Net Worth Update - July 2013

While cash flow is more important when it comes to financial independence, it's still good to look at the balance sheet too, which is why I provide these net worth updates. The markets surged higher again through July which when coupled with a very good savings rate helped to push my net worth up over $10k last month after a very disappointing June. I had a little over $900 in combined 401k contributions, $670 in ESPP withholdings, and over $5,850 in after tax savings from my income. The rest of the change was due to market changes and dividends.

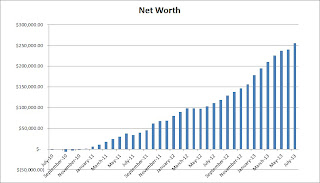

Current Assets: $272,916.54

Curent Liquid Assets: $148,148.36

Current Debts: -$16,975.43

Net Worth: $255,941.11

As I mentioned above things got back on track after a disappointing June. The increase came in at $15,827.72 and was good for a 6.59% increase from June's tally. July ended up being my third highest month ever. The best part is that I would say that I met my original goal of a $100k increase in my net worth for the year. Although technically I haven't since I'm $11.02 short of that target, but it's only been 7 months so I'll pretty much call it complete. I'm still short of my new revised goal of reaching $286k. Since my wife and I are in the process of purchasing a house the net worth is going to get a little skewed. I'm thinking of calculating my net worth with the house completely excluded and then also including both the debt and equity portions of the house. Any thoughts on the best way to account for a primary residence?

My after-tax savings rate for July ended up at 79.71% which was a bit disappointing but it did come back up from June. I'm now averaging 82.14% through the July which is phenomenal. This is currently ahead of my 80%+ savings rate goal. This is only savings from my net income that actually hits my checking account. However, I do have another 8% after tax being withheld to purchase shares through the employee stock purchase plan provided by my employer.

My non-retirement accounts net worth increased a very solid 0.48 years to 8.49.It's pretty amazing to see that with just my liquid assets I could cover my minimum expenses for almost 8.5 years, excluding inflation. It would have been higher had my spending/budgeting gone better but the expenses weren't anything too outrageous. Sadly this is going to take a hit with a big chunk of cash going towards the down-payment for the house. I'll still do my best though to rebuild my liquid assets as quickly as possible.

I've updated my Progress page to reflect July's changes.

How was your July? Did you do better or worse than you expected this month?

Current Assets: $272,916.54

Curent Liquid Assets: $148,148.36

Current Debts: -$16,975.43

Net Worth: $255,941.11

As I mentioned above things got back on track after a disappointing June. The increase came in at $15,827.72 and was good for a 6.59% increase from June's tally. July ended up being my third highest month ever. The best part is that I would say that I met my original goal of a $100k increase in my net worth for the year. Although technically I haven't since I'm $11.02 short of that target, but it's only been 7 months so I'll pretty much call it complete. I'm still short of my new revised goal of reaching $286k. Since my wife and I are in the process of purchasing a house the net worth is going to get a little skewed. I'm thinking of calculating my net worth with the house completely excluded and then also including both the debt and equity portions of the house. Any thoughts on the best way to account for a primary residence?

My after-tax savings rate for July ended up at 79.71% which was a bit disappointing but it did come back up from June. I'm now averaging 82.14% through the July which is phenomenal. This is currently ahead of my 80%+ savings rate goal. This is only savings from my net income that actually hits my checking account. However, I do have another 8% after tax being withheld to purchase shares through the employee stock purchase plan provided by my employer.

My non-retirement accounts net worth increased a very solid 0.48 years to 8.49.It's pretty amazing to see that with just my liquid assets I could cover my minimum expenses for almost 8.5 years, excluding inflation. It would have been higher had my spending/budgeting gone better but the expenses weren't anything too outrageous. Sadly this is going to take a hit with a big chunk of cash going towards the down-payment for the house. I'll still do my best though to rebuild my liquid assets as quickly as possible.

How was your July? Did you do better or worse than you expected this month?

Good point on the challenge of including primary residence as part of net worth. To date, I haven't been reporting out my housing equity on primary residence as I assume I'll have to move somewhere else if I sell (though I guess I could always go back to renting).

ReplyDeleteIf you are going to include it, I'd do net equity.

Integrator,

DeleteIf I do include our primary residence then it will definitely be net of the loan. Although I wonder if it's best to use the appraised value and not the actual agreed upon purchase price. I think I'll probably just go about reporting my net worth with and without the house to show both situations.

Thanks for stopping by!

It is fair to include equity in your primary home in your net worth. But best to use a low/conservative number. Since it is a new purchase, I'd be surprised if the appraised price and the sale price were much different. In any case, use the lower of the two and subtract the remaining mortgage balance. Then round down and lop off a several thousand (because if you had to sell today, you are unlikely to recoup full amount of equity due to transaction costs). Best of luck!

DeleteKerim,

DeleteI think including it's perfectly fine as long as you realize that it's not the most liquid of assets. Don't count on being able to tap that equity in a dire situation, or quickly for that matter. I think I'm going to report my net worth including the house, so net equity, and also excluding the house just to give a better picture.

Thanks for stopping by!

Sounds like you had a fantastic month too! Plus you nudged your way over the quarter million mark in net worth - buy yourself some more dividend paying stocks to celebrate!

ReplyDeleteKeep the momentum up!

Michael

Dividend Tactics,

DeleteIt was a great month and actually this quarter is going to be awesome. If it weren't for the pending house purchase I would have another $45k to plop down on some dividend growth stocks. That'd be $1,350 in annual income assuming a 3.00% average yield.

I was very surprised to see this much progress get made towards my net worth. I hit a $100k increase in just 7 months. Well, I'm still $11 short of my goal, but I'd say that's winning right there.

Keep up the good work yourself! I can't wait to get back to picking up some solid dividend growth stocks.

Thanks for stopping by!

Kicking butt. Well done.

ReplyDeleteMark

Mark,

DeleteThanks and you're doing a great job yourself. Liked the Why dividends matter post.

Thanks for stopping by!

Impressive journey from negative net worth in 2010 to $250,000 today. At that rate, you should hit $1 million by or before 2020. Best wishes on your journey. You can turn that into some passive income. At the very least you can get the measly 1% return savings accounts are providing today.

ReplyDeleteFree Money Minute,

DeleteI've worked really hard to save as much as possible from my after-tax income. A high savings rate with consistent investing is the key to building wealth and passive income. I hope to hit $1M before 2020, but my wife and I are planning on kids in the next year or two and they have a way of eating away at your savings rate, both literally and figuratively. If I can still save 50% of my after tax income with kids then we should still reach $1M by then. Until I reach that point though I'll just keep investing in some of the best companies in the world.

Thanks for stopping by!