Income Update - March 2013

This year has been just amazing. My income has been way up and that has helped to contribute to so many of my goals for 2013. I did really good in March on controlling the expenses, and brought them back in line with January after February's increase due to the cell phone billing issue. I was actually under both my groceries and restaurant budgets for the month, which rarely happens. I can usually keep one under but that's because the other is over. My minimum expenses came in at $1,314.30 which lowered my average thus far in 2013 to $1,372.94 which is currently under my goal of sub-$1,400. My total expenses for March ended at $1,481.64. This was a little higher than I wanted but I needed some new running shoes if I want to stay on track with my weight loss goal. My average total monthly expenses for 2013 sit at $1,512.32 and should hopefully keep coming down.

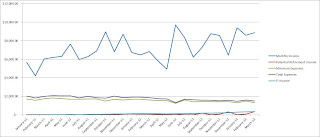

As mentioned in my March dividend update, I received $352.33 in dividends and counting interest income of $3.72, my total potential retirement income came in at $356.05. This covered 27.09% of my minimum expenses for March. The 30 year treasury yield ended March at 3.10%. Based on this my FI number, monthly income that could be generated using liquid net worth invested in the 30 year Treasury bond, would generate $337.64 in monthly income. This would cover 25.69% of my minimum expenses from March.

*Minimum Expenses are only the expenses related to rent, utilities, car, food, minimum payment on debt and other necessities. In other words, the required amount of replacement income I would need for financial independence.

*Total Expenses are the total monthly outflow of money.

*Potential Retirement Income is income received from dividends, interest, cash back from credit card purchases and any other source of income not related to my job.

*FI is my liquid net worth invested at the 30 year treasury bond yield at the end of each month divided by 12 to get monthly income.

I've updated my Progress page to reflect March's changes.

How did you do on your budget for the month? Is there anything you're going to focus more on in April due to March's expenses?

As mentioned in my March dividend update, I received $352.33 in dividends and counting interest income of $3.72, my total potential retirement income came in at $356.05. This covered 27.09% of my minimum expenses for March. The 30 year treasury yield ended March at 3.10%. Based on this my FI number, monthly income that could be generated using liquid net worth invested in the 30 year Treasury bond, would generate $337.64 in monthly income. This would cover 25.69% of my minimum expenses from March.

*Minimum Expenses are only the expenses related to rent, utilities, car, food, minimum payment on debt and other necessities. In other words, the required amount of replacement income I would need for financial independence.

*Total Expenses are the total monthly outflow of money.

*Potential Retirement Income is income received from dividends, interest, cash back from credit card purchases and any other source of income not related to my job.

*FI is my liquid net worth invested at the 30 year treasury bond yield at the end of each month divided by 12 to get monthly income.

| Category | Amount |

|---|---|

| Paycheck | $7,898.01 |

| Expense Check | $963.12 |

| TOTAL | $8,861.13 |

| Category | Budgeted Amount | Actual Amount | Subtotal |

|---|---|---|---|

| Rent | $480.00 | $480.00 | |

| Utilities | $220.58 | $130.25 | |

| Gas | $150.00 | $93.41 | |

| Car Insurance | $95.00 | $95.00 | |

| Groceries | $200.00 | $197.85 | |

| Restaurants | $125.00 | $87.21 | |

| Entertainment | $0.00 | $19.00 | |

| Cell Phone | $95.00 | $92.35 | |

| Other | $49.06 | $49.06 | |

| Miscellaneous | $55.00 | $132.14 | |

| Gifts | $0.00 | $5.37 | |

| EXPENSES SUBTOTAL | $1,381.64 | ||

| SAVINGS | |||

| Trip | $300.00 | $300.00 | |

| Roth IRA | $0.00 | $0.00 | |

| Emergency Fund | $0.00 | $88.00 | |

| Gifts | $50.00 | $50.00 | |

| FI savings | $6,941.49 | $6,941.49 | |

| Car Maint/Repair | $100.00 | $100.00 | |

| SAVINGS SUBTOTAL | $7,479.49 | ||

| TOTAL | $8,861.13 |

I've updated my Progress page to reflect March's changes.

How did you do on your budget for the month? Is there anything you're going to focus more on in April due to March's expenses?

Pursuit,

ReplyDeleteGreat job man! You're killing it month after month. I need a higher paying job! :)

I saved 57% of my net income this month due to an income that was below average, and higher expenses due to travel. Overall, still averaging 60% on the year, however.

Keep up the great work!!

Best wishes.

DM,

DeleteThe higher paying job really helps to juice the investment account. It's great getting to add a really good chunk every month to the account and get it working for me. Great job averaging 60% for the year, I know you've had some non-recurring expenses so far this year so it should only go up from here.

Thanks for stopping by!

I think you should also include your dividend income and options income in the totals. However, it is amazing how a high paying job can do wonders for saving money and achieving FI.

DeleteOn a side note, have you tried selling naked puts?

DGI,

DeleteI've thought about adding the dividend and option income in the totals but think for now I'm not going to. The dividends and option income don't ever leave my account and I'm more worried about cash that actually hits my checking account because that is the money that is most likely to find other uses for. That's the same reason that I don't count my ESPP withholding because that cash is directly withheld from my paycheck, but that would be an extra 8% to my after-tax savings rate.

I recently got margin added to my account to let me start selling naked puts. I've got a few of them open right now but am holding off on selling more for the time being because I don't want to be over=leveraged should a drop in the market come. If the market does pull back then I'll feel a little better about selling some more naked puts, although I'll probably end up going through a lot of my cash to make buys. I really like naked puts though because the cash-secured route leaves too much capital sitting idle and it just taunts me knowing that I can't use it.

Thanks for stopping by!

You are going to find Financial Independence very soon with numbers like this my friend. I'm pumped for you, I just told my wife how awesome it would be to have low expenses like you do!

ReplyDeleteMarvin,

DeleteI certainly hope so. I actually just crossed the $100k mark for my FI portfolio in about 1 year 8 months. I figure that I need to take advantage of the great opportunity of a high income and low necessary expenses with not having any children in the picture, because they will certainly change things. Keep up the good work yourself!

Thanks for stopping by!