Coca-Cola Stock Analysis

I can't believe I hadn't posted this before because Coca-Cola (KO) is one of my core holdings that I wish I could add more to and I really enjoy their product. Coca-Cola closed trading on Friday, November 23rd at $37.93.

Company Background:

The Coca-Cola Company, a beverage company, engages in the manufacture, marketing, and sale of nonalcoholic beverages worldwide. The company primarily offers sparkling beverages and still beverages. Its sparkling beverages include nonalcoholic ready-to-drink beverages with carbonation, such as carbonated energy drinks, and carbonated waters and flavored waters. The company’s still beverages comprise nonalcoholic beverages without carbonation, such as noncarbonated waters, flavored waters and enhanced waters, noncarbonated energy drinks, juices and juice drinks, ready-to-drink teas and coffees, and sports drinks. It also provides flavoring ingredients, sweeteners, powders for purified water products, beverage ingredients, and fountain syrups. The Coca-Cola Company sells its products primarily under the Diet Coke, Fanta, Sprite, Coca-Cola Zero, vitaminwater, Powerade, Minute Maid, Simply, Georgia, and Del Valle brand names. The company offers its beverage products through company-owned or controlled bottling and distribution operators, as well as through independently owned bottling partners, distributors, wholesalers, and retailers.

DCF Valuation:

Analysts expect Coca-Cola to grow earnings 8.20% per year for the next five years and I've assumed they can continue to grow at 3.50% per year thereafter, slightly above the long term inflation rate. Running these numbers through a DCF analysis with a 10% discount rate yields a fair value price of $37.40. This means that at $37.93 the shares are overvalued by 1.4%.

Graham Number:

Over the last 12 months, Coca-Cola's EPS were $1.91 and it's current book value per share is $7.40. The Graham Number is calculated to be $17.83, which means it is currently overvalued by 112.7%.

Average High Dividend Yield:

Coca-Cola's average high dividend yield for the past 5 years is 3.49% and for the past 10 years is 3.21%. This gives target prices of $29.76 and $32.41 respectively based on the current annual dividend of $1.04. These are overvalued by 27.5% and 17.0%, respectively. I think the average high yield is going to be somewhere between the two for the next few years, but will eventually begin to creep higher. So far in 2012 the high yield mark hit 3.08% with a low yield of 2.56%.

Average Low PE Ratio:

KO's average low PE ratio for the past 5 years is 14.70 and for the past 10 years is 17.02. This corresponds to a price per share of $29.40 and $34.05 respectively based off the analyst estimate of $2.00 per share for the fiscal year ending in December. The 5 year and 10 year low PE price targets are overvalued by 29.0% and 11.4%, respectively. Coca-Cola has typically traded for a PE ratio that is a premium to the market as a whole, so the 10 year average low PE ratio of 17 should be fairly typical of what you'll see KO trade for on a PE basis.

Average Low P/S Ratio:

Coca-Cola's average low PS ratio for the past 5 years is 3.1 and for the past 10 years is 3.6. This corresponds to a price per share of $32.70 and $37.94 respectively based off the analyst estimate for revenue growth from FY 2011 to FY 2012. Their current PS ratio is 3.52. The 5 year and 10 year low PS price targets are overvalued by 16.0% and fairly valued.

Dividend Discount Model:

For the DDM I assumed that KO will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, 5 or 10 year growth rates. In this case that would be 8.24%. After that I assumed they can continue to raise dividends for the next 5 years at 75% of 8.24%, or 6.19%, and by 3.50% in perpetuity. The dividend growth rates are based off fiscal year increases and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on this, Coca-Cola is worth $20.96 meaning it's overvalued by 80.9%.

PE Ratios:

Coca-Cola's trailing PE is 19.86 and it's forward PE is 17.32. The PE3 based on the average earnings for the last 3 years is 19.45. I like to see the PE3 be less than 15 which KO is currently well above.at it's current price. Compared to it's industry, KO seems to be overvalued versus DPS (15.33) and PEP (18.69). Against the industry as a whole, Coca-Cola is undervalued with the industry carrying a PE ratio of 22.62. All industry comparisons are on a TTM EPS basis.

Fundamentals:

KO's gross margin for FY 2010 and FY 2011 were 68.0% and 65.1% respectively. They have averaged a 68.6% gross profit margin since 2001 with a low of 65.1% in FY 2011. Their net income margin for the same years were 33.6% and 18.4% respectively. Since 2001 their net income margin has averaged 21.6% with a low of 18.2%. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. Coca-Cola passes both with flying colors with a gross margin substantially higher than 60% and more than doubling my 10% target. Since every industry is different and allows for different margins it's useful to compare Coca-Cola's margins to it's competitors. KO captured 115.4% of the gross margin for the industry and 123.5% of the net profit margin for in fiscal year 2011. These are both very promising because it shows that there is a high demand for their product and that cost increases in their materials can be passed to the consumer without jeopardizing the profits of the company. Their cash-to-debt ratio for the same years were 0.71 and 0.52. This is the only real blemish from a fundamentals perspective.

Share Buyback:

Coca-Cola's shares outstanding have decreased every year since 2001. They have decreased on average 0.85% of the shares outstanding since FY 2001 ended and a total of 8.98% of the shares outstanding at the end of FY 2001. This is another way that management can essentially return cash to shareholders and it's great that they are siding with their investors.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Coca-Cola is a dividend champion and recently hit 50 consecutive years of dividend increases. Their current annual dividend sits at $1.04 for a current yield of 2.74%. KO's annual increase for the last 1, 3, 5 and 10 years have been 10.64%, 8.24%, 8.87% and 10.03%. These numbers are different from the actual quarterly increases since these are based off the dividends paid out during each fiscal year. Coca-Cola has one more payout this year with an ex-div date of November 28th and will pay out in December. Their next dividend increase should come with the April 2013 payout. Their payout ratio has increased slightly since 2001 but has averaged 51.60%. The highest payout based off earnings was 60.80% in FY 2008. Considering they've been growing the dividend at a 10% annual increase over the last 10 years, it's very nice to see that the payout ratio hasn't increased at the same rate.

Their FCF per share is one of the biggest surprises for me while researching the company. They've only had one year with negative FCF but have only once had a FCF payout ratio less than 100%. I would like to see the FCF payout ratio come down because it will show that management is able to have more cushion for down years.

Return on Equity and Return on Capital Invested:

Coca-Cola's ROE has averaged 30.65% since 2001 with a low of 27.10% and a high of 34.20%. Their ROCI is at a nice level as well averaging 25.90% since 2001 with a low of 18.90% and a high of 30.90%. For both ROE and ROCI I don't necessarily look for any absolute values rather I like to see stable to increasing levels over the long term.

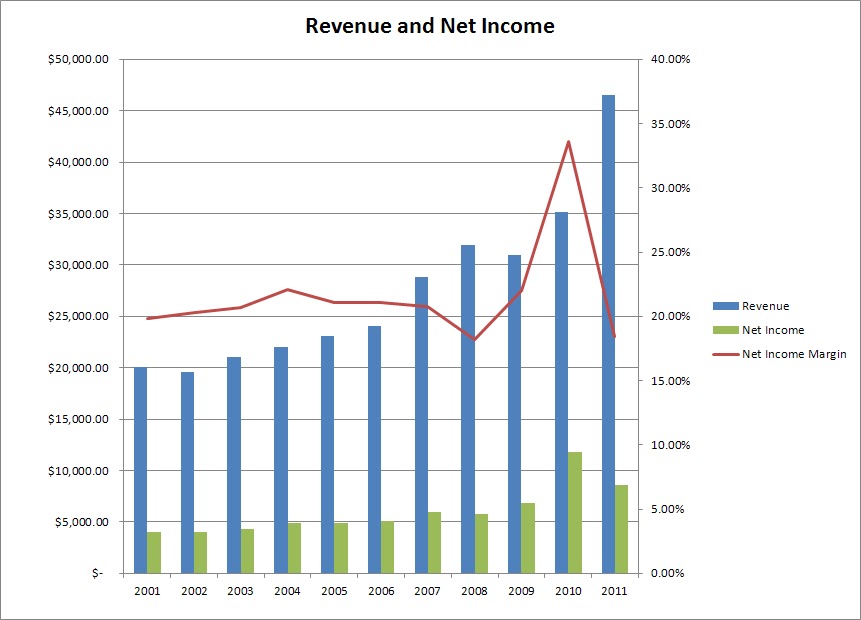

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how Coca-Cola has done on that front. Their revenue growth since 2001 has been a respectable 8.76% per year but their net income has been growing at an 7.98% rate since 2001. Since revenue has grown faster than net income their net income margin has retracted slightly. Revenue has grown every year but two since 2001 with the down years being 2002 and 2009. Both negative year-over-year comparison's saw revenue come in just slightly down with only 2.6% and 3.0% declines.

Tangible Book Value:

Coca-Cola's tangible book value per share leaves much to be desired with it decreasing between 2001 and 2011. The first half of the period saw great growth and even up through 2009 it had increased a total of 47%. However in 2010 it took a big hit and was essentially flat in 2011. The decrease is most likely to the purchase of bottling segment to control more of the operations. This is something I'll be looking for when the FY 2012 annual report is released next year.

Forecast:

The chart shows the historical prices since 2001 and the forecast based on the average PE ratios and the expected EPS values. I have also included a forecast based off a PE ratio that is only 75% of the average low PE ratio for the previous 5 years and 10 years whichever is least. Since I think the 10 year average low PE of 17 is going to be more typical for KO I'll use that number. I like to the look to buy at the 75% Low PE price or lower to provide for additional margin of safety. In this case the target low PE is 17.02 and the 0.75 * PE is12.77 . This corresponds to a entry price of $34.05 and $19.15 based off the expected earnings for FY 2012 of $2.00. Currently Coca-Cola is trading at a $1.50 discount and $18.78 premium to the target prices, respectively. I don't think you'll see KO trading for a sub 13 PE ratio anytime soon. Coca-Cola is 36% higher than the low PE price based on the range of valuations.

Conclusion:

The average of all the valuation models gives a fair value $29.22 which means that Coca-Cola is currently trading at a 29.8% premium to the average fair value. I've also calculated the fair value with the highest and lowest valuation methods thrown out. In this case, the DCF and Graham Number valuations are thrown out and the new average is $30.03. KO is trading at a 26.3% premium to this price as well.

Overall I would say that Coca-Cola is currently a hold but if the price can pull back with the market over European or Middle East concerns or our own Fiscal Cliff mess then I would be ready to pick up some more shares around the $34 level. That would be a 10% drop from current prices. The 3.00% yield level is at a price of $34.67 and the 3.25% yield is at $32.00. With a company as large and strong and stable as Coca-Cola you have to be willing to pay a premium to pick up shares and that shows in their historical averages.

What do you think about Coca-Cola as a DG investment at today's prices?

Company Background:

The Coca-Cola Company, a beverage company, engages in the manufacture, marketing, and sale of nonalcoholic beverages worldwide. The company primarily offers sparkling beverages and still beverages. Its sparkling beverages include nonalcoholic ready-to-drink beverages with carbonation, such as carbonated energy drinks, and carbonated waters and flavored waters. The company’s still beverages comprise nonalcoholic beverages without carbonation, such as noncarbonated waters, flavored waters and enhanced waters, noncarbonated energy drinks, juices and juice drinks, ready-to-drink teas and coffees, and sports drinks. It also provides flavoring ingredients, sweeteners, powders for purified water products, beverage ingredients, and fountain syrups. The Coca-Cola Company sells its products primarily under the Diet Coke, Fanta, Sprite, Coca-Cola Zero, vitaminwater, Powerade, Minute Maid, Simply, Georgia, and Del Valle brand names. The company offers its beverage products through company-owned or controlled bottling and distribution operators, as well as through independently owned bottling partners, distributors, wholesalers, and retailers.

DCF Valuation:

Analysts expect Coca-Cola to grow earnings 8.20% per year for the next five years and I've assumed they can continue to grow at 3.50% per year thereafter, slightly above the long term inflation rate. Running these numbers through a DCF analysis with a 10% discount rate yields a fair value price of $37.40. This means that at $37.93 the shares are overvalued by 1.4%.

Graham Number:

Over the last 12 months, Coca-Cola's EPS were $1.91 and it's current book value per share is $7.40. The Graham Number is calculated to be $17.83, which means it is currently overvalued by 112.7%.

Average High Dividend Yield:

Coca-Cola's average high dividend yield for the past 5 years is 3.49% and for the past 10 years is 3.21%. This gives target prices of $29.76 and $32.41 respectively based on the current annual dividend of $1.04. These are overvalued by 27.5% and 17.0%, respectively. I think the average high yield is going to be somewhere between the two for the next few years, but will eventually begin to creep higher. So far in 2012 the high yield mark hit 3.08% with a low yield of 2.56%.

KO's average low PE ratio for the past 5 years is 14.70 and for the past 10 years is 17.02. This corresponds to a price per share of $29.40 and $34.05 respectively based off the analyst estimate of $2.00 per share for the fiscal year ending in December. The 5 year and 10 year low PE price targets are overvalued by 29.0% and 11.4%, respectively. Coca-Cola has typically traded for a PE ratio that is a premium to the market as a whole, so the 10 year average low PE ratio of 17 should be fairly typical of what you'll see KO trade for on a PE basis.

Average Low P/S Ratio:

Coca-Cola's average low PS ratio for the past 5 years is 3.1 and for the past 10 years is 3.6. This corresponds to a price per share of $32.70 and $37.94 respectively based off the analyst estimate for revenue growth from FY 2011 to FY 2012. Their current PS ratio is 3.52. The 5 year and 10 year low PS price targets are overvalued by 16.0% and fairly valued.

Dividend Discount Model:

For the DDM I assumed that KO will be able to grow dividends for the next 5 years at the minimum of 15% or the lowest of the 1, 3, 5 or 10 year growth rates. In this case that would be 8.24%. After that I assumed they can continue to raise dividends for the next 5 years at 75% of 8.24%, or 6.19%, and by 3.50% in perpetuity. The dividend growth rates are based off fiscal year increases and don't necessarily correspond to quarter over quarter increases. To calculate the value I used a discount rate of 10%. Based on this, Coca-Cola is worth $20.96 meaning it's overvalued by 80.9%.

PE Ratios:

Coca-Cola's trailing PE is 19.86 and it's forward PE is 17.32. The PE3 based on the average earnings for the last 3 years is 19.45. I like to see the PE3 be less than 15 which KO is currently well above.at it's current price. Compared to it's industry, KO seems to be overvalued versus DPS (15.33) and PEP (18.69). Against the industry as a whole, Coca-Cola is undervalued with the industry carrying a PE ratio of 22.62. All industry comparisons are on a TTM EPS basis.

Fundamentals:

KO's gross margin for FY 2010 and FY 2011 were 68.0% and 65.1% respectively. They have averaged a 68.6% gross profit margin since 2001 with a low of 65.1% in FY 2011. Their net income margin for the same years were 33.6% and 18.4% respectively. Since 2001 their net income margin has averaged 21.6% with a low of 18.2%. I typically like to see gross margins greater than 60% and at least higher than 40% with net income margins being 10% and at least 7%. Coca-Cola passes both with flying colors with a gross margin substantially higher than 60% and more than doubling my 10% target. Since every industry is different and allows for different margins it's useful to compare Coca-Cola's margins to it's competitors. KO captured 115.4% of the gross margin for the industry and 123.5% of the net profit margin for in fiscal year 2011. These are both very promising because it shows that there is a high demand for their product and that cost increases in their materials can be passed to the consumer without jeopardizing the profits of the company. Their cash-to-debt ratio for the same years were 0.71 and 0.52. This is the only real blemish from a fundamentals perspective.

Share Buyback:

Coca-Cola's shares outstanding have decreased every year since 2001. They have decreased on average 0.85% of the shares outstanding since FY 2001 ended and a total of 8.98% of the shares outstanding at the end of FY 2001. This is another way that management can essentially return cash to shareholders and it's great that they are siding with their investors.

A negative number for the % change value means shares were bought back by the company and a positive value means the shares outstanding increased.

Dividend Analysis:

Coca-Cola is a dividend champion and recently hit 50 consecutive years of dividend increases. Their current annual dividend sits at $1.04 for a current yield of 2.74%. KO's annual increase for the last 1, 3, 5 and 10 years have been 10.64%, 8.24%, 8.87% and 10.03%. These numbers are different from the actual quarterly increases since these are based off the dividends paid out during each fiscal year. Coca-Cola has one more payout this year with an ex-div date of November 28th and will pay out in December. Their next dividend increase should come with the April 2013 payout. Their payout ratio has increased slightly since 2001 but has averaged 51.60%. The highest payout based off earnings was 60.80% in FY 2008. Considering they've been growing the dividend at a 10% annual increase over the last 10 years, it's very nice to see that the payout ratio hasn't increased at the same rate.

Their FCF per share is one of the biggest surprises for me while researching the company. They've only had one year with negative FCF but have only once had a FCF payout ratio less than 100%. I would like to see the FCF payout ratio come down because it will show that management is able to have more cushion for down years.

Return on Equity and Return on Capital Invested:

Coca-Cola's ROE has averaged 30.65% since 2001 with a low of 27.10% and a high of 34.20%. Their ROCI is at a nice level as well averaging 25.90% since 2001 with a low of 18.90% and a high of 30.90%. For both ROE and ROCI I don't necessarily look for any absolute values rather I like to see stable to increasing levels over the long term.

Revenue and Net Income:

Since the basis of dividend growth is revenue and net income growth, we'll now look at how Coca-Cola has done on that front. Their revenue growth since 2001 has been a respectable 8.76% per year but their net income has been growing at an 7.98% rate since 2001. Since revenue has grown faster than net income their net income margin has retracted slightly. Revenue has grown every year but two since 2001 with the down years being 2002 and 2009. Both negative year-over-year comparison's saw revenue come in just slightly down with only 2.6% and 3.0% declines.

Tangible Book Value:

Coca-Cola's tangible book value per share leaves much to be desired with it decreasing between 2001 and 2011. The first half of the period saw great growth and even up through 2009 it had increased a total of 47%. However in 2010 it took a big hit and was essentially flat in 2011. The decrease is most likely to the purchase of bottling segment to control more of the operations. This is something I'll be looking for when the FY 2012 annual report is released next year.

Forecast:

Conclusion:

The average of all the valuation models gives a fair value $29.22 which means that Coca-Cola is currently trading at a 29.8% premium to the average fair value. I've also calculated the fair value with the highest and lowest valuation methods thrown out. In this case, the DCF and Graham Number valuations are thrown out and the new average is $30.03. KO is trading at a 26.3% premium to this price as well.

Overall I would say that Coca-Cola is currently a hold but if the price can pull back with the market over European or Middle East concerns or our own Fiscal Cliff mess then I would be ready to pick up some more shares around the $34 level. That would be a 10% drop from current prices. The 3.00% yield level is at a price of $34.67 and the 3.25% yield is at $32.00. With a company as large and strong and stable as Coca-Cola you have to be willing to pay a premium to pick up shares and that shows in their historical averages.

What do you think about Coca-Cola as a DG investment at today's prices?

PIP,

ReplyDeleteOutstanding analysis. Much appreciated!

I'd love to buy more KO, but simply cannot do so at current prices. I would be buying on a 10% dip as well, right alongside yourself. I doubt we'll be seeing $30 a share on a high quality company like KO anytime soon, but would be more than willing to buy it in that $33-34 range.

KO is probably that "If I could only own one stock" pick for me. It's quite ironic, in this case, that it's one of my smaller holdings. Valuation is paramount.

Best wishes!

DM,

DeleteKO is one company I've always tried to get more invested in but it's never come down in price enough since I first purchased it. Luckily I made a pretty big investment in them at the time for a cost basis of $33.72 and I'd love to pick up some more shares around that price. I agree, less than $30 is very optimistic and probably won't happen but the low $30's is realistic.

I truly believe that KO will be around for years and years and it helps that I really enjoy their products.

Thanks for stopping by!

I think coca cola is an excellent company. The one issue that I would have with this company is their concentration in the beverage business. Most companies will become more diverse as they become larger over time coke has remained soley in the beverage business. The company is divided into two groups a marketing and promotional arm and the bottling division.

ReplyDeleteThere's something to be said though about knowing what your good at and sticking with that. Diversifying into other ventures, even if it's related like the food/snack business, isn't always the best thing for a company. There's plenty of examples of companies that diversified away from their core just because they could and failed miserably.

DeleteThanks for stopping by!

Waiting for $30 prices gets you easily in a situation where the stock price hits $40...and $50...

ReplyDelete