Proctor & Gamble Dividend Stock Analysis

I'm going to revisit my previous dividend stock analysis on Procter & Gamble. It's been about a year so it's time for an update. I've learned so much more about stock analysis in that time so this will be more thorough and hopefully more insightful. They are a dividend champion with 56 consecutive years of increasing dividends. P&G closed trading on Wednesday, April 17th at $79.06.

Company Background (sourced from Yahoo! Finance):

The Procter & Gamble Company, together with its subsidiaries, engages in the manufacture and sale of a range of branded consumer packaged goods. The company operates in five segments: Beauty, Grooming, Health Care, Fabric Care and Home Care, and Baby Care and Family Care. The Beauty segment provides antiperspirants, deodorants, cosmetics, hair care products, hair colors, personal cleansings, prestige products, professional salon products, and skin care products primarily under the Head & Shoulders, Olay, Pantene, SK-II, and Wella brand names. The Grooming segment offers blades and razors, electronic hair removal devices, hair care appliances, and pre and post shave products primarily under the Braun, Fusion, Gillette, and Mach3 brand names. The Health Care segment provides feminine care, gastrointestinal, incontinence, rapid diagnostics, respiratory, toothbrush, toothpaste, oral care, and other personal health care products, as well as vitamins/minerals/supplements primarily under the Always, Crest, Oral-B, and Vicks brand names. The Fabric Care and Home Care segment offers bleach and laundry additives, air care products, batteries, dish care items, fabric enhancers, laundry detergents, pet care products, and surface care products primarily under the Ace, Ariel, Dawn, Downy, Duracell, Febreze, Gain, Iams, and Tide brand names. The Baby Care and Family Care segment provides baby wipes, diapers and pants, paper towels, tissues, and toilet papers primarily under the Bounty, Charmin, and Pampers brand names. The company markets its products through mass merchandisers, grocery stores, membership club stores, drug stores, high-frequency stores, department stores, perfumeries, pharmacies, salons, and e-commerce in approximately 180 countries worldwide. The Procter & Gamble Company has a strategic partnership with Verix, Inc. for building business intelligence capabilities.

DCF Valuation:

Analysts expect Procter & Gamble to grow earnings 7.88% per year for the next five years and I've assumed they can continue to grow at 3.50% per year thereafter. Running these numbers through a two stage DCF analysis with a 10% discount rate yields a fair value price of $73.69. This means the shares are trading at a 7.3% premium to the DCF.

Graham Number:

With a current book value per share of $23.99 and TTM EPS of $4.41, the Graham Number is calculated to be $48.79. Currently PG is trading for a 62.0% premium to the Graham Number.

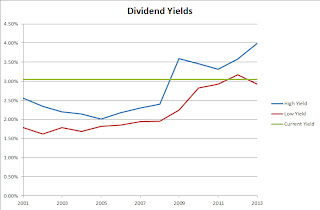

Average High Dividend Yield:

Procter & Gamble's average high dividend yield for the past 5 years is 3.27% and for the past 10 years is 2.72%. This gives target prices of $73.59 and $88.54 respectively based on the current annual dividend of $2.41. The 10 year average seems low to me based on what we can expect going forward. A lot of that is due to the overvaluation in the earlier part of the decade where the average high yield from 2003-2008 averaged 2.20%. I don't expect it to get back to that level, rather the 3.27% seems like a much more comfortable level so I'll use the 5 year average in my calculations.Procter & Gamble is currently trading at a 7.4% premium to my assumed average high dividend yield valuation.

Average Low PE Ratio:

Johnson and Johnson's average low PE ratio for the past 5 years is 14.29 and for the past 10 years is 16.79. This corresponds to a price per share of $57.86 and $68.00 respectively based off the analyst estimate of $4.05 per share for fiscal year 2013. Both historical averages are at reasonable levels and I'd feel comfortable purchasing near those price points. Procter & Gamble has traditionally commanded a premium in on a price-to-earnings basis and I'm fine with that since they are a steady grower that typically doesn't have big negative surprises in the operations of the company. For the sake of being conservative I'll use the 5 year average since it's lower, although I expect it to be closer to 16 in normal economic times. Currently PG is trading for a 36.6% premium to the 5 year P/E price target.

Average Low P/S Ratio:

Procter & Gamble's average low PS ratio for the past 5 years is 1.94 and for the past 10 years is 2.11. This corresponds to a price per share of $59.84 and $64.92 respectively based off the analyst estimate for revenue growth from FY 2012 to FY 2013. Currently, their current PS ratio is 2.63 on a trailing twelve months basis. I'll use the 5 year average in my calculations just to be conservative, although I think it will creep back up to over 2.00. PG is currently trading at a 21.8% premium to this price.

Dividend Discount Model:

For the DDM, I assumed that PG will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, 5 or 10 year growth rates. In this case that would be 9.55%. After that I assumed they can continue to raise dividends for 3 years at 75% of 9.55% or 7.16% and in perpetuity at 3.50%. The dividend growth rates are based off fiscal year payouts and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on the DDM, PG is worth $50.61, meaning it's overvalued by 56.2%.

PE Ratios:

Procer & Gamble's trailing PE is 17.93 and it's forward PE is 18.13. The PE3 based on the average earnings for the last 3 years is 20.27. I like to see the PE3 be less than 15 which PG is currently well over. Compared to it's industry, PG seems to be undervalued versus JNJ (21.74) and KMB (22.77) as well as the industry overall (20.41). All industry comparisons are on a TTM basis. PG's PEG for the next 5 years is currently at 2.48 while JNJ is at 2.30 and KMB is at 2.42. The industry as a whole carries a 2.14 PEG ratio. Based on the PEG ratio, PG is overvalued versus it's competitors and the industry as a whole, meaning you're paying more for the growth of PG.

Fundamentals:

PG's gross margins for FY 2011 and FY 2012 were 54.1% and 53.2% respectively. They have averaged a 54.6% gross profit margin since 2003 with a low of 52.9% in FY 2003. Their net income margin for the same years were 14.3% and 13.0%. Since 2003 their net income margin has averaged 13.9% with a low of 112.0% in FY 2003. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. PG is doing well on both margin fronts. Since each industry is different and allows for different margins, we'll see where they stand against the industry. For FY 2012, Procter & Gamble captured 97.1% of the gross margin for the industry and 117.1% of the net income margin. I'd like to see the gross margin comparison to come up, but it's good to see that despite the lower gross margin, their net income margin is well above the industry.

Share Buyback:

PG's shares outstanding have been decreasing the last 7 fiscal years, but has increased overall due to the split in FY 2006. Since the split in FY 2006, they've bought back a total of 10.5% of their outstanding shares for an annualized rate of 1.83%. By repurchasing shares, PG is able to increase EPS and management can return cash to shareholders this way by increasing the ownership stake of the company for all the outstanding shares. It was nice to see that the buyback program was increased during the "Great Recession" as management felt that the share price was depressed. I always like to see management making timely buyback moves because if the buyback is done when the share price is overvalued they are destroying shareholder value rather than increasing it.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Procter & Gamble is a dividend champion with 56 consecutive years of increases and recently announced an increase in their dividend. Their current annual dividend sits at $2.41 for a yield of 3.04%. PG's annual increases for the last 1, 3, 5 and 10 years have been 10.6%, 9.6%, 10.3% and 11.2%. These numbers are different from the actual quarterly increases since they are based off the dividends paid out during each fiscal year. Their payout ratio has averaged 44.0% since FY 2003, peaking in 2012 with a 58.5% ratio. I'd really like to see the payout ratio come down and using the average analyst estimate for FY 2013, the payout ratio is projected to be 59.5%. Having a low payout ratio leaves more room for management to increase the dividend without overly burdening the underlying business.

Procter & Gamble's free cash flow has been great since FY 2001 with every year having a positive cash flow. Their free cash flow payout ratio has averaged only 44.7% since FY 2003, which is right at their EPS payout ratio. However in FY 2011 and 2012 the FCF payout ratio was 59.6% and 67.5% respectively due to lower operating cash flow. Annual total shareholder return when accounting for buybacks plus dividends has averaged 112.5% of FCF since FY 2003, so clearly that can't continue. I expect the buyback program to be lowered unless they can increase the FCF. Total yield, % shares bought back + dividend yield has averaged a very solid 6.11% since FY 2008. It actually reached as high as 8.50% in FY 2009, which just goes to show how important it is to have cash available for special opportunities.

Return on Equity and Return on Capital Invested:

PG's ROE has averaged 17.1% since 2006 and has been very stable since then. Their ROCI has averaged a 12.3% since 2006 and like their ROE has been very stable over that time. I don't necessarily look for any absolute values, rather I like to see stable to increasing levels over the long term. I'd like to see it increasing, but these levels are still very solid. The dip is due to the stock split in FY 2005.

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how PG has done on that front. Their revenue growth since 2002 has been solid with a 7.60% annual increase and their net income has been growing at a 9.62% rate. Since their net income has been growing faster than revenue, their net income margin has increased from 10.82% to 13.03% between FY 2002 and FY 2012. Over that time, PG has had 2 years of decline in revenue , FY 2009 and FY 2010, with net income declining in the same years as well as in FY 2012. Revenue and net income are both projected to increase in FY 2013 which will be great to see them get back on track.

Forecast:

The chart shows the historical high and low prices since 2001 and the forecast based on the average PE ratios and the expected EPS values. I have also included a forecast based off a PE ratio that is only 75% of the average low PE ratio. I like to the look to buy at the 75% Low PE price or lower to provide for additional margin of safety, although this price doesn't come around very often. In this case the target low PE is 15.5 and the 0.75 * PE is 10.7. This corresponds to an entry price of $62.93 based off the expected earnings for FY 2013 of $4.05, with a 75% target price of $43.40. The average PE price would give a target price of $70.08. Currently PG is trading at a $35.66 premium to the 75% low PE target price and a $8.98 premium to the average PE price. If you believe the analyst estimates are pretty close, then PG is trading on the high end of it's typical range.

Conclusion:

The average of all the valuation models gives a target entry price of $61.58 which means that Procter & Gamble is currently trading at a 28.4% premium to the average.. I've also calculated it with the highest and lowest valuation methods thrown out. In this case, the DCF and Graham Number valuations are removed and the new average is $61.75. PG is trading at a 28.0% premium to this price as well.

Assuming that PG can grow their earnings and dividends at the rates that I assumed, you're looking at average returns over the next 10 years. In 2023, EPS would be $6.78 and slapping an average PE of 17.30 gives a price of $117.25. Over the next 10 years you'd also receive $38.89 in dividends for a total return of 197.50% which is good for a 7.04% annualized rate. If you purchase at my target entry price of $61.75, your projected 10 year total return jumps to 252.86% for an annualized return of 9.72%.

Overall, I would say that Procter & Gamble is currently overvalued, or at least on the high end of the fair value range. I wish I had re-analyzed PG before now, because I would have been a buyer last year. The biggest question marks with PG from an investment standpoint are the increasing payout ratios, both off EPS and FCF, and the decline in operating cash flow. With the "Great Recession" further behind us, hopefully net income will begin to increase once again. If you think that that's a reason PG became a consumer staple giant and will continue to do so in the future, then now could be a decent time to initiate a position and look to buy on a pullback. The biggest driver of growth going forward will need to be the international/emerging markets. They've started to focus more on marketing their product line to the needs of the faster developing nations and success here will make up the majority of the growth for the company. Based on the average of it's typical yield, P/E, and P/S ratios it should trade around $76.25 and the high valuation level would be around $84.60. I'll be looking to add to my position but would like to see the price come down to at least the low $70's before considering a purchase. If there is a decline to that level, I'd probably go the route of setting a "limit order" through selling a put option.

To check out more reports check out my Stock Analysis page.

What do you think about Procter & Gamble as a DG investment at today's prices?

Company Background (sourced from Yahoo! Finance):

The Procter & Gamble Company, together with its subsidiaries, engages in the manufacture and sale of a range of branded consumer packaged goods. The company operates in five segments: Beauty, Grooming, Health Care, Fabric Care and Home Care, and Baby Care and Family Care. The Beauty segment provides antiperspirants, deodorants, cosmetics, hair care products, hair colors, personal cleansings, prestige products, professional salon products, and skin care products primarily under the Head & Shoulders, Olay, Pantene, SK-II, and Wella brand names. The Grooming segment offers blades and razors, electronic hair removal devices, hair care appliances, and pre and post shave products primarily under the Braun, Fusion, Gillette, and Mach3 brand names. The Health Care segment provides feminine care, gastrointestinal, incontinence, rapid diagnostics, respiratory, toothbrush, toothpaste, oral care, and other personal health care products, as well as vitamins/minerals/supplements primarily under the Always, Crest, Oral-B, and Vicks brand names. The Fabric Care and Home Care segment offers bleach and laundry additives, air care products, batteries, dish care items, fabric enhancers, laundry detergents, pet care products, and surface care products primarily under the Ace, Ariel, Dawn, Downy, Duracell, Febreze, Gain, Iams, and Tide brand names. The Baby Care and Family Care segment provides baby wipes, diapers and pants, paper towels, tissues, and toilet papers primarily under the Bounty, Charmin, and Pampers brand names. The company markets its products through mass merchandisers, grocery stores, membership club stores, drug stores, high-frequency stores, department stores, perfumeries, pharmacies, salons, and e-commerce in approximately 180 countries worldwide. The Procter & Gamble Company has a strategic partnership with Verix, Inc. for building business intelligence capabilities.

DCF Valuation:

Analysts expect Procter & Gamble to grow earnings 7.88% per year for the next five years and I've assumed they can continue to grow at 3.50% per year thereafter. Running these numbers through a two stage DCF analysis with a 10% discount rate yields a fair value price of $73.69. This means the shares are trading at a 7.3% premium to the DCF.

Graham Number:

With a current book value per share of $23.99 and TTM EPS of $4.41, the Graham Number is calculated to be $48.79. Currently PG is trading for a 62.0% premium to the Graham Number.

Average High Dividend Yield:

Procter & Gamble's average high dividend yield for the past 5 years is 3.27% and for the past 10 years is 2.72%. This gives target prices of $73.59 and $88.54 respectively based on the current annual dividend of $2.41. The 10 year average seems low to me based on what we can expect going forward. A lot of that is due to the overvaluation in the earlier part of the decade where the average high yield from 2003-2008 averaged 2.20%. I don't expect it to get back to that level, rather the 3.27% seems like a much more comfortable level so I'll use the 5 year average in my calculations.Procter & Gamble is currently trading at a 7.4% premium to my assumed average high dividend yield valuation.

Johnson and Johnson's average low PE ratio for the past 5 years is 14.29 and for the past 10 years is 16.79. This corresponds to a price per share of $57.86 and $68.00 respectively based off the analyst estimate of $4.05 per share for fiscal year 2013. Both historical averages are at reasonable levels and I'd feel comfortable purchasing near those price points. Procter & Gamble has traditionally commanded a premium in on a price-to-earnings basis and I'm fine with that since they are a steady grower that typically doesn't have big negative surprises in the operations of the company. For the sake of being conservative I'll use the 5 year average since it's lower, although I expect it to be closer to 16 in normal economic times. Currently PG is trading for a 36.6% premium to the 5 year P/E price target.

Average Low P/S Ratio:

Procter & Gamble's average low PS ratio for the past 5 years is 1.94 and for the past 10 years is 2.11. This corresponds to a price per share of $59.84 and $64.92 respectively based off the analyst estimate for revenue growth from FY 2012 to FY 2013. Currently, their current PS ratio is 2.63 on a trailing twelve months basis. I'll use the 5 year average in my calculations just to be conservative, although I think it will creep back up to over 2.00. PG is currently trading at a 21.8% premium to this price.

Dividend Discount Model:

For the DDM, I assumed that PG will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, 5 or 10 year growth rates. In this case that would be 9.55%. After that I assumed they can continue to raise dividends for 3 years at 75% of 9.55% or 7.16% and in perpetuity at 3.50%. The dividend growth rates are based off fiscal year payouts and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on the DDM, PG is worth $50.61, meaning it's overvalued by 56.2%.

PE Ratios:

Procer & Gamble's trailing PE is 17.93 and it's forward PE is 18.13. The PE3 based on the average earnings for the last 3 years is 20.27. I like to see the PE3 be less than 15 which PG is currently well over. Compared to it's industry, PG seems to be undervalued versus JNJ (21.74) and KMB (22.77) as well as the industry overall (20.41). All industry comparisons are on a TTM basis. PG's PEG for the next 5 years is currently at 2.48 while JNJ is at 2.30 and KMB is at 2.42. The industry as a whole carries a 2.14 PEG ratio. Based on the PEG ratio, PG is overvalued versus it's competitors and the industry as a whole, meaning you're paying more for the growth of PG.

Fundamentals:

PG's gross margins for FY 2011 and FY 2012 were 54.1% and 53.2% respectively. They have averaged a 54.6% gross profit margin since 2003 with a low of 52.9% in FY 2003. Their net income margin for the same years were 14.3% and 13.0%. Since 2003 their net income margin has averaged 13.9% with a low of 112.0% in FY 2003. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. PG is doing well on both margin fronts. Since each industry is different and allows for different margins, we'll see where they stand against the industry. For FY 2012, Procter & Gamble captured 97.1% of the gross margin for the industry and 117.1% of the net income margin. I'd like to see the gross margin comparison to come up, but it's good to see that despite the lower gross margin, their net income margin is well above the industry.

Share Buyback:

PG's shares outstanding have been decreasing the last 7 fiscal years, but has increased overall due to the split in FY 2006. Since the split in FY 2006, they've bought back a total of 10.5% of their outstanding shares for an annualized rate of 1.83%. By repurchasing shares, PG is able to increase EPS and management can return cash to shareholders this way by increasing the ownership stake of the company for all the outstanding shares. It was nice to see that the buyback program was increased during the "Great Recession" as management felt that the share price was depressed. I always like to see management making timely buyback moves because if the buyback is done when the share price is overvalued they are destroying shareholder value rather than increasing it.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Procter & Gamble is a dividend champion with 56 consecutive years of increases and recently announced an increase in their dividend. Their current annual dividend sits at $2.41 for a yield of 3.04%. PG's annual increases for the last 1, 3, 5 and 10 years have been 10.6%, 9.6%, 10.3% and 11.2%. These numbers are different from the actual quarterly increases since they are based off the dividends paid out during each fiscal year. Their payout ratio has averaged 44.0% since FY 2003, peaking in 2012 with a 58.5% ratio. I'd really like to see the payout ratio come down and using the average analyst estimate for FY 2013, the payout ratio is projected to be 59.5%. Having a low payout ratio leaves more room for management to increase the dividend without overly burdening the underlying business.

Procter & Gamble's free cash flow has been great since FY 2001 with every year having a positive cash flow. Their free cash flow payout ratio has averaged only 44.7% since FY 2003, which is right at their EPS payout ratio. However in FY 2011 and 2012 the FCF payout ratio was 59.6% and 67.5% respectively due to lower operating cash flow. Annual total shareholder return when accounting for buybacks plus dividends has averaged 112.5% of FCF since FY 2003, so clearly that can't continue. I expect the buyback program to be lowered unless they can increase the FCF. Total yield, % shares bought back + dividend yield has averaged a very solid 6.11% since FY 2008. It actually reached as high as 8.50% in FY 2009, which just goes to show how important it is to have cash available for special opportunities.

Return on Equity and Return on Capital Invested:

PG's ROE has averaged 17.1% since 2006 and has been very stable since then. Their ROCI has averaged a 12.3% since 2006 and like their ROE has been very stable over that time. I don't necessarily look for any absolute values, rather I like to see stable to increasing levels over the long term. I'd like to see it increasing, but these levels are still very solid. The dip is due to the stock split in FY 2005.

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how PG has done on that front. Their revenue growth since 2002 has been solid with a 7.60% annual increase and their net income has been growing at a 9.62% rate. Since their net income has been growing faster than revenue, their net income margin has increased from 10.82% to 13.03% between FY 2002 and FY 2012. Over that time, PG has had 2 years of decline in revenue , FY 2009 and FY 2010, with net income declining in the same years as well as in FY 2012. Revenue and net income are both projected to increase in FY 2013 which will be great to see them get back on track.

Forecast:

Conclusion:

The average of all the valuation models gives a target entry price of $61.58 which means that Procter & Gamble is currently trading at a 28.4% premium to the average.. I've also calculated it with the highest and lowest valuation methods thrown out. In this case, the DCF and Graham Number valuations are removed and the new average is $61.75. PG is trading at a 28.0% premium to this price as well.

Assuming that PG can grow their earnings and dividends at the rates that I assumed, you're looking at average returns over the next 10 years. In 2023, EPS would be $6.78 and slapping an average PE of 17.30 gives a price of $117.25. Over the next 10 years you'd also receive $38.89 in dividends for a total return of 197.50% which is good for a 7.04% annualized rate. If you purchase at my target entry price of $61.75, your projected 10 year total return jumps to 252.86% for an annualized return of 9.72%.

Overall, I would say that Procter & Gamble is currently overvalued, or at least on the high end of the fair value range. I wish I had re-analyzed PG before now, because I would have been a buyer last year. The biggest question marks with PG from an investment standpoint are the increasing payout ratios, both off EPS and FCF, and the decline in operating cash flow. With the "Great Recession" further behind us, hopefully net income will begin to increase once again. If you think that that's a reason PG became a consumer staple giant and will continue to do so in the future, then now could be a decent time to initiate a position and look to buy on a pullback. The biggest driver of growth going forward will need to be the international/emerging markets. They've started to focus more on marketing their product line to the needs of the faster developing nations and success here will make up the majority of the growth for the company. Based on the average of it's typical yield, P/E, and P/S ratios it should trade around $76.25 and the high valuation level would be around $84.60. I'll be looking to add to my position but would like to see the price come down to at least the low $70's before considering a purchase. If there is a decline to that level, I'd probably go the route of setting a "limit order" through selling a put option.

To check out more reports check out my Stock Analysis page.

What do you think about Procter & Gamble as a DG investment at today's prices?

Like you, I feel that PG is on the overvalued side. I wish I would have invested in it earlier too. But a man only has so much capital. Incidentally, my PG analysis is supposed to go live on Monday and basically agrees with yours.

ReplyDeleteThanks for this analysis!

MyFIJ,

DeleteUnfortunately it's on the overvalued side because I'd love to get some more exposure to PG. I knew this was going to be the case going into the analysis, but I needed to revisit and figure out my valuation ranges and prices targets in case there's a drop.

That's funny that your analysis on PG will be coming out on Monday. It's always great to get some confirmation on my analyses, at least I'm not the only one thinking that way. I remember about 2-3 weeks ago you and Dividend Growth Stock Investing had an analysis on LO released on the same day.

Thanks for stopping by!

I love this business, but not at this price and effective yield. I'd rather deploy my capital elsewhere for the moment. I agree with your conclusion of overvaluation

ReplyDeleteIntegrator,

DeleteI'm in the same boat as you. The value just isn't there and there's no room for error at current prices. I'll gladly put capital to work elsewhere for now and just wait for the chance when PG becomes better priced.

Thanks for stopping by!

I agree with you; love the company, dislike the price it's been traded at ;-)

ReplyDeleteI guess PG is also getting a premium due to its business model and dividend payout stability in such a volatile market. I've seen a similar situation with Coca-Cola recently (I own shares of KO).

I would definitely wait to buy PG but I'm afraid the stock won't drop by 20%...

Dividend Guy,

DeleteNo kidding! The price is way too high for my liking right now. I can't believe I didn't pick up PG and JNJ last year, but live and learn. I won't make that mistake again.

I'll gladly take a 20% haircut but that could be a while. We might have to settle for 10%, although who knows when that will happen too.

Thanks for stopping by!

Nice analysis. I agree that PG is slightly overvalued right now. I'm satisfied with the size of my position, so I will just continue to hold. The price would have to drop to below $70 before I would give serious consideration to buying more shares.

ReplyDeleteDGM,

DeleteI should have been adding before but just never did. I got wrapped up in looking for other stocks when there was a perfectly good value proposition staring me in the face. I didn't want to average up my cost basis and I think that was part of the reason that I didn't purchase more shares. Live and learn and I won't make that mistake again. If it gets down to the low $70's I'll be seriously considering adding to my position but not too heavily, I'd want to see the mid-$60's before backing up the truck.

Thanks for stopping by!