Church & Dwight (CHD) Dividend Stock Analysis

We all know about Johnson & Johnson, Proctor & Gamble, Clorox, Colgate-Palmolive and the like and what they have done in terms of building wealth and continually producing rising dividend streams. While I still expect continued growth in all of the companies as well as their dividends, a lot of their growth has been in the past and slower growth should be expected given their already massive sizes. So what's an investor to do if they want to find a similar business model that can potentially provide higher overall growth than their counterparts. One potential idea is the much smaller Church & Dwight Company, Inc. (CHD). Church & Dwight Co. closed trading on Friday, December 13th at $65.76, offering a current yield of 1.70%.

Company Background (sourced from Yahoo! Finance):

Church & Dwight Co., Inc., together with its subsidiaries, develops, manufactures, and markets a range of household, personal care, and specialty products under various brand names in the United States and internationally. The company operates in three segments: Consumer Domestic, Consumer International, and Specialty Products Division (SPD). The Consumer Domestic segment offers household products, such as baking soda, carpet and cat litter deodorizers, clumping cat litters, washing soda, fabric softeners, dryer cloths, aluminum and stainless steel cleaners, daily shower cleaners, fine fabric washes, cleaning products, dishwashing boosters, and bathroom and toilet bowl cleaners, as well as powder, liquid, and unit dose laundry detergents; and personal care products, which comprise toothpastes, home pregnancy and ovulation test kits, deodorants and antiperspirants, toothbrushes, shampoos, laxatives, dietary supplements, depilatories, lotions, creams, waxes, oral analgesics, nasal saline moisturizers, and condoms and vibrating products. The Consumer International segment markets and sells various personal care, over-the-counter, and household products in international markets, including Canada, France, Australia, the United Kingdom, Mexico, Brazil, and China. The SPD segment offers specialty chemicals, such as performance grade sodium bicarbonate, potassium carbonate, and potassium bicarbonate; animal nutrition products, including feed grade sodium bicarbonate, rumen fermentation enhancers, feed grade potassium carbonate, rumen bypass fat and lysine, essential fatty acids, and natural sodium sesquicarbonate; and specialty cleaners for commercial, professional, and industrial applications. The company sells its products through supermarkets, mass merchandisers, wholesale clubs, drugstores, convenience stores, dollar and pet stores, and other specialty stores, as well as Websites. Church & Dwight Co., Inc. was founded in 1846 and is headquartered in Ewing, New Jersey.

DCF Valuation:

Analysts expect Church & Dwight to grow earnings 11.43% per year for the next five years and I've assumed they can grow at 2/3 of that, or 7.62%, for the next 3 years and continue to grow at 3.50% per year thereafter. Running these numbers through a three stage DCF analysis with a 10% discount rate yields a fair value price of $63.81. This means the shares are trading at a 3.1% premium to the discounted cash flow analysis.

Graham Number:

The Graham Number valuation method was conceived of by Benjamin Graham, the father of value investing, and calculates the maximum price one should pay for a company given the earnings and book value. Church & Dwight earned $2.71 per share in the last twelve months and has a current book value per share of $16.08. The Graham Number is calculated to be $31.31, suggesting that CHD is overvalued by 110.0%.

Average High Dividend Yield:

Church & Dwight's average high dividend yield for the past 5 years is 1.65% and for the past 10 years is 1.20%. This gives target prices of $67.72 and $93.23 respectively based on the current annual dividend of $1.12. Normally I'll use one or both of the 5 or 10 year average high dividend yields in my fair value calculation; however, I'm making an exception on CHD and will use the 3 year average of 2.08% with a target price of $53.73 and the 5 year average. This gives a target entry price of $60.73. Church & Dwight is trading at an 8.3% premium to this price.

Average Low PE Ratio:

Church & Dwight's average low PE ratio for the past 5 years was 16.6 and for the past 10 years was 17.2. This corresponds to a price per share of $51.42 and $53.29 respectively based off the analyst estimate of $2.80 per share for fiscal year 2013. Both PE ratios are relatively close so I'll use the average of the two for my target entry price. This corresponds to a target price of $52.35 with a 16.9 P/E ratio. Church & Dwight is trading at a 25.6% premium, suggesting that it's overvalued.

Average Low P/S Ratio:

Church & Dwight's average low PS ratio for the past 5 years is 1.83 and for the past 10 years is 1.54. This corresponds to a price per share of $44.03 and $37.02 respectively based off the analyst estimate for revenue growth from FY 2012 to FY 2013. The price targets don't include effects due to potential share buybacks, rather it's just based off the analyst estimate for revenue and growth, to be a bit conservative. Currently, their current PS ratio is 2.86 on a trailing twelve months basis. Once again I'll use the average of the two ratios in my target entry price calculation, giving a target price of $40.53. Church & Dwight is currently trading for a 62.3% premium to this price.

Gordon Growth Model:

The Gordon Growth Model is a quick way to calculate the fair value of a company using the current dividend, the expected dividend growth rate, and your required rate of return or discount rate. Assuming a constant 8.00% dividend growth rate and a discount rate of 10.00%, the GGM valuation method yields a fair price of $56.00. Church & Dwight is currently trading at a 17.4% premium to this price, suggesting that it's overvalued.

Dividend Discount Model:

For the DDM, I assumed that Church & Dwight will be able to grow dividends for the next 5 years at the lowest of the 1, 3, 5 or 10 year growth rates or 15%. In this case that would be 15%. After that I assumed they can continue to raise dividends for 3 years at 75% of 15%, or 11.25%, and in perpetuity at 6.00%. The dividend growth rates are based off fiscal year payouts and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on the DDM, Church & Dwight is worth $40.96, meaning it's overvalued by 60.6%.

PE Ratios:

Church & Dwight's trailing PE is 24.27 and it's forward PE is 21.21. The PE3 based on the average earnings for the last 3 years is 26.77. I like to see the PE3 be less than 15 which CHD is currently well over. Compared to it's industry, CHD seems to be overvalued versus CLX (21.60) and PG (20.93). All comparisons are on a TTM basis. Church & Dwight's PEG for the next 5 years is currently at 2.05 which has them undervalued versus CLX (2.73) and PG (2.30). A lower PEG ratio is better because it means you're paying less for every dollar of growth the company achieves. While CHD is overvalued on a TTM PE basis, due to their much smaller size and higher expected growth, their PEG ratio is much lower than their larger competitors.

Fundamentals:

Church & Dwight's gross margin for FY 2011 and FY 2012 were 44.2% and 44.2% respectively. They have averaged a 41.2% gross profit margin over the last 10 years. Their net income margin for the same years were 11.3% and 12.0%. Since 2003 their net income margin has averaged 8.7%. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. While CHD is behind my typical gross margin target, they're still above the 40% threshold. On the net profit margin front they have been over 10% for the last three fiscal years and higher than the 7% level in all but one year. Since each industry is different and allows for different margins, I feel it's prudent to compare Church & Dwight to its industry. For FY 2012, CHD captured 99.8% of the gross margin for the industry but a whopping 193.5% of the net income margin. On a TTM basis, Church & Dwight's gross profit margin was 45% while CLX's was 43% and PG was 50%. Church & Dwight's net profit margin was 12.0% with CLX earning 10.2% and PG earning 13.6%. Against their larger and direct competitors, Church & Dwight is doing much better at turning sales into both gross and net profit which can afford them to withstand another slowdown in the global economy as 40% of their revenues come from "value" brands".

Share Buyback:

Church & Dwight has not been a serial share repurchased with only 2 years of decreasing shares outstanding since FY 2001 closed. Since FY 2002 management has increased the share count by 13.8% for an aveage annual increase of 1.3%. However, during FY 2012 management announced a $300 million share repurchase plan as a way to return excess cash to shareholders. The share count did decrease 2.1% during FY 2012 as part of the buyback plan and through 3Q 2013 has decreased another 1.2%. I'd like to see the share buyback plan continue on as share buybacks are generally more flexible compared to a dividend program. If a company slows their buyback during a year due to overvaluation of the shares or some hiccups in company operations, I have no issue. However, if they wanted to reduce the dividend then I know a lot of investors will be jumping ship, myself included. By decreasing the share count management can return excess earnings to owners in a tax efficient manner.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Church & Dwight is a dividend contender with 17 consecutive years of dividend increases. They have increased the dividend at a 16.7%, 53.4%, 45.8%, and 26.9% rate over the last 1, 3, 5, and 10 year periods respectively. Dividend increases are based off fiscal year payouts and don't necessarily correspond to annual payouts. Obviously those 40%+ dividend increases won't be able to continue, but a growth in the neighborhood of 10-15% is very much possible if the EPS growth rate comes to light. Their payout ratio based off EPS has averaged 18.4% over the last 10 years but was a much heftier 39.2% for FY 2012.

Church & Dwight's cash flow has consistently increased across both operating cash flow, free cash flow, and free cash flow after dividends were paid. Over the last 5 years they've been able to turn approximately 78% of their operating cash flow into free cash flow and 63% of their operating cash flow into free cash flow after paying the dividend. Their free cash flow has increased from $75.3 M in 2002 to $449.1 M in 2012 for an average annual increase of 19.6%. Their free cash flow after dividends has increased as well from $63.4 M to $314.6 M over the same time for an average annual increase of 17.4%. The free cash flow payout ratio has averaged 14.6% over the last 10 years. While it increased to approximately 30% in FY 2012, it's still comfortably below the EPS payout of 39%.

Return on Equity and Return on Capital Invested:

Church & Dwight's ROE has averaged a solid 16.0% over the last 10 years while their ROCI has averaged 10.4%. Their ROE has been fairly consistent too ranging from a high of 18.5% to a low of 15.2%. ROCI has shown a nice rising trend, with a low of 6.8% and a high of 13.5%. Despite an overall increase in total debt, their debt-to-equity ratio has fallen from 0.91 in FY 2003 to 0.12 in FY 2012 due to rising equity levels. Subsequently, their debt-to-capitalization ratio has fallen as well from 43.0% in FY 2003 to just 10.9% in FY 2012. Things are on the right track here as I much prefer the companies I invest in to have low debt levels as the more leverage they use the higher the overall risk should a slowdown in their operations force their hand. Being a consumer staples company though, even in the worst of times you're still going to have people buying your products. Who doesn't still need detergent, toothpaste and the like no matter what the economy is doing. For consumer staples companies though, having lower debt levels can allow you to make strategic acquisitions and expansions when other companies might be struggling as you can use debt to help finance the acquisition.

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how Church & Dwight has done on that front. Their revenue growth since the end of FY 2002 has been excellent with a 10.8% annual increase growing their revenue from $1,047 M to $2,922 M in FY 2012. Their net income growth has far outpaced revenue growth with a 18.0% annual growth rate increasing net income from $66.7 M to $349.8 M. This has led to the net profit margin increasing from 6.4% in FY 2002 all the way up to 12.0% in FY 2012. Management has made it a goal to further increase their margins by decreasing overhead expenses and growing their sales.

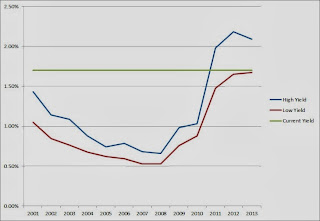

Forecast:

The chart shows the historical high and low prices since 2001 and the forecast based on the average PE ratios and the expected EPS values. I have also included a forecast based off a PE ratio that is only 75% of the average low PE ratio. I like to the look to buy at the 75% Low PE price or lower to provide for a larger margin of safety, although this price doesn't usually come around very often. In the case of Church & Dwight, the target low PE is 16.9 and the 0.75 * PE is 12.7. This corresponds to an entry price of $47.29 based off the expected earnings for FY 2013 of $2.80, with a 75% target price of $34.83. Currently Church & Dwight is trading at a $27.19 premium to the 75% low PE target price and a $13.41 premium to the low PE price. Seeing as how FY 2013 will be ending in less than 2 weeks, let's take a look at the price targets for FY 2014. Analysts expect EPS to come in at $3.10 for FY 2014 which gives a low PE target price of $52.35 and a 75% target price of $38.57. The current price line in the chart intersects the average PE price line in FY 2015 so you're currently paying up for about 2 years of growth if you buy near these levels.

Conclusion:

The average of all the valuation models gives a target entry price of $49.38 which means that Church & Dwight is currently trading at a 33% premium to the target entry price. I've also calculated it with the highest and lowest valuation methods thrown out. In this case, the DCF and Graham Number valuations are removed and the new average is $50.11. Church & Dwight is trading at a 31% premium to this price as well.

Assuming that Church & Dwight can grow their earnings and dividends at the rates that I assumed, you're looking at solid returns over the next 10 years at current prices. In 2022, EPS would be $6.17 and slapping an average PE of 18.9 gives a price of $116.39. Over the next 5 years you'd also receive $23.85 per share in dividends for a total return of 113.3%% which is good for a 7.9% annualized rate if you purchase at the current price. If you purchase at the target entry price of $50.11, your projected 10 year total return jumps to 179.9% for an annualized return of 10.8%.

According to Yahoo! Finance the 1 year target estimate is at $70.41 suggesting about 7.1% upside from Friday's closing price. Followers at The Motley Fool have CHD rated as a 4 out of 5 stock, meaning they're bullish on the company. However, Morningstar has them rated as a 2 star stock suggesting that it's trading above their fair value estimate.

You might not know any of Church & Dwight's products off the top of your head, but rest assured you'll definitely recognize the names. Their 8 power brands are Arm & Hammer, OxiClean, Spinbrush, First Response, Nair, Orajel, Xtra, and Trojan. The Arm & Hammer brand is in more aisles of the grocery store than any other brand and is currently in 9 out of 10 households in America. Their 8 "Power Brands" made up 80% of their consumer sales in FY 2012. Their overall product portfolio is made up of 60% "premium" brands and 40% "value" brands which should allow them to weather any slide in the economy well as consumers switch to the value branded products and still maintain solid sales as they switch back to premium products when the economy improves.

As part of their 10 key initiatives to drive investor return, they are expanding internationally. From 2000-2012, CHD grow from a US-centric company to now acquiring 18% of their revenues in foreign countries. International revenue growth has been a bit lower than I expected, but 5%+ from 2007 to 2012 is still at a comfortable level. Acquisitions is another part of their growth plan and given their low debt levels and high FCF conversion I'd expect to see another acquisition to be in the works over the next year. In 2012 CHD purchased Avid Health, Inc. which was a leader in the adult and children gummy vitamin business.

One concern with CHD, as well as most other consumer staples companies, is that their largest customers tend to make up a large amount of revenues. From 2010 through 2012, Walmart accounted for 23%, 23%, and 24% of their sales. While this is a bit of a concern since one customer deciding it didn't want to carry the CHD lineup could potentially disrupt 20%+ of their revenues.

The advantage that a Church & Dwight has over it's larger counterparts is that there's plenty of room for growth and for acquisitions to make much more meaningful impacts on the bottom line. A billion dollar brand coming to CHD would increase revenues by 34% at CHD; however, PG acquiring a billion dollar brand only increases revenues 1.2%. I really like the consume staples sector for consistent dividend increases year in and year out as the demand for their products rarely dips by significant levels. Mid-cap companies can offer the best of both worlds between growth companies and established moats as their presence and brands are already in place but there's still significant room to expand and for acquisitions to be accretive to earnings. I'm going to really be watching to see how CHD continues to do on international expansion as that will be a big driver of growth along with potential acquisitions.

Church & Dwight is due for a dividend increase with their next payment in early March and I'd like to pick up shares of Church & Dwight, but just not at these levels. Based on their results thus far this year, I'd expect to see the quarterly dividend increased from $0.28 to either $0.31 (10.7%) or $0.32 (14.3%). This would give a yield at current prices around 1.93%. I'll be looking to initiate a position if shares dip to the $58-60 level.

To check out more reports check out my Stock Analysis page.

Remember if you haven't yet done so, sign up for the free Simply Investing Course giveaway. The entry period ends on Saturday, December 21st.

What do you think about Church & Dwight as a DG investment? How do you think the long-term dividend growth prospects are?

Company Background (sourced from Yahoo! Finance):

Church & Dwight Co., Inc., together with its subsidiaries, develops, manufactures, and markets a range of household, personal care, and specialty products under various brand names in the United States and internationally. The company operates in three segments: Consumer Domestic, Consumer International, and Specialty Products Division (SPD). The Consumer Domestic segment offers household products, such as baking soda, carpet and cat litter deodorizers, clumping cat litters, washing soda, fabric softeners, dryer cloths, aluminum and stainless steel cleaners, daily shower cleaners, fine fabric washes, cleaning products, dishwashing boosters, and bathroom and toilet bowl cleaners, as well as powder, liquid, and unit dose laundry detergents; and personal care products, which comprise toothpastes, home pregnancy and ovulation test kits, deodorants and antiperspirants, toothbrushes, shampoos, laxatives, dietary supplements, depilatories, lotions, creams, waxes, oral analgesics, nasal saline moisturizers, and condoms and vibrating products. The Consumer International segment markets and sells various personal care, over-the-counter, and household products in international markets, including Canada, France, Australia, the United Kingdom, Mexico, Brazil, and China. The SPD segment offers specialty chemicals, such as performance grade sodium bicarbonate, potassium carbonate, and potassium bicarbonate; animal nutrition products, including feed grade sodium bicarbonate, rumen fermentation enhancers, feed grade potassium carbonate, rumen bypass fat and lysine, essential fatty acids, and natural sodium sesquicarbonate; and specialty cleaners for commercial, professional, and industrial applications. The company sells its products through supermarkets, mass merchandisers, wholesale clubs, drugstores, convenience stores, dollar and pet stores, and other specialty stores, as well as Websites. Church & Dwight Co., Inc. was founded in 1846 and is headquartered in Ewing, New Jersey.

DCF Valuation:

Analysts expect Church & Dwight to grow earnings 11.43% per year for the next five years and I've assumed they can grow at 2/3 of that, or 7.62%, for the next 3 years and continue to grow at 3.50% per year thereafter. Running these numbers through a three stage DCF analysis with a 10% discount rate yields a fair value price of $63.81. This means the shares are trading at a 3.1% premium to the discounted cash flow analysis.

Graham Number:

The Graham Number valuation method was conceived of by Benjamin Graham, the father of value investing, and calculates the maximum price one should pay for a company given the earnings and book value. Church & Dwight earned $2.71 per share in the last twelve months and has a current book value per share of $16.08. The Graham Number is calculated to be $31.31, suggesting that CHD is overvalued by 110.0%.

Average High Dividend Yield:

Church & Dwight's average high dividend yield for the past 5 years is 1.65% and for the past 10 years is 1.20%. This gives target prices of $67.72 and $93.23 respectively based on the current annual dividend of $1.12. Normally I'll use one or both of the 5 or 10 year average high dividend yields in my fair value calculation; however, I'm making an exception on CHD and will use the 3 year average of 2.08% with a target price of $53.73 and the 5 year average. This gives a target entry price of $60.73. Church & Dwight is trading at an 8.3% premium to this price.

Church & Dwight's average low PE ratio for the past 5 years was 16.6 and for the past 10 years was 17.2. This corresponds to a price per share of $51.42 and $53.29 respectively based off the analyst estimate of $2.80 per share for fiscal year 2013. Both PE ratios are relatively close so I'll use the average of the two for my target entry price. This corresponds to a target price of $52.35 with a 16.9 P/E ratio. Church & Dwight is trading at a 25.6% premium, suggesting that it's overvalued.

Average Low P/S Ratio:

Church & Dwight's average low PS ratio for the past 5 years is 1.83 and for the past 10 years is 1.54. This corresponds to a price per share of $44.03 and $37.02 respectively based off the analyst estimate for revenue growth from FY 2012 to FY 2013. The price targets don't include effects due to potential share buybacks, rather it's just based off the analyst estimate for revenue and growth, to be a bit conservative. Currently, their current PS ratio is 2.86 on a trailing twelve months basis. Once again I'll use the average of the two ratios in my target entry price calculation, giving a target price of $40.53. Church & Dwight is currently trading for a 62.3% premium to this price.

Gordon Growth Model:

The Gordon Growth Model is a quick way to calculate the fair value of a company using the current dividend, the expected dividend growth rate, and your required rate of return or discount rate. Assuming a constant 8.00% dividend growth rate and a discount rate of 10.00%, the GGM valuation method yields a fair price of $56.00. Church & Dwight is currently trading at a 17.4% premium to this price, suggesting that it's overvalued.

Dividend Discount Model:

For the DDM, I assumed that Church & Dwight will be able to grow dividends for the next 5 years at the lowest of the 1, 3, 5 or 10 year growth rates or 15%. In this case that would be 15%. After that I assumed they can continue to raise dividends for 3 years at 75% of 15%, or 11.25%, and in perpetuity at 6.00%. The dividend growth rates are based off fiscal year payouts and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on the DDM, Church & Dwight is worth $40.96, meaning it's overvalued by 60.6%.

PE Ratios:

Church & Dwight's trailing PE is 24.27 and it's forward PE is 21.21. The PE3 based on the average earnings for the last 3 years is 26.77. I like to see the PE3 be less than 15 which CHD is currently well over. Compared to it's industry, CHD seems to be overvalued versus CLX (21.60) and PG (20.93). All comparisons are on a TTM basis. Church & Dwight's PEG for the next 5 years is currently at 2.05 which has them undervalued versus CLX (2.73) and PG (2.30). A lower PEG ratio is better because it means you're paying less for every dollar of growth the company achieves. While CHD is overvalued on a TTM PE basis, due to their much smaller size and higher expected growth, their PEG ratio is much lower than their larger competitors.

Fundamentals:

Church & Dwight's gross margin for FY 2011 and FY 2012 were 44.2% and 44.2% respectively. They have averaged a 41.2% gross profit margin over the last 10 years. Their net income margin for the same years were 11.3% and 12.0%. Since 2003 their net income margin has averaged 8.7%. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. While CHD is behind my typical gross margin target, they're still above the 40% threshold. On the net profit margin front they have been over 10% for the last three fiscal years and higher than the 7% level in all but one year. Since each industry is different and allows for different margins, I feel it's prudent to compare Church & Dwight to its industry. For FY 2012, CHD captured 99.8% of the gross margin for the industry but a whopping 193.5% of the net income margin. On a TTM basis, Church & Dwight's gross profit margin was 45% while CLX's was 43% and PG was 50%. Church & Dwight's net profit margin was 12.0% with CLX earning 10.2% and PG earning 13.6%. Against their larger and direct competitors, Church & Dwight is doing much better at turning sales into both gross and net profit which can afford them to withstand another slowdown in the global economy as 40% of their revenues come from "value" brands".

Share Buyback:

Church & Dwight has not been a serial share repurchased with only 2 years of decreasing shares outstanding since FY 2001 closed. Since FY 2002 management has increased the share count by 13.8% for an aveage annual increase of 1.3%. However, during FY 2012 management announced a $300 million share repurchase plan as a way to return excess cash to shareholders. The share count did decrease 2.1% during FY 2012 as part of the buyback plan and through 3Q 2013 has decreased another 1.2%. I'd like to see the share buyback plan continue on as share buybacks are generally more flexible compared to a dividend program. If a company slows their buyback during a year due to overvaluation of the shares or some hiccups in company operations, I have no issue. However, if they wanted to reduce the dividend then I know a lot of investors will be jumping ship, myself included. By decreasing the share count management can return excess earnings to owners in a tax efficient manner.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Church & Dwight is a dividend contender with 17 consecutive years of dividend increases. They have increased the dividend at a 16.7%, 53.4%, 45.8%, and 26.9% rate over the last 1, 3, 5, and 10 year periods respectively. Dividend increases are based off fiscal year payouts and don't necessarily correspond to annual payouts. Obviously those 40%+ dividend increases won't be able to continue, but a growth in the neighborhood of 10-15% is very much possible if the EPS growth rate comes to light. Their payout ratio based off EPS has averaged 18.4% over the last 10 years but was a much heftier 39.2% for FY 2012.

Church & Dwight's cash flow has consistently increased across both operating cash flow, free cash flow, and free cash flow after dividends were paid. Over the last 5 years they've been able to turn approximately 78% of their operating cash flow into free cash flow and 63% of their operating cash flow into free cash flow after paying the dividend. Their free cash flow has increased from $75.3 M in 2002 to $449.1 M in 2012 for an average annual increase of 19.6%. Their free cash flow after dividends has increased as well from $63.4 M to $314.6 M over the same time for an average annual increase of 17.4%. The free cash flow payout ratio has averaged 14.6% over the last 10 years. While it increased to approximately 30% in FY 2012, it's still comfortably below the EPS payout of 39%.

Return on Equity and Return on Capital Invested:

Church & Dwight's ROE has averaged a solid 16.0% over the last 10 years while their ROCI has averaged 10.4%. Their ROE has been fairly consistent too ranging from a high of 18.5% to a low of 15.2%. ROCI has shown a nice rising trend, with a low of 6.8% and a high of 13.5%. Despite an overall increase in total debt, their debt-to-equity ratio has fallen from 0.91 in FY 2003 to 0.12 in FY 2012 due to rising equity levels. Subsequently, their debt-to-capitalization ratio has fallen as well from 43.0% in FY 2003 to just 10.9% in FY 2012. Things are on the right track here as I much prefer the companies I invest in to have low debt levels as the more leverage they use the higher the overall risk should a slowdown in their operations force their hand. Being a consumer staples company though, even in the worst of times you're still going to have people buying your products. Who doesn't still need detergent, toothpaste and the like no matter what the economy is doing. For consumer staples companies though, having lower debt levels can allow you to make strategic acquisitions and expansions when other companies might be struggling as you can use debt to help finance the acquisition.

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how Church & Dwight has done on that front. Their revenue growth since the end of FY 2002 has been excellent with a 10.8% annual increase growing their revenue from $1,047 M to $2,922 M in FY 2012. Their net income growth has far outpaced revenue growth with a 18.0% annual growth rate increasing net income from $66.7 M to $349.8 M. This has led to the net profit margin increasing from 6.4% in FY 2002 all the way up to 12.0% in FY 2012. Management has made it a goal to further increase their margins by decreasing overhead expenses and growing their sales.

Forecast:

Conclusion:

The average of all the valuation models gives a target entry price of $49.38 which means that Church & Dwight is currently trading at a 33% premium to the target entry price. I've also calculated it with the highest and lowest valuation methods thrown out. In this case, the DCF and Graham Number valuations are removed and the new average is $50.11. Church & Dwight is trading at a 31% premium to this price as well.

Assuming that Church & Dwight can grow their earnings and dividends at the rates that I assumed, you're looking at solid returns over the next 10 years at current prices. In 2022, EPS would be $6.17 and slapping an average PE of 18.9 gives a price of $116.39. Over the next 5 years you'd also receive $23.85 per share in dividends for a total return of 113.3%% which is good for a 7.9% annualized rate if you purchase at the current price. If you purchase at the target entry price of $50.11, your projected 10 year total return jumps to 179.9% for an annualized return of 10.8%.

According to Yahoo! Finance the 1 year target estimate is at $70.41 suggesting about 7.1% upside from Friday's closing price. Followers at The Motley Fool have CHD rated as a 4 out of 5 stock, meaning they're bullish on the company. However, Morningstar has them rated as a 2 star stock suggesting that it's trading above their fair value estimate.

You might not know any of Church & Dwight's products off the top of your head, but rest assured you'll definitely recognize the names. Their 8 power brands are Arm & Hammer, OxiClean, Spinbrush, First Response, Nair, Orajel, Xtra, and Trojan. The Arm & Hammer brand is in more aisles of the grocery store than any other brand and is currently in 9 out of 10 households in America. Their 8 "Power Brands" made up 80% of their consumer sales in FY 2012. Their overall product portfolio is made up of 60% "premium" brands and 40% "value" brands which should allow them to weather any slide in the economy well as consumers switch to the value branded products and still maintain solid sales as they switch back to premium products when the economy improves.

As part of their 10 key initiatives to drive investor return, they are expanding internationally. From 2000-2012, CHD grow from a US-centric company to now acquiring 18% of their revenues in foreign countries. International revenue growth has been a bit lower than I expected, but 5%+ from 2007 to 2012 is still at a comfortable level. Acquisitions is another part of their growth plan and given their low debt levels and high FCF conversion I'd expect to see another acquisition to be in the works over the next year. In 2012 CHD purchased Avid Health, Inc. which was a leader in the adult and children gummy vitamin business.

One concern with CHD, as well as most other consumer staples companies, is that their largest customers tend to make up a large amount of revenues. From 2010 through 2012, Walmart accounted for 23%, 23%, and 24% of their sales. While this is a bit of a concern since one customer deciding it didn't want to carry the CHD lineup could potentially disrupt 20%+ of their revenues.

The advantage that a Church & Dwight has over it's larger counterparts is that there's plenty of room for growth and for acquisitions to make much more meaningful impacts on the bottom line. A billion dollar brand coming to CHD would increase revenues by 34% at CHD; however, PG acquiring a billion dollar brand only increases revenues 1.2%. I really like the consume staples sector for consistent dividend increases year in and year out as the demand for their products rarely dips by significant levels. Mid-cap companies can offer the best of both worlds between growth companies and established moats as their presence and brands are already in place but there's still significant room to expand and for acquisitions to be accretive to earnings. I'm going to really be watching to see how CHD continues to do on international expansion as that will be a big driver of growth along with potential acquisitions.

Church & Dwight is due for a dividend increase with their next payment in early March and I'd like to pick up shares of Church & Dwight, but just not at these levels. Based on their results thus far this year, I'd expect to see the quarterly dividend increased from $0.28 to either $0.31 (10.7%) or $0.32 (14.3%). This would give a yield at current prices around 1.93%. I'll be looking to initiate a position if shares dip to the $58-60 level.

To check out more reports check out my Stock Analysis page.

Remember if you haven't yet done so, sign up for the free Simply Investing Course giveaway. The entry period ends on Saturday, December 21st.

What do you think about Church & Dwight as a DG investment? How do you think the long-term dividend growth prospects are?

Another crazy overvalued consumer staples company, PIP. Like Clorox, PG, and the others. They will all come down as growth disappoints and the bond money returns to bonds....which I'm hoping will happen when interest rates go up. We'll see. I'm picking up some General Mills in the next couple days, now that they missed their quarter Cheers

ReplyDelete-Bryan

Bryan,

DeleteYeah, unfortunately a lot of the consumer staples are overvalued. At least CHD is kind of justified as they are expected to have a lot more growth than the behemoths. I'm torn on whether I want rates to rise much from here only because I'd really like to take advantage of the low rates to pick up at least one rental property in 2014. Hopefully 1Q. I think it would add some higher monthly cash flow and some good diversification of income sources. But I'm still looking forward to the shift back to bonds to lighten the demand for consumer staples stocks some. Hopefully we can get some good opportunities to add to some great, consistent dividend payers.

Thanks for the analysis on CHD. I've recently been considering initiating a position in them....love the brand portfolio they have and the stability they provide as a cons staples company. I suspected they were overvalued and needed to wait a little longer before pulling the trigger. Your analysis helps to reinforce this.

ReplyDeleteIntegrator,

DeleteNo problem. Love the company and their brands, but not the current share price. Their power brands are all number one in their respective markets which is a pretty amazing feat. At CHD is expected to grow at a decent clip which kind of justifies the high PE compared to some of the slower growing beasts like PG, CLX, CL. But I don't think the growth is enough to justify the current price. Would love to pick up a mid-cap consumer staples company because they can add that combination of growth plus they already have a solid moat in place which can lead to huge future DG. We'll just have to wait for better prices though.

Thanks for stopping by!

Nice analysis. Back in 2005, I didn't do nearly a comprehensive analysis as you have done. While I definitely looked at the financials, what appealed to me was the product mix. I can remember the Arm & Hammer brand all the way back to when I was little and I figured the brand would probably outlive me. I also liked the fact one of their brands is Trojan condoms (a product you can't resuse...at least I hope you don't). When I delved further into their product mix I noticed a similarity. CHD makes/sells stuff you constantly have to replenish. As with the condoms, you don't want to reuse liquid detergent, toothpaste, kitty litter, etc..

ReplyDeleteBased on my "super" in depth analysis, we picked up a few thousand shares. Since then, my wife and I have watched the stock split and the dividend grow exponentially.

Sure, the stock might look a bit rich at the moment but how many shares are you looking to purchase? Seriously, so you pay $66.48 (today's closing price) vs $60 and you buy 1000 shares. What's $6,480 in the great scheme of things? Thirty years from now, will you really care?

You don't disclose your age in your profile but from reading your background, you sound as if you have one of the key components required to grow your wealth....time.

Just my $0.02 worth.

Cheers.

Chuck from Ontario

Chuck,

DeleteI hope no one's reusing condoms. Just thought of that makes me a little sick. The product mix is great and they're slowly growing their brands. The consumer staples sure are great for investors, I love give the razor away sell the blades model. Nothing like consistent repeat customers. Even if you didn't do a in depth look at the financials, you did the most important part which is finding a successful business model. Like WB says, "It's better to buy a great company at a fair price, than a fair company at a great price".

As far as the valuation I'm kind of torn on it. Sure, the difference in the long run won't really be that noticeable, but the starting price determines your future returns. If I had an amount set aside specifically to purchase CHD, then yeah I'd probably plop some down, but since I'm still in acquisition mode, then I don't see why I shouldn't purchase companies that I feel have similar growth prospects but a better valuation.

Thought I had my age somewhere, but I guess I don't. I'm 29 now and turning 30 in early January so I've still got time on my side, although time is also kind of pressed since I'm trying my best to reach FI no later than 40, hopefully much sooner.

Thanks for stopping by Chuck and for your thoughts. It's always great to get feedback from readers to help us all learn.

Thanks for your in depth look at CHD. Having been a follower of ARM & HAMMER as well as the general mix, I pulled the trigger this summer buying at $59. It is a tad overvalued, but the low beta consumer stable line is quite the investment for recessions

ReplyDeletewhich come along at regular intervals. For a retiree, one can sleep well being fairly certain future 10% annual div. increases will deal effectively with inflation. Self taught student of Warren Buffett. Ray

Ray,

DeleteI probably should have bought some earlier this year, but I'm sure something else happened to catch my eye at the time. Those low beta consumer staples companies are great for consistent dividend increases as most of them have their brands established enough to be able to pass on at least inflation costs so you can expect at a minimum to get those kind of raises. Glad to meet another self taught investor and I hope your retirement goes well. I'm hoping to reach early FI and possibly ER in the next few years.

Thanks for stopping by!