Moody's Corporation: The More It Drops The Better It Looks $MCO

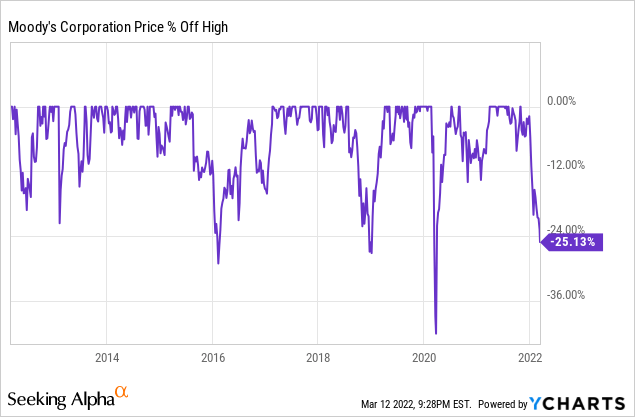

Moody's Corporation (MCO) is a business I've had my eye on for quite some time, but could never wrap my head around the valuation. With the share price off 25% since the late October high, and in the 4th deepest drawdown of the last decade, I wanted to take another look at this company to see if now could be the time to add shares to my portfolio.

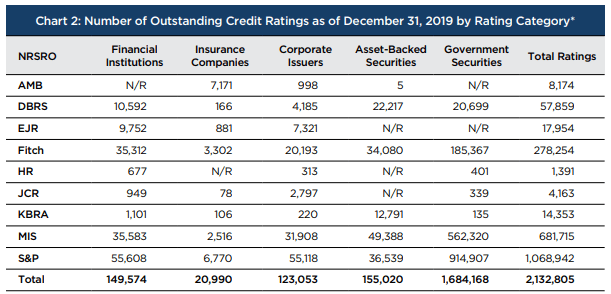

The 3 largest players in the credit ratings space are Moody's, S&P Global, and Fitch. As we can see, S&P is by far the leader in terms of ongoing ratings with ~50% market share, while Moody's is second with ~32% market share. Fitch comes in around 13%. Combined those 3 account for ~95% of the ongoing ratings.

FY 2020 OCG Annual Report on NRSROs

The top players don't necessarily fiercely compete with each other since nearly all major issuances will be rated by 2 of the big 3.

Their client businesses aren't necessarily tied to Moody's; however, they will receive lower interest rates on debt offerings when they have a rating from one of the major agencies and the lower debt service payments far outweigh the fees paid to Moody's.

Moody's is organized in two operating segments: (1) Moody's Investors Service MIS - which provides initial and ongoing ratings on debt offerings, and (2) Moody's Analytics MA - which provides portfolio modeling, data, and risk managements capabilities to institutional investors.

MIS is expected to grow slower in the low-to-mid single digit range, but carries higher margins. Meanwhile, the MA segment is expected to show faster topline growth but carries lower margins.

Comments

Post a Comment