Income Update - February 2014

I'm a big proponent of tracking every single penny that comes into your hands if you're really wanting to make a change to your finances. Mental accounting is too difficult to keep track of and the mundane everyday expenses get forgotten. Once you keep a detailed history you can see that you're really spending $400 per month on restaurants or $100 on coffee or whatever little expenses that are fine by themselves but add up quickly to destroy a budget. This is why I like to keep track of all of my expenses to help keep myself accountable and looking to see what areas I'm just plain doing poor in. If you want to improve your finances, then please track everything for a 3 month span and then take action to make positive changes.

February's spending didn't go as well as I'd have liked. Nothing really stood out as being excessive and the total expenses came in right in line with January's spending. I need to find a way to start cutting some expenses if I want a shot a hitting my goal of less than $2,350 in average monthly total expenses. I mentioned in my 2014 goals post that I'm changing the way I calculate my expenses and savings. I usually save for expenses like gifts, property taxes, car insurance, travel, and more each month and some of those categories were counted as savings, even though they were earmarked to be spent. With the new year I'm now counting all of those savings categories as expenses rather than savings.

Total expenses for the month came in at $2,680.53 which was about $6.00 higher than January, so I'd call it flat month to month. The expense categories I'm focusing on for the year continue to be my food expenses, both groceries and restaurants. Groceries did a lot better than in January and just barely tallied over my $200 per month target at $209.22. Restaurants came in well under my $110 target at just $82.39 which I'm very happy about. Despite the fairly good job I did with my food expenses compared to February, total expenses were pretty much flat thanks to $47 being spent at bars and $40 for my gym membership. I don't go out to bars all that often so occasionally spending $50 is fine by me, but the gym membership cost will be recurring. Although that goes in line with my goal to improve my overall fitness by losing weight, specifically fat, and gaining muscle. I'm still well over my $2,350 target by about $300 so I'm not sure if there's even a realistic chance of hitting that goal. That's a shame since it's only February and one of my goals is already shot. There's not a whole lot of wiggle room in my budget but there's still some areas I can cut; namely miscellaneous and food spending.

Passive income expense coverage was pretty solid considering the relatively high expenses and solid month of dividends. I received $224 in dividends during February and another $5 in interest bringing my potential retirement income to $229.29. That was good enough to cover 8.55% of my total expenses for the month. That almost doubled February 2013's 4.89% mark. My FI Income, monthly income based on the 30 year US Treasury bond yield of 3.59% using my net worth excluding traditional retirement accounts, came in at $690.81 which covered 25.77% of my expenses from February.

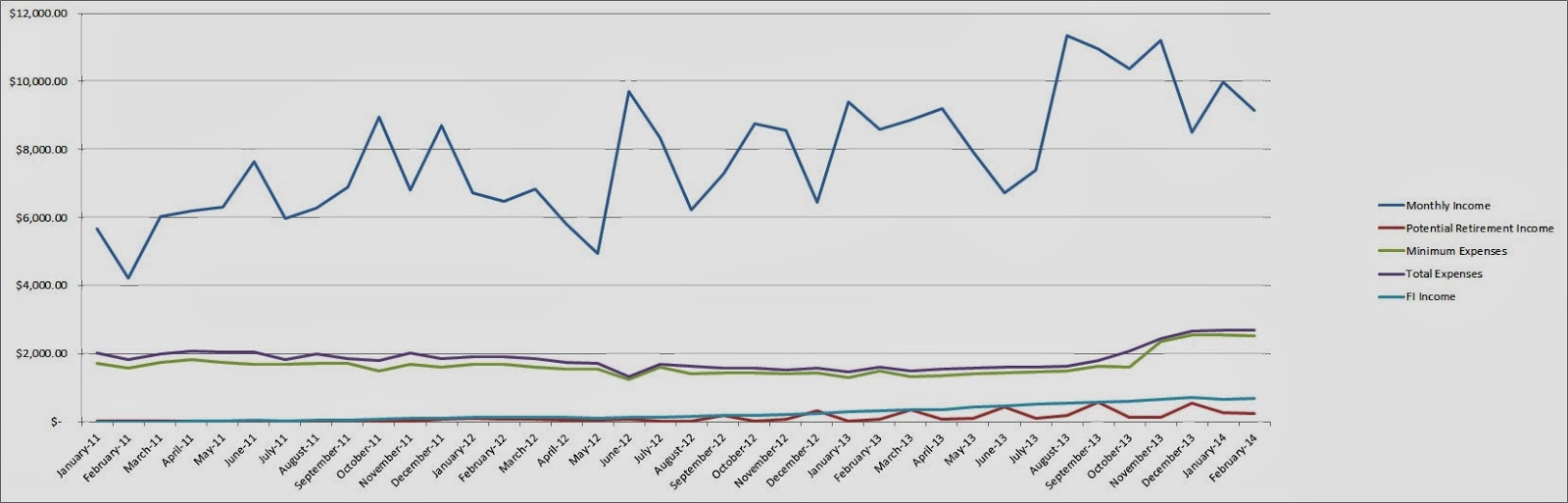

*Minimum Expenses are only the expenses related to rent, utilities, car, food, minimum payment on debt and other necessities. In other words, the required amount of replacement income I would need for financial independence.

*Total Expenses are the total monthly outflow of money.

*Potential Retirement Income is income received from dividends, interest, cash back from credit card purchases and any other source of income not related to my job.

*FI Income is my liquid net worth invested at the 30 year treasury bond yield at the end of each month divided by 12 to get monthly income.

*Savings that is earmarked to be spent.

I've updated my Progress page to reflect February's changes.

Also, I'm starting a newsletter that I hope to get going over the next month or two so go on and be the first to sign up to receive new posts to your email and newsletter!

How did you do on your budget for the month? Is there anything you're going to focus more on in March?

February's spending didn't go as well as I'd have liked. Nothing really stood out as being excessive and the total expenses came in right in line with January's spending. I need to find a way to start cutting some expenses if I want a shot a hitting my goal of less than $2,350 in average monthly total expenses. I mentioned in my 2014 goals post that I'm changing the way I calculate my expenses and savings. I usually save for expenses like gifts, property taxes, car insurance, travel, and more each month and some of those categories were counted as savings, even though they were earmarked to be spent. With the new year I'm now counting all of those savings categories as expenses rather than savings.

Total expenses for the month came in at $2,680.53 which was about $6.00 higher than January, so I'd call it flat month to month. The expense categories I'm focusing on for the year continue to be my food expenses, both groceries and restaurants. Groceries did a lot better than in January and just barely tallied over my $200 per month target at $209.22. Restaurants came in well under my $110 target at just $82.39 which I'm very happy about. Despite the fairly good job I did with my food expenses compared to February, total expenses were pretty much flat thanks to $47 being spent at bars and $40 for my gym membership. I don't go out to bars all that often so occasionally spending $50 is fine by me, but the gym membership cost will be recurring. Although that goes in line with my goal to improve my overall fitness by losing weight, specifically fat, and gaining muscle. I'm still well over my $2,350 target by about $300 so I'm not sure if there's even a realistic chance of hitting that goal. That's a shame since it's only February and one of my goals is already shot. There's not a whole lot of wiggle room in my budget but there's still some areas I can cut; namely miscellaneous and food spending.

Passive income expense coverage was pretty solid considering the relatively high expenses and solid month of dividends. I received $224 in dividends during February and another $5 in interest bringing my potential retirement income to $229.29. That was good enough to cover 8.55% of my total expenses for the month. That almost doubled February 2013's 4.89% mark. My FI Income, monthly income based on the 30 year US Treasury bond yield of 3.59% using my net worth excluding traditional retirement accounts, came in at $690.81 which covered 25.77% of my expenses from February.

*Minimum Expenses are only the expenses related to rent, utilities, car, food, minimum payment on debt and other necessities. In other words, the required amount of replacement income I would need for financial independence.

*Total Expenses are the total monthly outflow of money.

*Potential Retirement Income is income received from dividends, interest, cash back from credit card purchases and any other source of income not related to my job.

*FI Income is my liquid net worth invested at the 30 year treasury bond yield at the end of each month divided by 12 to get monthly income.

| Category | Amount |

|---|---|

| Paycheck | $7,191.22 |

| Expense Check | $1,943.40 |

| TOTAL | $9,134.62 |

| Category | Budgeted Amount | Actual Amount | Subtotal |

|---|---|---|---|

| Mortgage | $911.84 | $911.84 | |

| House Insurance | $127.92 | $127.92 | |

| Property Taxes | $371.08 | $371.08 | |

| Gas | $175.00 | $160.28 | |

| Car Insurance | $163.25 | $163.25 | |

| Groceries | $200.00 | $209.22 | |

| Restaurants | $100.00 | $82.39 | |

| Bars | $0.00 | $47.00 | |

| Debt Payment (Fridge) | $300.00 | $300.00 | |

| Cell Phone | $10.81 | $10.81 | |

| Gym Membership | $40.00 | $40.00 | |

| Miscellaneous | $55.00 | $106.74 | |

| Gifts* | $75.00 | $75.00 | |

| Car Maint./Repair* | $75.00 | $75.00 | |

| Trip* | $0.00 | $0.00 | |

| EXPENSES SUBOTAL | $2,680.53 | ||

| Emergency Fund | $1,500.00 | $1,500.00 | |

| Investing | $5,029.72 | $4,954.09 | |

| SAVINGS SUBTOTAL | $6,454.09 | ||

| TOTAL | $9,134.62 |

I've updated my Progress page to reflect February's changes.

Also, I'm starting a newsletter that I hope to get going over the next month or two so go on and be the first to sign up to receive new posts to your email and newsletter!

How did you do on your budget for the month? Is there anything you're going to focus more on in March?

Looks like another solid month. I wish I could get my grocery budget that low. February was a great month for me, mostly because I finished my taxes and found I owed much less than expected. Great progress!

ReplyDeleteZach,

DeleteThe grocery spending is for myself only for about 75% of each month and since you have a family I'd expect yours to be higher. That's why I feel mine is a bit too high. It was great when I was laid off because I ended up cooking 95% of our meals so it was cheaper because of cooking, cheaper because of economies of scale (cooking for two is a lot cheaper the cooking for one), and not to mention a whole lot healthier.

I hope that will be the case for us as well because I expect we'll be paying around $700. I'll have to play around with my withholdings throughout the year to try and get it closer to $0 but it's difficult forecasting the effects of dividends, ESPP sales, and income from the blog.

Thanks for stopping by!

Pretty stout performance in February. I know you've written a few articles for Seeking Alpha recently, so has any income from that been realized yet?

ReplyDeleteBest of luck in starting a newsletter as well!

w2r,

DeleteI've earned a bit from the articles but SA only pays out quarterly so nothing has hit my bank account yet. Although I should see my first income from there in April. I really need to start getting a few more articles written there.

I'm really looking forward to the newsletter and some other ideas I have for the blog. It's a pretty exciting time and I just wish I had more time to write. There's a lot of ideas floating around my head for articles but it's been difficult recently to get some written up.

Thanks for stopping by!

PIP,

ReplyDeleteGreat YOY increase in the dividends. Your monthly savings rate is off the chart. Keep saving aggressively and investing conservatively and you will gain FI in no time!

MDP,

DeleteI was quite surprised to see such a big jump. I knew I had invested a lot of capital over the last year but I hadn't really paid attention to the dividends I could expect to receive each month. Not soon enough, but at least I'm working towards it!

Thanks for stopping by!

Hi PIP,

ReplyDeleteI am always amazed about your big paycheck!

That´s awesome!!

And at the beginning of your post, you write:

" I'm a big proponent of tracking every single penny that comes into your hands if you're really wanting to make a change to your finances"

I can only agree!

20 years ago, I have tracked every penny.

Even the money of my wallet :-)

That was a lot of work - but it also has made a lot of fun.

Best regards

D-S

D-S,

DeleteThe income sure is nice and really helps to put the journey towards FI into overdrive.

Especially when you're starting out I think you have to track every penny. I admit that I don't keep as close tabs on it now and my expenses don't really vary all that much from month to month, but I still track every penny. I just don't keep my spreadsheet as up to date as I used to throughout the month. Plus when you track all of those pennies you get to find out exactly where you money is going and can do all sorts of fun analysis on it if you're a math nerd like me.

Thanks for stopping by!

That's one of the coolest line graphs I've seen in personal finance. Great stuff! I love seeing everything pulling up off the bottom line: here's to hoping you go parabolic in the near future!

ReplyDeleteDone by Forty,

DeleteThanks and I'm glad you like it. I think it really shows where you stand as far as income/expenses/savings/passive income. I'd love to see the passive income go parabolic but I don't think that'll be happening anytime soon. That's the problem with trying to reach FI/ER quickly, you just don't have the time for compounding to really do it's work as invested capital does most of the heavy lifting. Either way though when I reach FI, I won't really care how I got there.

Thanks for stopping by!

Pursuit,

ReplyDeleteAnother blockbuster month! That income is really stellar, and it looks like you've done a fantastic job keeping lifestyle inflation under control.

Keep up the great work!

Best wishes.

DM,

DeleteLuckily it comes pretty natural to me and I don't have to fight lifestyle inflation that much. I much prefer a very simple life.

Thanks for stopping by!

Wow, insurances sure are expensive in the U.S!

ReplyDeleteYour car insurance is triple mine in the UK, and we British always complain how cheap everything is over there.

It is great to see how other peoples spending stacks up against your own, so you can get ideas where you can save. I also noticed your debt repayment of $300, if you could get rid of that you would be almost at your target.

Just one question if you don't mind. You show your pay check and expenses, but with the number of visitors you get to your blog, do you receive any additional income from there?

Keep up with informing everyone how you are doing

FI UK

FI UK,

DeleteInsurances vary a whole lot across the US. Here in Texas property taxes, homeowners insurance and auto insurance is pretty expensive. Although we don't have a state income tax like most of the states here do. Also the car insurance is for my wife and I so it's really for 2 people/2 cars. It's still expensive though.

I've thought about just paying off the debt but it's at 0% interest and we'll just be getting rid of one debt and then applying this payment to the others. We had very little furniture and almost no appliances when we bought our house so we had to go and buy a fridge, living room set and bedroom set. Everything is at 0% interest for varying lengths of time but the fridge will be the first to get paid off and then we'll just put that $300 towards the next debt. If the markets continue to increase and I can't find any good rental opportunities then we'll probably just take some of the savings to pay off everything and be completely debt free.

I do earn money here from Adsense and also from my articles at Seeking Alpha. I only earn about $30 per month from Adsense and they only pay the month after you cross the $100 total. Seeking Alpha only pays quarterly. So I'll only mention those incomes in the months that I actually receive payment. If it starts to become pretty significant payouts then I might break it down to monthly earnings even if it's not paid yet.

Thanks for stopping by!

Great job! My favorite part is that you have such great income but still pinch pennies and look for every way to improve on your expenses. This is how you get filthy rich. You are an inspiration and I truly appreciate you sharing these income updates with the world.

ReplyDeleteRyan,

DeleteAfter going through my layoff and finding out what's really important to me, hint it's not sitting in a cubicle all day, I feel blessed to have found such a high paying job. Of course it comes with it's own issues as I have to be gone from home and family but I feel that the best way to make up for that lost time is to save/invest as much as possible to give my wife and I the freedom to do what we want.

I'm glad that you find my blog inspirational. If I can help convince or motivate one person to start taking control of their finances and investing then I feel happy.

Thanks for stopping by!

Great breakdown of your expenses. You are doing significantly better than I am able to do on groceries. I also noticed the lack of utilities which is another place I have been getting hammered, do you only pay on certain months? Anyways congrats on keeping the expenses so low, it's really motivating to see someone who has been able to have such good consistency over a long period. Take care.

ReplyDeleteDividendasaur,

DeleteMy wife pays for the utilities. Since I work away from home and am gone for around 3 weeks each month it's easiest for my wife and I to keep separate finances. The expenses above are only the ones I cover. So it's not a true picture of the total household expenses but it's around a 2:1 ratio. My total food bill is still way too high though. Considering I'm paying mainly for myself throughout the month $300+ seems really high. The best part about keeping track for a while is that your baseline expenses get into a groove. For the most part they don't change that much whether I track my spending throughout the month or not.

Thanks for stopping by!

Awesome month! That's a lot of bacon you're bringing home and it's wonderful to see how disciplined you are in saving most of it.

ReplyDeleteGreat progress on the passive income as well, compared to this time last year!

FI Fighter,

DeleteI might be tempted to spend more of my savings on actual bacon though. It was a really good month and I'm blessed to make as high of an income as I do. There's a lot of people that I meet through work with the same schedule, or lack there of, that I have but spend all their money on toys. I understand wanting to do so but for me I'd rather have a fat portfolio than garage of 4-wheelers. Especially since I know they don't get to ride them that often because they're away from home like me. Personally I say take care of the finances first and then when you reach FI you can easily work another 6-12 months to spend only on the toys.

Thanks for stopping by!

Another great month, well done!!!

ReplyDeleteAm I reading that correctly? You're investing almost $5,000 per month but also have $300 debt payment?

Mark

Mark,

DeleteYeah, you caught that. The $300 debt payment is for our refrigerator when we bought our house. It's interest free for 12 months and we've got it set up to be paid off before the 11th month. I've contemplated just paying it off but the 0% interest has kept me from doing so. The $5k hasn't been invested yet but it's earmarked for investment, specifically a rental property. If over the next few months we don't find something intriguing then I'll start applying extra savings towards the debt to get that done with. Luckily with my cash flow that'll be a one and done type thing.

Thanks for stopping by!

It's gotta be real motivating to see your FI income starting to cover more and more of your total expenses. I need to start tracking things this way, I think it would give me that extra boost to really focus on FI income.

ReplyDeleteFirst Million,

DeleteIt's pretty cool to see the FI income moving on up to cover more and more of my expenses. If I can get things going better with lowering expenses it's a double whammy of progress. It's really motivating and that's another reason why I like to track as much data as possible. The more data you have the more fun charts you can make.

Thanks for stopping by!

Wow that is a big paycheck - nice! And even though you're getting paid well you're very frugal. Inspiring.

ReplyDelete