Cisco Dividend Stock Analysis

I wanted to take a more in depth look at a company I've sold some puts on, Cisco (CSCO). Cisco is by no means a dividend champion, challenger, or even contender with only 2 years of increases, but the potential is there for rapid growth so I figured we should look a bit more into the company. Cisco closed trading on Friday, May 17th at $24.04.

Company Background (sourced from Yahoo! Finance):

Cisco Systems, Inc. designs, manufactures, and sells Internet protocol (IP) based networking and other products related to the communications and information technology industries worldwide. It offers switching products, including fixed-configuration and modular switches, and storage products that provide connectivity to end users, workstations, IP phones, access points, and servers, as well as function as aggregators on local-area networks and wide-area networks; and routers that interconnects public and private IP networks for mobile, data, voice, and video applications. The company also provides set-top boxes; cable modem CPE products, such as data, EMTA, and gateways; cable modem termination systems products; videoscape software products; and headend equipment, which include encoders, decoders, and transcoders. In addition, it offers collaboration products comprising IP phones, call center and messaging products, unified communications infrastructure products, and Web-based collaborative offerings, as well as telepresence systems that integrates voice, video, data, and mobile applications on fixed and mobile networks; and security products consisting of firewall, intrusion prevention, remote access, virtual private networks, unified clients, network admission control, Web gateways, and email gateways, which deliver identity, network, and content security solutions for mobile, collaborative, and cloud-enabled businesses. Further, the company provides wireless products, such as wireless access points, controllers, antennas, and integrated management solutions; data center products, which include blade and rack servers, fabric interconnects, and server access virtualization; and home networking and other networking products. Additionally, it offers technical support services; and responsive, preventive, and consultative support services for its technologies.

DCF Valuation:

Analysts expect Cisco to grow earnings 8.33% per year for the next five years and I've assumed they can continue to grow at 3.50% per year thereafter. Running these numbers through a two stage DCF analysis with a 12% discount rate yields a fair value price of $28.19. This means the shares are trading at a 14.0% discount to the DCF.

Graham Number:

With a current book value per share of $10.66 and TTM EPS of $1.80, the Graham Number is calculated to be $20.78. Currently Cisco is trading for a 16.7% premium to the Graham Number.

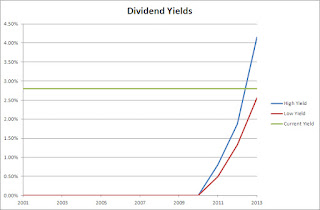

Average High Dividend Yield:

Cisco's average high dividend yield for the past 2 years is 3.01% and for the past 3 years is 2.27%. This gives target prices of $22.60 and $29.90 respectively based on the current annual dividend of $0.68. I think the 3.00% range is probably going to be closer to the average high yield going forward so I'll use the 2 year average. Cisco is currently trading at a 7.3% premium to my assumed average high dividend yield valuation.

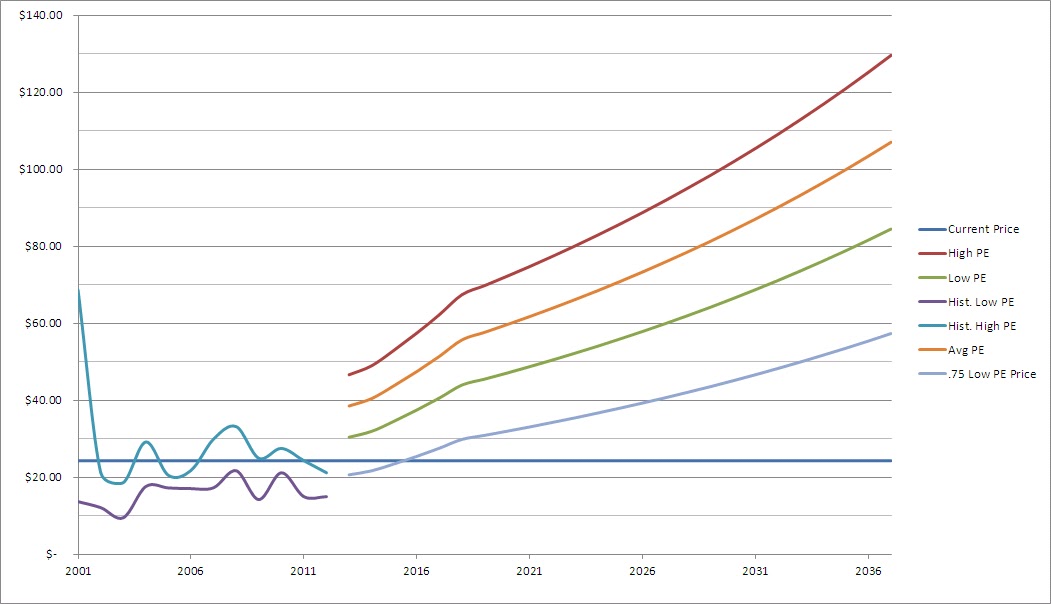

Average Low PE Ratio:

Cisco's average low PE ratio for the past 5 years is 13.74 and for the past 10 years is 16.64. This corresponds to a price per share of $27.49 and $33.28 respectively based off the analyst estimate of $2.00 per share for fiscal year 2013. As Cisco has become a more mature company their P/E ratios have been contracting. Going forward I expect the 5 year range of 13.74 to 20.92 to be more typical although I still think it will come down from here. For this reason I'll calculate a target entry price based off a low P/E ratio of 10 going forward which gives a target entry price of $20.00. Cisco is currently trading at a 21.2% premium to this price.

Average Low P/S Ratio:

Cisco's average low PS ratio for the past 5 years is 2.41 and for the past 10 years is 3.20. This corresponds to a price per share of $22.13 and $29.31 respectively based off the analyst estimate for revenue growth from FY 2012 to FY 2013. Currently, their current PS ratio is 2.70 on a trailing twelve months basis. I'll use the 5 year average in my calculations just to be conservative. Cisco is currently trading at a 9.5% premium to this price.

Dividend Discount Model:

For the DDM, I assumed that Cisco will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, 5 or 10 year growth rates. In this case that would be 15%. Cisco doesn't have a long history of growing their dividend since they first initiated it in April 2011 but the growth has been fantastic since. With more of the "old tech" companies building their history of increasing the dividend I think Cisco will continue to do so. After that I assumed they can continue to raise dividends for 3 years at 75% of 15% or 11.25% and in perpetuity at 3.50%. The dividend growth rates are based off fiscal year payouts and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on the DDM, Cisco is worth $19.40, meaning it's overvalued by 24.9%.

PE Ratios:

Cisco's trailing PE is 13.47 and it's forward PE is 111.54. The PE3 based on the average earnings for the last 3 years is 18.23. I like to see the PE3 be less than 15 which Cisco is currently over. Compared to it's industry, Cisco seems to be undervalued versus JNPR (35.08) as well as the industry overall (20.41). All industry comparisons are on a TTM basis. Cisco's PEG for the next 5 years is currently at 1.43 while ALU is at 0.23 and JNPR is at 1.04. Based on the PEG ratio, Cisco is overvalued versus it's competitors, meaning you're paying more for the growth of PG.

Fundamentals:

Cisco's gross margins for FY 2011 and FY 2012 were 65.9% and 66.1% respectively. They have averaged a 69.2% gross profit margin since 2003 with a low of 65.9% in FY 2011. Their net income margin for the same years were 15.0% and 17.5%. Since 2003 their net income margin has averaged 19.5% with a low of 15.0% in FY 2011. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. Cisco is doing well on both margin fronts. Since each industry is different and allows for different margins, we'll see where they stand against the industry. For FY 2012, Cisco captured 103.5% of the gross margin for the industry and 120.1% of the net income margin. Being an industry leader has its advantages in pricing power and allows them to maintain higher than industry average margins.

Share Buyback:

Cisco's shares outstanding have been decreasing the last 10 years. Since FY 2002, they've purchased 27.4% of their shares outstanding for an average annualized decrease of 3.2%. Looking at the amount spent on share buybacks, it slowed in 2012 and over the TTM. So management could be feeling that the share price is closer to fairly valued at more recent price. By repurchasing shares, Cisco is able to increase EPS and management can return cash to shareholders this way by increasing the ownership stake of the company for all the outstanding shares.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Cisco is far from being a dividend champion or even a challenger with only 3 years of increasing dividends under their belt, assuming the dividend is maintained the rest of this year. Their current annual dividend sits at $0.68 for a yield of 2.81%. Cisco's quarterly increases have been 33.3%, 75.0%, and 21.4%. The last 2 increases have been after just 2 quarters so the annualized rates are even higher. Since initiating the dividend, the payout ratio has averaged 14.5%. Based on the analyst estimate of $2.00 in EPS for FY 2013 and the forecast dividends of $0.62, the payout ratio for FY 2013 should come in around 31%. The payout ratio is still plenty low to allow for mid double digit growth rates of the dividend. If EPS increases at the analyst estimate of 8.33% they can increase dividends at 11.50% and maintain a constant payout ratio assuming the share buyback program continues to retire ~3.2% of the shares outstanding each year. Having a low payout ratio leaves more room for management to increase the dividend without overly burdening the underlying business.

Cisco's free cash flow has been great since FY 2002 growing at a 10.1% annualized rate. Their free cash flow payout ratio has averaged only 10.9% since FY 2011, which is even lower than the payout based on earnings. Annual total shareholder return when accounting for buybacks plus dividends has averaged 72.6% of FCF since FY 2011 and is at 51.6% over the last twelve months.

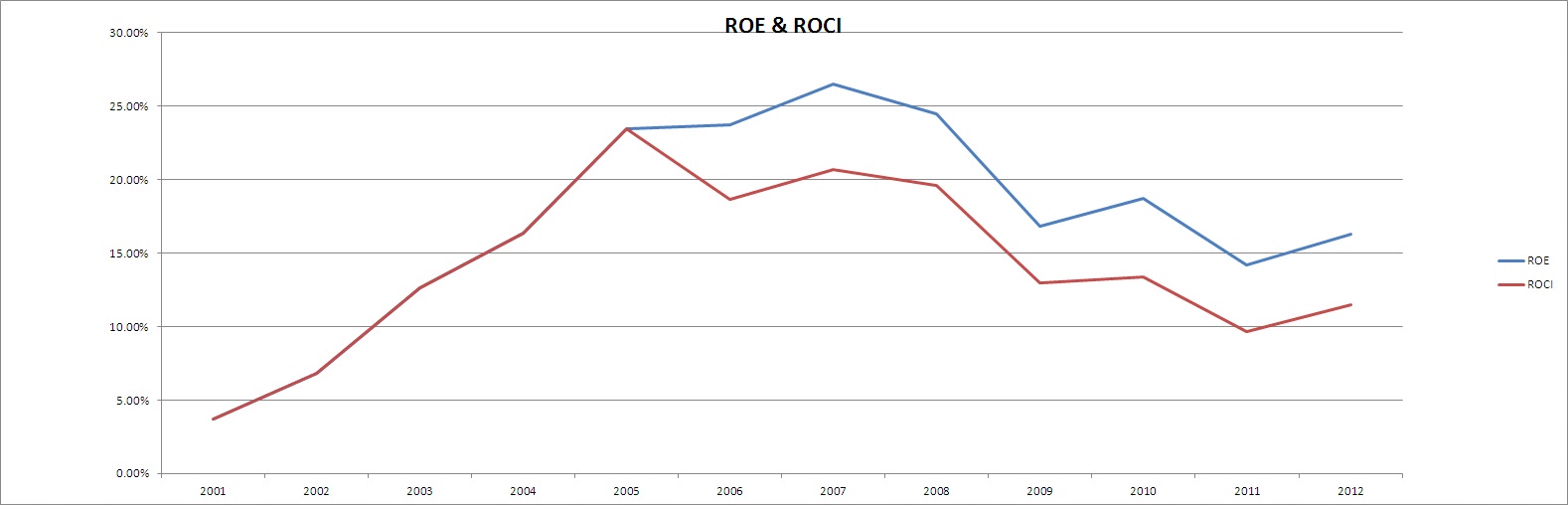

Return on Equity and Return on Capital Invested:

Cisco's ROE has averaged 19.3% since 2003 and has been very strong since then although a bit more volatile than I'd like ranging from 12.6% to 26.5%. Their ROCI has averaged a 15.9% since 2003 and like their ROE has been very strong but more volatile than I'd like to see. I don't necessarily look for any absolute values, rather I like to see stable to increasing levels over the long term. Cisco's ROE and ROCI are both not exactly stable, but even in the down years it's still being maintained a solid levels.

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how Cisco has done on that front. Their revenue growth since 2002 has been solid with a 9.31% annual increase and their net income has been growing at a 15.56% rate. Since their net income has been growing faster than revenue, their net income margin has increased from 10.0% to 17.5% between FY 2002 and FY 2012. Over that time, Cisco has had 2 years of decline in revenue , FY 2003 and FY 2009. The first decline was marginal with in the grand scheme of things but the FY 2009 decrease was pretty significant. Considering all of the issues that were going on with the economy between FY's 2009 and 2009 the decline wasn't that bad. They've already surpassed the previous high for revenue and continued their growing ways.

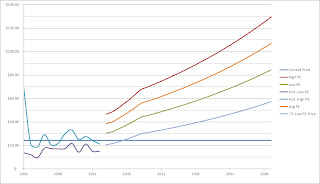

Forecast:

The chart shows the historical high and low prices since 2001 and the forecast based on the average PE ratios and the expected EPS values. I have also included a forecast based off a PE ratio that is only 75% of the average low PE ratio. I like to the look to buy at the 75% Low PE price or lower to provide for additional margin of safety, although this price doesn't usually come around very often. In this case the target low PE is 15.2 and the 0.75 * PE is 10.3. This corresponds to an entry price of $30.38 based off the expected earnings for FY 2013 of $2.00, with a 75% target price of $20.61. The average PE price would give a target price of $38.49. Currently Cisco is trading at a $3.63 premium to the 75% low PE target price and a $14.25 discount to the average PE price. If you believe the analyst estimates are pretty close, then Cisco is trading on the lower end of it's typical range.

Conclusion:

The average of all the valuation models gives a target entry price of $22.18 which means that Cisco is currently trading at a 9.3% premium to the target entry price. I've also calculated it with the highest and lowest valuation methods thrown out. In this case, the DCF and DDM valuations are removed and the new average is $21.38. Cisco is trading at a 13.4% premium to this price as well.

Assuming that Cisco can grow their earnings and dividends at the rates that I assumed, you're looking at solid returns over the next 10 years. In 2023, EPS would be $3.32 and slapping an average PE of 16 gives a price of $53.10. Over the next 10 years you'd also receive $14.34 in dividends for a total return of 278.20% which is good for a 10.77% annualized rate. If you purchase at my target entry price of $22.18, your projected 10 year total return jumps to 304.04% for an annualized return of 11.76%.

Overall, I would say that Cisco is currently fairly valued after jumping over 14% after their latest quarterly earnings release. Most of their competitors had bad quarters while Cisco continued to shine in the last quarter. Cisco is the market leader although the moat isn't as wide with it being a technology company. It's too easy for some groundbreaking technology to come along and quickly make their products obsolete. As I mentioned in my first put option post on Cisco, according to Internet World Stats only 34% of the global population has access to the internet. We're still probably decades away from having everyone connected, but there's plenty of room for growth in Cisco's product line. As smartphones and tablets continue to be more involved in our everyday lives, Cisco is in an enviable position being a market leader and providing the backend technology to satisfy everyone's data consumption needs. I only see computer networking increasing in the future and Cisco's line up of routers, switches and various other products to grow as well. From a dividend growth stand point Cisco has plenty of room to increase the dividend at a double digit rate for years to come. The issue is whether management will truly commit to annually increasing the dividend like clockwork. They have a very short history just recently hitting the 2 year mark in April 2013.

I'd be interested in purchasing Cisco, but like most other companies I want to own, just not at today's prices. So I'm left with 2 options, either just sit tight and wait for the price to retreat or I can sell put options. I don't see any combinations of strike price and option premium to allow for solid returns if it expires or a great entry price if it's executed so for now I'll just sit on my cash and look for other opportunities.

To check out more reports check out my Stock Analysis page.

What do you think about Cisco as a DG investment at today's prices? Do you think they'll continue with increasing the dividend or was this just a play to boost the share price with many investors flocking towards dividends?

Company Background (sourced from Yahoo! Finance):

Cisco Systems, Inc. designs, manufactures, and sells Internet protocol (IP) based networking and other products related to the communications and information technology industries worldwide. It offers switching products, including fixed-configuration and modular switches, and storage products that provide connectivity to end users, workstations, IP phones, access points, and servers, as well as function as aggregators on local-area networks and wide-area networks; and routers that interconnects public and private IP networks for mobile, data, voice, and video applications. The company also provides set-top boxes; cable modem CPE products, such as data, EMTA, and gateways; cable modem termination systems products; videoscape software products; and headend equipment, which include encoders, decoders, and transcoders. In addition, it offers collaboration products comprising IP phones, call center and messaging products, unified communications infrastructure products, and Web-based collaborative offerings, as well as telepresence systems that integrates voice, video, data, and mobile applications on fixed and mobile networks; and security products consisting of firewall, intrusion prevention, remote access, virtual private networks, unified clients, network admission control, Web gateways, and email gateways, which deliver identity, network, and content security solutions for mobile, collaborative, and cloud-enabled businesses. Further, the company provides wireless products, such as wireless access points, controllers, antennas, and integrated management solutions; data center products, which include blade and rack servers, fabric interconnects, and server access virtualization; and home networking and other networking products. Additionally, it offers technical support services; and responsive, preventive, and consultative support services for its technologies.

DCF Valuation:

Analysts expect Cisco to grow earnings 8.33% per year for the next five years and I've assumed they can continue to grow at 3.50% per year thereafter. Running these numbers through a two stage DCF analysis with a 12% discount rate yields a fair value price of $28.19. This means the shares are trading at a 14.0% discount to the DCF.

Graham Number:

With a current book value per share of $10.66 and TTM EPS of $1.80, the Graham Number is calculated to be $20.78. Currently Cisco is trading for a 16.7% premium to the Graham Number.

Average High Dividend Yield:

Cisco's average high dividend yield for the past 2 years is 3.01% and for the past 3 years is 2.27%. This gives target prices of $22.60 and $29.90 respectively based on the current annual dividend of $0.68. I think the 3.00% range is probably going to be closer to the average high yield going forward so I'll use the 2 year average. Cisco is currently trading at a 7.3% premium to my assumed average high dividend yield valuation.

Cisco's average low PE ratio for the past 5 years is 13.74 and for the past 10 years is 16.64. This corresponds to a price per share of $27.49 and $33.28 respectively based off the analyst estimate of $2.00 per share for fiscal year 2013. As Cisco has become a more mature company their P/E ratios have been contracting. Going forward I expect the 5 year range of 13.74 to 20.92 to be more typical although I still think it will come down from here. For this reason I'll calculate a target entry price based off a low P/E ratio of 10 going forward which gives a target entry price of $20.00. Cisco is currently trading at a 21.2% premium to this price.

Average Low P/S Ratio:

Cisco's average low PS ratio for the past 5 years is 2.41 and for the past 10 years is 3.20. This corresponds to a price per share of $22.13 and $29.31 respectively based off the analyst estimate for revenue growth from FY 2012 to FY 2013. Currently, their current PS ratio is 2.70 on a trailing twelve months basis. I'll use the 5 year average in my calculations just to be conservative. Cisco is currently trading at a 9.5% premium to this price.

Dividend Discount Model:

For the DDM, I assumed that Cisco will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, 5 or 10 year growth rates. In this case that would be 15%. Cisco doesn't have a long history of growing their dividend since they first initiated it in April 2011 but the growth has been fantastic since. With more of the "old tech" companies building their history of increasing the dividend I think Cisco will continue to do so. After that I assumed they can continue to raise dividends for 3 years at 75% of 15% or 11.25% and in perpetuity at 3.50%. The dividend growth rates are based off fiscal year payouts and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on the DDM, Cisco is worth $19.40, meaning it's overvalued by 24.9%.

PE Ratios:

Cisco's trailing PE is 13.47 and it's forward PE is 111.54. The PE3 based on the average earnings for the last 3 years is 18.23. I like to see the PE3 be less than 15 which Cisco is currently over. Compared to it's industry, Cisco seems to be undervalued versus JNPR (35.08) as well as the industry overall (20.41). All industry comparisons are on a TTM basis. Cisco's PEG for the next 5 years is currently at 1.43 while ALU is at 0.23 and JNPR is at 1.04. Based on the PEG ratio, Cisco is overvalued versus it's competitors, meaning you're paying more for the growth of PG.

Fundamentals:

Cisco's gross margins for FY 2011 and FY 2012 were 65.9% and 66.1% respectively. They have averaged a 69.2% gross profit margin since 2003 with a low of 65.9% in FY 2011. Their net income margin for the same years were 15.0% and 17.5%. Since 2003 their net income margin has averaged 19.5% with a low of 15.0% in FY 2011. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. Cisco is doing well on both margin fronts. Since each industry is different and allows for different margins, we'll see where they stand against the industry. For FY 2012, Cisco captured 103.5% of the gross margin for the industry and 120.1% of the net income margin. Being an industry leader has its advantages in pricing power and allows them to maintain higher than industry average margins.

Share Buyback:

Cisco's shares outstanding have been decreasing the last 10 years. Since FY 2002, they've purchased 27.4% of their shares outstanding for an average annualized decrease of 3.2%. Looking at the amount spent on share buybacks, it slowed in 2012 and over the TTM. So management could be feeling that the share price is closer to fairly valued at more recent price. By repurchasing shares, Cisco is able to increase EPS and management can return cash to shareholders this way by increasing the ownership stake of the company for all the outstanding shares.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Cisco is far from being a dividend champion or even a challenger with only 3 years of increasing dividends under their belt, assuming the dividend is maintained the rest of this year. Their current annual dividend sits at $0.68 for a yield of 2.81%. Cisco's quarterly increases have been 33.3%, 75.0%, and 21.4%. The last 2 increases have been after just 2 quarters so the annualized rates are even higher. Since initiating the dividend, the payout ratio has averaged 14.5%. Based on the analyst estimate of $2.00 in EPS for FY 2013 and the forecast dividends of $0.62, the payout ratio for FY 2013 should come in around 31%. The payout ratio is still plenty low to allow for mid double digit growth rates of the dividend. If EPS increases at the analyst estimate of 8.33% they can increase dividends at 11.50% and maintain a constant payout ratio assuming the share buyback program continues to retire ~3.2% of the shares outstanding each year. Having a low payout ratio leaves more room for management to increase the dividend without overly burdening the underlying business.

Cisco's free cash flow has been great since FY 2002 growing at a 10.1% annualized rate. Their free cash flow payout ratio has averaged only 10.9% since FY 2011, which is even lower than the payout based on earnings. Annual total shareholder return when accounting for buybacks plus dividends has averaged 72.6% of FCF since FY 2011 and is at 51.6% over the last twelve months.

Return on Equity and Return on Capital Invested:

Cisco's ROE has averaged 19.3% since 2003 and has been very strong since then although a bit more volatile than I'd like ranging from 12.6% to 26.5%. Their ROCI has averaged a 15.9% since 2003 and like their ROE has been very strong but more volatile than I'd like to see. I don't necessarily look for any absolute values, rather I like to see stable to increasing levels over the long term. Cisco's ROE and ROCI are both not exactly stable, but even in the down years it's still being maintained a solid levels.

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how Cisco has done on that front. Their revenue growth since 2002 has been solid with a 9.31% annual increase and their net income has been growing at a 15.56% rate. Since their net income has been growing faster than revenue, their net income margin has increased from 10.0% to 17.5% between FY 2002 and FY 2012. Over that time, Cisco has had 2 years of decline in revenue , FY 2003 and FY 2009. The first decline was marginal with in the grand scheme of things but the FY 2009 decrease was pretty significant. Considering all of the issues that were going on with the economy between FY's 2009 and 2009 the decline wasn't that bad. They've already surpassed the previous high for revenue and continued their growing ways.

Forecast:

Conclusion:

The average of all the valuation models gives a target entry price of $22.18 which means that Cisco is currently trading at a 9.3% premium to the target entry price. I've also calculated it with the highest and lowest valuation methods thrown out. In this case, the DCF and DDM valuations are removed and the new average is $21.38. Cisco is trading at a 13.4% premium to this price as well.

Assuming that Cisco can grow their earnings and dividends at the rates that I assumed, you're looking at solid returns over the next 10 years. In 2023, EPS would be $3.32 and slapping an average PE of 16 gives a price of $53.10. Over the next 10 years you'd also receive $14.34 in dividends for a total return of 278.20% which is good for a 10.77% annualized rate. If you purchase at my target entry price of $22.18, your projected 10 year total return jumps to 304.04% for an annualized return of 11.76%.

Overall, I would say that Cisco is currently fairly valued after jumping over 14% after their latest quarterly earnings release. Most of their competitors had bad quarters while Cisco continued to shine in the last quarter. Cisco is the market leader although the moat isn't as wide with it being a technology company. It's too easy for some groundbreaking technology to come along and quickly make their products obsolete. As I mentioned in my first put option post on Cisco, according to Internet World Stats only 34% of the global population has access to the internet. We're still probably decades away from having everyone connected, but there's plenty of room for growth in Cisco's product line. As smartphones and tablets continue to be more involved in our everyday lives, Cisco is in an enviable position being a market leader and providing the backend technology to satisfy everyone's data consumption needs. I only see computer networking increasing in the future and Cisco's line up of routers, switches and various other products to grow as well. From a dividend growth stand point Cisco has plenty of room to increase the dividend at a double digit rate for years to come. The issue is whether management will truly commit to annually increasing the dividend like clockwork. They have a very short history just recently hitting the 2 year mark in April 2013.

I'd be interested in purchasing Cisco, but like most other companies I want to own, just not at today's prices. So I'm left with 2 options, either just sit tight and wait for the price to retreat or I can sell put options. I don't see any combinations of strike price and option premium to allow for solid returns if it expires or a great entry price if it's executed so for now I'll just sit on my cash and look for other opportunities.

To check out more reports check out my Stock Analysis page.

What do you think about Cisco as a DG investment at today's prices? Do you think they'll continue with increasing the dividend or was this just a play to boost the share price with many investors flocking towards dividends?

I think Cisco will continue to aggressively grow the dividend thanks to the massive pile of cash they are holding. I normally only hold the CCC's, but I made an exception for Cisco.

ReplyDeleteI've got an options question for you. I'm with ScottTrade, but they won't let you sell Naked Puts to open. Which brokerage do you use for Options trading?

I'm with you on Cisco. I think they'll continue growing the dividend but it is a risk to consider since there's not exactly a long history there. Since initiating it though they've grown it 14.4% per quarter. Thats some outrageous growth and the potential for more to come is there.

DeleteI would think scottrade would allow you to sell naked puts but you should have to fill out a margin agreement and have the appropriate option level approval. I use Fidelity although there's better options out there that offer lower commission. I'm not exactly sure how they stack up on order execution though.

Thanks for stopping by!

I double checked my Scott Trade accout. I've got level 2 trading privliges which is their highest level. I've used my margin account at ST a few times in the past when their were actually bargains to be had in the market. I'll check it out with them. I love the idea of getting paid while I wait for a stock to drop to my price target.

DeleteI'm optimistic on Cisco, but you are right they haven't got a long enough track record to be considered a reliable dividend payer yet. Love the site by the way.

Hrmmm..let me know what you find out about Scottrade because I've been thinking of switching to them if they ever start their dividend reinvestment program up. The concept is pretty awesome since they let you accumulate the dividends from all companies and then choose which one to invest in, commission free. Great idea there.

DeleteThe potential is there and as investors we must look forward to see where they're going not where they've been. I think it's okay to allocate a small portion of one's portfolio to Cisco but I wouldn't go too heavy since the history isn't there and the tech industry is known to have sweeping changes every now and then that completely change the landscape.

Thanks for the compliment.

Hey PIP. Sorry I'm so slow a getting back to you. I finally sold some puts yesterday (KO and TGT). I had to open an Options Express account. Scott Trade doesn't allow selling to open (neither does Sharebuilder). ST says they will be offering this option by the summer. Anyway, thought I'd share. Site is still great. Careful on those rentals, that was my original plan. I like the dividend payers better they always pay on time and never call at midnight. Best of luck, Mike.

DeleteAs you know, I am a big fan of Cisco and think they have the opportunity to have tremendous growth, both in share value and in their dividend payments. Like several of the other technology "titans" they are sitting on an unbelievably large cash pile and will have the ability to continue to significantly raise their dividends. I was fortunate in that I was able to get assigned 100 shares at a cost of $20.65 per share. Another dividend increase or two will really load up the yield on cost for those shares.

ReplyDeleteAdditionally, as you've mentioned, the internet still has an impressive amount of pentration left in the tank and Cisco is well positioned to be a large part of the backbone of that growth. I think the next ten years will be very rewarding to Cisco shareholders.

W2R,

DeleteThe amount of cash sitting idle by some of these companies is astounding. I actually completely forgot to add in to my analysis their cash and short term investments per share. This comes to around $8.70 per share so the growth of the company is being discounted heavily. That's about 1/3 of the current market cap is essentially cash.

Thanks for stopping by!

Pursuit,

ReplyDeleteThanks for the analysis.

I concur completely. I think the future is fairly bright for Cisco because the future of the internet is so bright, and CSCO provides some basic infrastructure products that will ride the wave of that growth.

I was actually interested in initiating a position in the company, and mentioned that on my blog recently. Then it popped and I'm stuck again. Very frustrating to do some leg work and be ready to make a move and then see the price jump so dramatically. I agree that the stock is fairly priced here. I was interested before the pop because I thought there was a 10-15% margin of safety. Now that is gone.

I'll keep huntin...

Best wishes!

DM,

DeleteNo problem. I expected a pop after earnings were announced but didn't think it'd be 14+%. Luckily it's pulled back some so maybe we can get another chance to purchase around the $21 level. Since it is a tech company I'm trying to avoid going to heavily into them, especially since they don't exactly have a long history of growing the dividend but the potential is there and we have to look forward to be successful with investing.

Hopefully today's late day selloff will be the start of something great for all of us DG/value investors.

Thanks for stopping by!

I like your analysis, very detailed and throughout. I think Cisco may be able to continue its current dividend policy so it may be considered as a good addition to a portfolio. However, recently I am fully invested and do not plan on adding it. But that said, I didn't have this stock in my watch list, so I will be adding it.

ReplyDeleteOK, I just checked the stock and my source says the stock paying dividends since 2011 and only 1 year of dividend increase... :(

ReplyDeleteMartin,

DeleteGlad to bring a new stock to your attention. That's what I love about the DG/FI community, there's always someone bringing something new to the table each and every day. While Cisco doesn't have a long history the potential is there so I think it's worth taking a bit of a flyer on it. Plus there's still room for just price appreciation due to the growth of the company. I think they might have actually hit 2 years based on a fiscal year streak but assuming the next payment is maintained they'll have 2 full years of increases. Even though the history is short they've been growing it ridiculously fast. 14.40%. PER QUARTER. Not per year. That's crazy. I don't expect that going forward but double digit increases should still be on the way for the next few years.

Thanks for stopping by!

Thanks for going into detail with CSCO. I think the thesis here is strong, but as you say there is no way to know if a competitor will swoop in with better technology or not. CSCO is somewhat entrenched with all the cert programs and training they offer, it would be difficult to start a new company and accomplish what Cisco has built overnight. CSCO looks like a budding dividend story, pretty interesting. I don't like the sector at all, but this may be worth a gamble. Worthy of consideration.

ReplyDeleteCI,

DeleteI completely forgot about the cert programs and training. That's a great point for their stickiness. While it is a tech company and tech is subject to quick changes, you're right about Cisco probably not being as exposed to it and they won't disappear overnight. I think the opportunity is there for great dividend growth and total returns going forward. I liken them to a industrial company that will ebb and flow with the market cycle but overall growing the business through each cycle. Should be interesting to see how it plays out.

Thanks for stopping by!

Great review, I am seriously thinking about buying CSCO. I have a feeling this will one day be a dividend aristocrat. I think they will have continued dividend growth for a long time.

ReplyDeleteCaptain Dividend,

DeleteGlad to have you on board! I'm also wanting to pick up some Cisco but I want to buy closer to $22 or lower. I have 2 open put options that will give me purchase prices that I'd like so that's going to be my only exposure unless the markets head south and really give us an opportunity to get some value again. I also think they could be a dividend aristocrat in the future because there's still plenty of room for growth for the company.

Thanks for stopping by!

This is a site to view volume and stock technical analysis chart analysis. This site provides leading technical indicator analysis and provides a great stock screener.

DeleteThx for the great analysis. Cisco wouldn't have been on my radar for another 3 years since I only track stocks with a dividend history of at least 5 years. I might add it to my watch list sooner ;-)

ReplyDeleteNice post. In January 31, 2013 the company Cisco acquired Cariden Technologies Inc. In February 2013, it acquired Intucell and in May 2013 it acquired Ubiquisys. Its current dividend yield is 2.79%.

ReplyDeleteThis is a site to view volume and technical indicatorchart analysis. This site provides leading technical indicator analysis and provides a great stock screener.

ReplyDeleteFound this stock analysis this am as I am considering purchasing CSCO today after the dip of yesterday.

ReplyDeleteThanks for the great info.