, I believe 2021 was a bit of an outlier year as many companies held back on dividend growth in 2020 and thus had more capacity to raise it in 2021 as things stabilized. Unfortunately, inflation reared its head in 2022 with many companies seeing their margins squeezed as a result and calls for a recession grew louder as the year went on.

The average increase for 2022 came to 8.5% while the average of just those that announced raises came to 10.2%. The previous years results were 10.5% and 11.4%, respectively.

For 2022, the median raise for just the growers came to 7.9%. Surprisingly the median didn't drop all that much when looking at the entire portfolio. Including the five companies that didn't increase and the one cut from AT&T, the median dropped to just 7.4%.

In order to calculate the weighted dividend growth rate, I use the 1-year dividend growth rate for Position X multiplied by the Dividends for Position X divided by the Total Dividends for the portfolio. I then repeat that for each position that I own and add them together to get the weighted dividend growth rate for the portfolio. The reason I do this is because the weighted dividend growth rate better reflects the organic dividend growth that you achieve across the portfolio.

Assume that you have a portfolio with just two holdings: Company A pays a 5.0% dividend yield with a 4.0% 1-year growth rate while Company B pays a 1.0% dividend yield with a 20.0% dividend growth rate. We'll assume at the start of the year you invest $10k in each company such that your starting dividends are $600 total. At the end of the year, each company raises its dividend by the respective growth rate, and your forward dividends at the end of the year are now $645.

The average dividend growth rate between those two companies is 12.5%; however, the weighted dividend growth rate is 7.5%. The weighted dividend growth rate is dragged lower due to Company A's outsized proportion of the provided dividends.

Weighted Dividend Growth by Position (Author)

For 2022 the weighted dividend growth rate for my portfolio came to 6.7% compared to 2021's 8.7%.. I'm pretty happy with those results considering that over 5.5% of my dividends provided zero contribution or were a headwind.

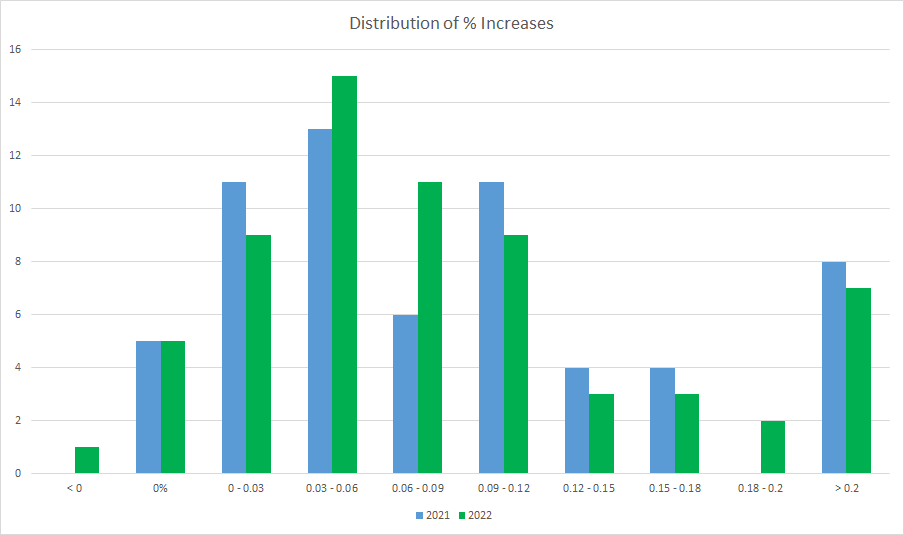

Distribution of Dividend Increases

Additionally, I like to see how the dividend increases are distributed among my holdings.

Distribution of Dividend Growth (Author)

Compared to 2021, 2022 saw a slow down in dividend growth although that's to be expected. Last year definitely saw a larger number of my holdings that announced raises in the 3%-12% range versus 2021 with less in the 12%+ area. Unfortunately, 2022 also brought about the nasty cut from AT&T which really dragged down the average increase.

Focus for 2023

Last year was a solid year despite the modest step back in overall dividend growth compared to 2021. Considering that 2021 was kind of a catch-up year for some companies that opted for modest raises in 2020 due to the uncertainty surrounding the pandemic I'm pretty happy with the results.

An average increase of 10.2% among the holdings that announced raises during the year with an 8.5% average increase across all of my holdings is more than adequate for what I'm targeting. My goal is a current yield in the 2.5% - 3.5% range, likely closer to the 2.5% - 3.0% area, with a weighted dividend growth rate in the 7-9% range. Unfortunately the weighted dividend growth rate did fall a bit short in 2022 at just 6.7%.

Last year was a great year for this portfolio with total dividends received coming in over $2,500 per quarter which was nearly $500 per quarter more than 2021's quarterly average. We also crossed several milestones in terms of forward dividends surpassing both the $10k mark as well as the $11k mark. What's really encouraging is that based on pretty modest growth assumptions and reinvestment we should get very close, if not exceed, the $12k mark this year without accounting for new capital being invested throughout the year.

I completely failed my goal of not adding new positions to my FI Portfolio with a net addition of 1 holding throughout the year. Although that was made up of 3 positions being sold out of, 1 being removed after its M&A completed, and 5 companies being added.

My goal for 2023 is to continue to build up the sizes of my existing positions rather than expanding the number of holdings. I don't have a hard-set goal to reduce the position count at this time; however, there's several companies that are potentially on the chopping block due to their weighting being too small to really even be worth the hassle or continued business struggles.

Image Source

Last year was a solid year despite the modest step back in overall dividend growth compared to 2021. Considering that 2021 was kind of a catch-up year for some companies that opted for modest raises in 2020 due to the uncertainty surrounding the pandemic I'm pretty happy with the results.

An average increase of 10.2% among the holdings that announced raises during the year with an 8.5% average increase across all of my holdings is more than adequate for what I'm targeting. My goal is a current yield in the 2.5% - 3.5% range, likely closer to the 2.5% - 3.0% area, with a weighted dividend growth rate in the 7-9% range. Unfortunately the weighted dividend growth rate did fall a bit short in 2022 at just 6.7%.

Last year was a great year for this portfolio with total dividends received coming in over $2,500 per quarter which was nearly $500 per quarter more than 2021's quarterly average. We also crossed several milestones in terms of forward dividends surpassing both the $10k mark as well as the $11k mark. What's really encouraging is that based on pretty modest growth assumptions and reinvestment we should get very close, if not exceed, the $12k mark this year without accounting for new capital being invested throughout the year.

I completely failed my goal of not adding new positions to my FI Portfolio with a net addition of 1 holding throughout the year. Although that was made up of 3 positions being sold out of, 1 being removed after its M&A completed, and 5 companies being added.

My goal for 2023 is to continue to build up the sizes of my existing positions rather than expanding the number of holdings. I don't have a hard-set goal to reduce the position count at this time; however, there's several companies that are potentially on the chopping block due to their weighting being too small to really even be worth the hassle or continued business struggles.

Image Source

Very Comprehensive report JC! It's always good to take a look back at how you've done and to assess where you want to go.

ReplyDeleteI especially liked your dividends club idea. I may implement something like that in the future. I just have one overall forward annual dividend and I try to increase that every year. But having a dividends club is a wonderful way at looking at the number of companies in terms of the dividend level they provide.

I use M1 Finance that sort of keep my portfolio in balance with each contribution, but I'll definitely consider doing something similar - especially if my account gets larger.

Finally, good luck with your 2023 goals. I think increasing the size of your holdings rather than expanding the number of holdings is a great goal and one that I share.