Income Update - February 2015

I'm a big proponent of tracking every single penny that comes into your hands if you're really wanting to make a change to your finances. Mental accounting is too difficult to keep track of and the mundane everyday expenses get forgotten. Once you keep a detailed history you can see that you're really spending $400 per month on restaurants or $100 on coffee or whatever little expenses that are fine by themselves but add up quickly to destroy a budget. This is why I like to keep track of all of my expenses to help keep myself accountable and looking to see what areas I'm just plain doing poor in. If you want to improve your finances, then please track everything for a 3 month span and then take action to make positive changes.

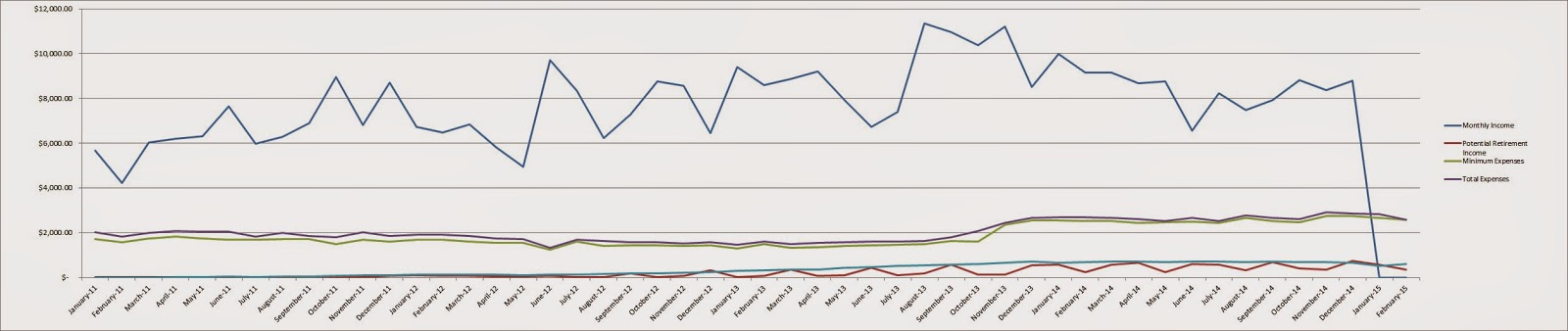

Well February wasn't exactly a great way to get back into the swing of things. The first thing you'll notice is the bag fat zero in the income column. Since I was on FMLA to be with my son that unfortunately meant we would have no income coming in. Luckily we had planned on this already and had ample cash savings built up as an emergency fund so we didn't struggle financially. So there were no extra savings to be had in February. March will fix that as I try to build up some more cash savings, well if I can keep myself from purchasing dividend growth stocks.

Total expenses for February came in at $2,587.82. Not horrible since it was in line with where the previous months had been while I was on FMLA. One big reason that expenses were so high was the restaurant spending. Since we're still spending every day at the hospital, well my wife every day and me every day that I'm not working, we end up eating out at restaurants at least one meal each day. That adds up quick and isn't good for the budget or the waist line. But hey, at least our gas spending came in under budget!

Dividends and other income was okay during February, although dividends did all of the heavy lifting since interest on savings was the only other passive income during the month. Dividends came in at $356.74 and I received another $1.98 in interest bringing our passive income for the month to $358.72. Passive income sources covered 13.86% of expenses for February. There's still a long way to go to reach 100% but I'm working on it slowly but surely. As a dividend growth investor seeking financial independence, my goal is to eventually have enough dividend income coming in on a monthly basis to cover all of my expenses and allow me to consider early retirement. So it's great to see that the long-term trend is higher.

My FI Income, monthly income based on the 30 year US Treasury bond yield of 2.60% using my net worth excluding traditional retirement accounts, came in at $596.68. That ended up being almost a $90 increase from January 2015. A good portion of the increase was due to the Treasury yield jumping from 2.20% to 2.60% but my net worth increasing also played a big role. FI income covered 23.06% of February's expenses.

*Minimum Expenses are only the expenses related to rent, utilities, car, food, minimum payment on debt and other necessities. In other words, the required amount of replacement income I would need for financial independence.

*Total Expenses are the total monthly outflow of money.

*Potential Retirement Income is income received from dividends, interest, cash back from credit card purchases and any other source of income not related to my job.

*FI Income is my liquid net worth invested at the 30 year treasury bond yield at the end of each month divided by 12 to get monthly income.

*Savings that is earmarked to be spent.

**Expenses shown above are only expenses that I paid for. My wife and I have split our expenses up due to my job having me out of town most of each month. The current split is around 65/35.

***Expenses shown are all expenses except for charges that are explicitly medical related, i.e. doctor/hospital bills.

Overall it was a decent month for my budget and a much welcomed normalization of total expenses after the last few months were well over budget. I'm hoping that November will build on the progress from October but I'm not going to be surprised at an increase in expenses either.

I've updated my Progress page to reflect February's changes.

Be sure to not miss out on any posts from Passive-Income-Pursuit and sign up to receive them by email. Also make sure to follow me on Twitter@JC_PIP.

How did you do on your budget for the month? Are you getting started off on the right track for your budgeting goals for the year?

Well February wasn't exactly a great way to get back into the swing of things. The first thing you'll notice is the bag fat zero in the income column. Since I was on FMLA to be with my son that unfortunately meant we would have no income coming in. Luckily we had planned on this already and had ample cash savings built up as an emergency fund so we didn't struggle financially. So there were no extra savings to be had in February. March will fix that as I try to build up some more cash savings, well if I can keep myself from purchasing dividend growth stocks.

Total expenses for February came in at $2,587.82. Not horrible since it was in line with where the previous months had been while I was on FMLA. One big reason that expenses were so high was the restaurant spending. Since we're still spending every day at the hospital, well my wife every day and me every day that I'm not working, we end up eating out at restaurants at least one meal each day. That adds up quick and isn't good for the budget or the waist line. But hey, at least our gas spending came in under budget!

Dividends and other income was okay during February, although dividends did all of the heavy lifting since interest on savings was the only other passive income during the month. Dividends came in at $356.74 and I received another $1.98 in interest bringing our passive income for the month to $358.72. Passive income sources covered 13.86% of expenses for February. There's still a long way to go to reach 100% but I'm working on it slowly but surely. As a dividend growth investor seeking financial independence, my goal is to eventually have enough dividend income coming in on a monthly basis to cover all of my expenses and allow me to consider early retirement. So it's great to see that the long-term trend is higher.

My FI Income, monthly income based on the 30 year US Treasury bond yield of 2.60% using my net worth excluding traditional retirement accounts, came in at $596.68. That ended up being almost a $90 increase from January 2015. A good portion of the increase was due to the Treasury yield jumping from 2.20% to 2.60% but my net worth increasing also played a big role. FI income covered 23.06% of February's expenses.

*Minimum Expenses are only the expenses related to rent, utilities, car, food, minimum payment on debt and other necessities. In other words, the required amount of replacement income I would need for financial independence.

*Total Expenses are the total monthly outflow of money.

*Potential Retirement Income is income received from dividends, interest, cash back from credit card purchases and any other source of income not related to my job.

*FI Income is my liquid net worth invested at the 30 year treasury bond yield at the end of each month divided by 12 to get monthly income.

| Category | Amount |

|---|---|

| Paycheck | $0.00 |

| Expense Check | $0.00 |

| TOTAL | $0.00 |

| Category | Budgeted Amount | Actual Amount | Subtotal |

|---|---|---|---|

| Mortgage | $911.84 | $911.84 | |

| House Insurance | $127.92 | $127.92 | |

| Property Taxes | $371.08 | $371.08 | |

| Gas | $175.00 | $101.83 | |

| Car Insurance | $224.83 | $224.83 | |

| Groceries | $200.00 | $209.70 | |

| Restaurants | $100.00 | $473.71 | |

| Bars | $0.00 | $0.00 | |

| Debt Payment (Fridge) | $0.00 | $0.00 | |

| Cell Phone | $10.81 | $10.81 | |

| Gym Membership | $40.00 | $40.00 | |

| Miscellaneous | $55.00 | $116.10 | |

| Gifts* | -- | -- | |

| Car Maint./Repair* | -- | -- | |

| Trip* | -- | -- | |

| EXPENSES SUBTOTAL | $2,587.82 | ||

| Emergency Fund | -- | -- | |

| Investing | $0.00 | $0.00 | |

| SAVINGS SUBTOTAL | $0.00 | ||

| TOTAL | $2.587.82T |

**Expenses shown above are only expenses that I paid for. My wife and I have split our expenses up due to my job having me out of town most of each month. The current split is around 65/35.

***Expenses shown are all expenses except for charges that are explicitly medical related, i.e. doctor/hospital bills.

Overall it was a decent month for my budget and a much welcomed normalization of total expenses after the last few months were well over budget. I'm hoping that November will build on the progress from October but I'm not going to be surprised at an increase in expenses either.

I've updated my Progress page to reflect February's changes.

Be sure to not miss out on any posts from Passive-Income-Pursuit and sign up to receive them by email. Also make sure to follow me on Twitter@JC_PIP.

How did you do on your budget for the month? Are you getting started off on the right track for your budgeting goals for the year?

You're doing great. This is what we all prepare for. It's unfortunate that it's happened, but you're going to make it through this challenge. I wish the best for your family in this tough time.

ReplyDeleteI see a $0 amount for monthly income? Is that normal?

ReplyDeleteBest of luck with your son, and its ok to not invest when medical emergencies take over. I was a bit confused between your dividend income and FI income, but I later saw the asterisk with the explanation. Hopefully things change for the best.

ReplyDelete