Mattel Stock Analysis

After seeing a few articles about Mattel after selling off due to a weak 1st quarter, which is fairly typical seeing as how they sell toys and after the Christmas season spending is usually light, I decided to run Mattel (MAT) through my screening process to see where it currently stands. Mattel closed on Wednesday 5/2/12 at $33.88.

Company Background:

Mattel, Inc., together with its subsidiaries, designs, manufactures, and markets various toy products. Its products comprise fashion dolls and accessories, vehicles and play sets, and games and puzzles. The company offers its products under the Mattel Girls and Boys brands, including Barbie, Polly Pocket, Little Mommy, Disney Classics, Monster High, Hot Wheels, Matchbox, Tyco R/C, CARS, Radica, Toy Story, WWE Wrestling, and Batman; Fisher-Price brands comprising Fisher-Price, Little People, BabyGear, View-Master, Dora the Explorer, Go Diego Go!, Thomas and Friends, Mickey Mouse, Sing-a-ma-jigs, See ‘N Say, and Power Wheels; and American Girl Brands, such as My American Girl, Bitty Baby, McKenna, and the newest Girl of the Year. It also publishes advice and activity books, as well as magazines comprising American Girl. The company sells its American Girl products directly to consumers through catalogue, Web site, and retail stores in the United States and Canada. Mattel sells its other products directly to retailers, including discount and free-standing toy stores, chain stores, department stores, and other retail outlets; wholesalers; and distribution centers worldwide.

DCF Valuation:

Analysts expect Mattel to be able to grow earnings 9.05% per year for the next five years and I've assumed they can continue to grow at 3.00% per year thereafter. Running these numbers through a DCF analysis with a 10% discount rate yields a fair value price of $43.94. This means that at $33.88 the shares are undervalued by 22.89%.

Graham Number:

Over the last 12 months, MAT's EPS were $2.17 and it's current book value per share is $7.76. The Graham Number is calculated to be $19.46 which means that at $33.88 the shares are overvalued by 74.06%. If you calculate the Graham Number based off the expected EPS, $2.41, for the fiscal year 2012 ending in December and keep the book value per share constant you arrive at a fair value price of $20.51. Either way MAT is overvalued quite a bit according to the Graham Number calculation.

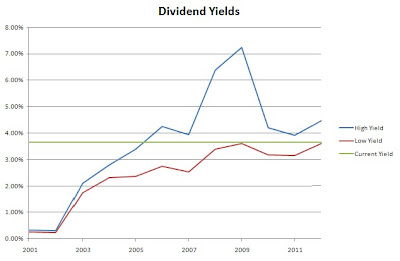

Average High Dividend Yield:

MAT's average high dividend yield for the past 10 years is 4.51% and for the past 5 years is 5.24%. We'll use the 5 year yield since Mattel has grown their dividends for the past 4 years. This gives a target price of $23.65 meaning Mattel is overvalued by 43.24%. The following chart shows the historical high and low dividend yield as well as the current yield.

Company Background:

Mattel, Inc., together with its subsidiaries, designs, manufactures, and markets various toy products. Its products comprise fashion dolls and accessories, vehicles and play sets, and games and puzzles. The company offers its products under the Mattel Girls and Boys brands, including Barbie, Polly Pocket, Little Mommy, Disney Classics, Monster High, Hot Wheels, Matchbox, Tyco R/C, CARS, Radica, Toy Story, WWE Wrestling, and Batman; Fisher-Price brands comprising Fisher-Price, Little People, BabyGear, View-Master, Dora the Explorer, Go Diego Go!, Thomas and Friends, Mickey Mouse, Sing-a-ma-jigs, See ‘N Say, and Power Wheels; and American Girl Brands, such as My American Girl, Bitty Baby, McKenna, and the newest Girl of the Year. It also publishes advice and activity books, as well as magazines comprising American Girl. The company sells its American Girl products directly to consumers through catalogue, Web site, and retail stores in the United States and Canada. Mattel sells its other products directly to retailers, including discount and free-standing toy stores, chain stores, department stores, and other retail outlets; wholesalers; and distribution centers worldwide.

DCF Valuation:

Analysts expect Mattel to be able to grow earnings 9.05% per year for the next five years and I've assumed they can continue to grow at 3.00% per year thereafter. Running these numbers through a DCF analysis with a 10% discount rate yields a fair value price of $43.94. This means that at $33.88 the shares are undervalued by 22.89%.

Graham Number:

Over the last 12 months, MAT's EPS were $2.17 and it's current book value per share is $7.76. The Graham Number is calculated to be $19.46 which means that at $33.88 the shares are overvalued by 74.06%. If you calculate the Graham Number based off the expected EPS, $2.41, for the fiscal year 2012 ending in December and keep the book value per share constant you arrive at a fair value price of $20.51. Either way MAT is overvalued quite a bit according to the Graham Number calculation.

Average High Dividend Yield:

MAT's average high dividend yield for the past 10 years is 4.51% and for the past 5 years is 5.24%. We'll use the 5 year yield since Mattel has grown their dividends for the past 4 years. This gives a target price of $23.65 meaning Mattel is overvalued by 43.24%. The following chart shows the historical high and low dividend yield as well as the current yield.

Average Low PE Ratio:

Mattel's average low PE ratio for the past 5 years is 10.41 and for the past 10 years is 11.87. This would correspond to a price per share of $25.08 and $28.60, respectively. The 5 year and 10 year low PE price targets are overvalued by 35.07% and 18.46%, respectively.

Dividend Discount Model:

For the DDM I assumed that MAT will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, 5 or 10 year growth rates. In this case that would be 10.58%. After that I assumed MAT can continue to raise dividends by 3.00% annually and used a discount rate of 7.5%. Based on this MAT is worth $34.67 meaning it's undervalued by 2.27%.

PE Ratios:

Matttel's trailing PE is 15.61 and it's forward PE is 12.89. The CAPE for the previous 10 years is 23.73. Compared to it's industry, MAT seems to be overvalued versus HAS (13.55) and fairly valued versus the industry as a whole (15.48). All industry and competitor comparisons are on a TTM EPS basis.

Fundamentals:

MAT's gross margin for FY 2010 and FY 2011 were 50.46% and 50.20% respectively. Their gross margin is very high at 50% and consitent too. I like to see both of those when looking at potential dividend growth stocks since it means they have pricing power. Their net income margin for the same years were 11.69% and 12.26% respectively. I like the net income margin to be at least 10% and preferably rising. MAT passes both of my criteria for net income margin. The cash-to-debt ratio for the same years were 1.35 and 0.91. I much would much rather see Mattel get their cash-to-debt ratio back to at least even but at 0.91 it's still manageable.

Share Buyback:

MAT's shares outstanding have been falling thanks to their share buyback program.

Dividend Analysis:

The biggest drawback that I see in Mattel is that it's dividend growth history is spotty. They've only increased their dividend for 4 consectutive years including this year's raise. Despite the fact that the dividend growht is a little suspect their 10 year growth rate is still high at 37.86%. Its growth rates for the past 1 year, 3 year, 5 year and 10 year are 34.78%, 18.25%, 10.58% and 37.86% respectively. While MAT isn't the most consistent divdend growth stock, 2007 - 2009 all had a $0.75 annual dividend, it makes up for it with bigger increases when available. They increased their dividend 700% from $0.05 to $0.40 per share in 2003 and most recently increased it from $0.92 to $1.24.

Their payout ratio is still in what I would consider a safe zone around the 50% mark. Since 2003 the payout ratio has average 46.31%. The FCF payout ratio is a little troubling. Sicne 2001 they've only had 6 years with a FCF payout ratio positive and less than 100%. The highest it's been in that time was in 2007 with a 750% ratio.

Return on Equity and Return on Capital: Invested

MAT's ROE and ROCI have been relatively consistent and generally trending upwards since 2001. I like to see a stable or increasing value for both.

Average Price and EPS:

MAT's average share price has tracked their EPS almost perfectly in terms of growth rate since 2008. This means that their PE ratio has been fairly consistent in that time period.

Forecast:

The chart shows the historical prices for the previous 10 years and the forecast based on the average PE ratios and the expected EPS values. I have also included a forecast based off a PE ratio that is only 75% of the average low PE ratio for the previous 10 years. I like to the look to buy at the 75% Low PE price or lower to provide for additional margin of safety. Currently Mattel is trading at a $15 premium to the forecast.

Conclusion:

The average of all the valuation models gives a value of $31.52 which means that MAT is currently trading at a 7.50% premium to the fair value.

Overall I think that MAT is slightly overvalued at today's prices. If you can get into Mattel with a 4.00% YOC it might be tempting to take a chance on. That would mean a cost basis of $31.00 even. This wouldn't give you a good margin of safety but could still prove to be a solid beginning point. However do keep in mind that this might not be a great dividend growth stock due to their past inconsistencies in raising the dividend. But every company started at one point having just 4 years of consistent dividend growth. I would definitely want to check in on their latest earnings call to see what management had to say.

Comments

Post a Comment