Net Worth Update - July 2014

While cash flow is more important when it comes to financial independence, it's still good to look at the balance sheet too, which is why I provide these net worth updates. The S&P 500 was down 2.16% during July although the real action came on the last day as the S&P 500 saw a 2.00% drop sparking worries of a correction being underway. Since more and more of my net worth is tied to the markets, there's a larger correlation between my net worth and the markets and for July my net worth suffered. As a dividend growth investor I'm not overly concerned with the short-term gyrations as long as the dividend stream remains in tact, but the markets' effect is noticeable. I had just under $5,700 in after-tax savings from my paycheck, almost $900 in ESPP contributions, and just over $1,200 in 401k contributions counting the employer match. The rest of the changes were due to dividends received and changes in the stock market. All in all July saw a $5,412.25 decrease in my net worth. Yikes!

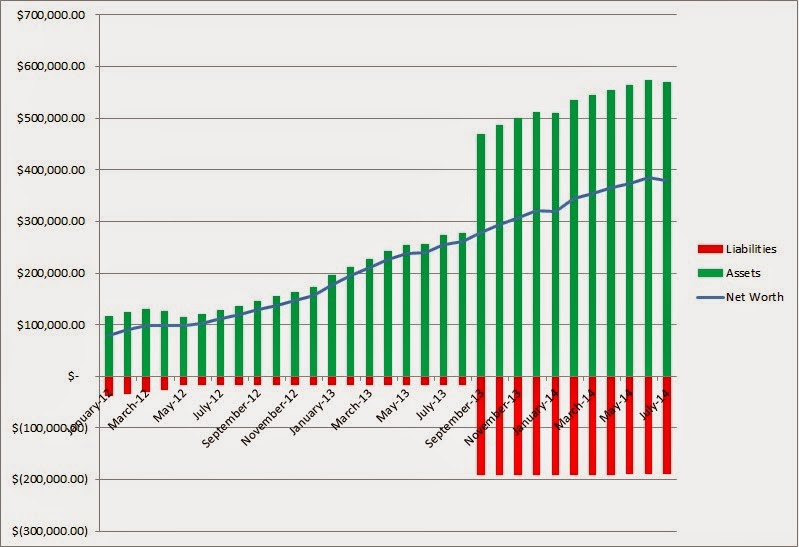

Current Assets: $568,957.53

Curent Liquid Assets: $187,305.01

Current Debts: -$189,536.61

Net Worth: $379,420.92

I had put together a nice string of increases since January but July had something different in store. What's good to see, at least from my point of view, is that my net worth decreased only $5,400 in a down month for the markets. If you add back in the $5,000 we spent on the down payment for my wife's new Acura RDX then it was essentially a flat month. The asset side will eventually turn back positive so I'm not worried about it at all over the short term. Liabilities are pretty much just the mortgage on our house which we now have 21.02% equity in our house. I don't see the point in paying extra on the mortgage given our relatively low interest rate and think we'll come out much further ahead investing extra cash flow for the time being.

July's net worth decreased 1.41% from the end of June and year-to-date I've had an increase of $59,306.70. My goal for the year is to have a $125k increase but that might be in jeopardy with the backtrack this month. I'm now 47.45% of the way towards my goal but we're 58% of the way through the year. The net worth goal is more of a secondary goal since so much of it is out of my hands. I can maintain a large savings rate and invest those savings but I can't make the markets go up. And I have no idea where they go from here. If they continue to march higher or even stay flat then there's a chance I can still reach my goal but if they trend down the rest of the year it's probably not likely. Although I'd prefer that so I can get some better long term values when I invest my capital.

I've changed the chart for my net worth to better reflect our situation now that there's significant debt on the books with our mortgage. The chart will now show both assets and liabilities as well as the net worth. I also changed the colors because I didn't notice this until April but assets were red and liabilities were green. So that's now been fixed.

My after-tax savings rate for July came in at 69.47% which is well over my goal of50% 65%. I revised my goal higher during my mid year goal checkup and July was almost right on pace to get me to my new goal. I don't expect to have too many other big expenses or items to save for the rest of this year so almost all excess cash flow will be funneled directly into savings for investment purposes. This should help increase my savings rate throughout the rest of the year. This is a big drop-off from 2013's 81.31% rate, but that's because I changed the way I calculate my savings rate. It's now just savings from my after-tax income that is specifically marked for investment. I think this gives a "purer" savings rate since it's only true savings/investment capital from my after tax income.

Based on my expenses from July, my liquid savings would last for 6.22 years, a 0.26 year increase from June. I'm glad to get this moving back in the right direction after June's decline ended a 4 month streak of increases. The increase was mainly due to the drop in expenses from June to July. But I'll take it where I can. The direction is at least right.

I've updated my Progress page to reflect July's changes.

Make sure you sign up to receive new posts to your email so you don't miss anything. And be sure to follow me on Twitter@JC_PIP to get up to the minute news of new purchases for my portfolio.

How did your net worth do in July?

Current Assets: $568,957.53

Curent Liquid Assets: $187,305.01

Current Debts: -$189,536.61

Net Worth: $379,420.92

I had put together a nice string of increases since January but July had something different in store. What's good to see, at least from my point of view, is that my net worth decreased only $5,400 in a down month for the markets. If you add back in the $5,000 we spent on the down payment for my wife's new Acura RDX then it was essentially a flat month. The asset side will eventually turn back positive so I'm not worried about it at all over the short term. Liabilities are pretty much just the mortgage on our house which we now have 21.02% equity in our house. I don't see the point in paying extra on the mortgage given our relatively low interest rate and think we'll come out much further ahead investing extra cash flow for the time being.

July's net worth decreased 1.41% from the end of June and year-to-date I've had an increase of $59,306.70. My goal for the year is to have a $125k increase but that might be in jeopardy with the backtrack this month. I'm now 47.45% of the way towards my goal but we're 58% of the way through the year. The net worth goal is more of a secondary goal since so much of it is out of my hands. I can maintain a large savings rate and invest those savings but I can't make the markets go up. And I have no idea where they go from here. If they continue to march higher or even stay flat then there's a chance I can still reach my goal but if they trend down the rest of the year it's probably not likely. Although I'd prefer that so I can get some better long term values when I invest my capital.

I've changed the chart for my net worth to better reflect our situation now that there's significant debt on the books with our mortgage. The chart will now show both assets and liabilities as well as the net worth. I also changed the colors because I didn't notice this until April but assets were red and liabilities were green. So that's now been fixed.

My after-tax savings rate for July came in at 69.47% which is well over my goal of

Based on my expenses from July, my liquid savings would last for 6.22 years, a 0.26 year increase from June. I'm glad to get this moving back in the right direction after June's decline ended a 4 month streak of increases. The increase was mainly due to the drop in expenses from June to July. But I'll take it where I can. The direction is at least right.

Make sure you sign up to receive new posts to your email so you don't miss anything. And be sure to follow me on Twitter@JC_PIP to get up to the minute news of new purchases for my portfolio.

How did your net worth do in July?

Yeah the markets seem to be going down the last few days. It's not strange considering all the turmoil in the world these days. But hey, like you said, that provides DG investors the opportunity with better long term investments.

ReplyDeleteDividend Dream,

DeleteYeah the end of July was pretty rough for the US markets but I was glad to see it happen. I ended up investing about $9.5k of my cash that had been on the sidelines. So my forward dividend income made a nice jump.

Thanks for stopping by!

July has been a roadblock for lot of people, but I like it since I can get more stocks for the same capital. Investing close of 10K in a month is wonderful. Congrats.

ReplyDeleteDGJ

DGJ,

DeleteJust a minor blip in the long term. Like you I was quite excited to be able to buy more shares for the same amount of capital.

Thanks for stopping by!

Thanks for sharing your recent net worth update with us. You can't sweat month over month decreases especially when a lot of your net worth is tied to a very volatile and fluctuating stock market. As long as those dividends keep rolling in you are ahead of most and doing OK but I know you already know that. I think you are also on the right track regarding your mortgage too. If you have a very low rate you're better off putting that extra money to work elsewhere. Till your next update!

ReplyDeleteDivHut,

DeleteYeah it's no big deal. Now if I we see an increasing market and my net worth decreases significantly then I'll be worried. For now though the declines are just opportunities. I was pretty surprised though to see a rather insignificant decline considering the $5k that went to the car. Ahhh...the wonderful combination of a high income and a high savings rate.

Thanks for stopping by!

I have yet to calculate my net worth for the month of July. I don't have a good feeling, so I have been purposely putting it off.

ReplyDeleteMichelle,

DeleteWell go for it! The worst that can happen is that you find out where you stand and can make a change this month to improve your net worth.

Thanks for stopping by!