Income Update - October 2012

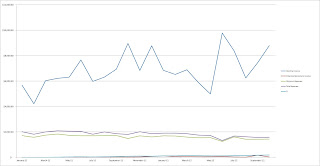

October's spending was right in line with August and September which is good because it hasn't increased but it's still higher that where I would like for it to be. I was hoping to be able to get my spending down to the $1,300 mark but I just don't see that happening. I know if I can cut back on my restaurant spending that I'll be able to make some pretty big strides in the reduction because for the most part my restaurant and grocery spending is the largest portion of my spending that I realistically have room to cut from. My minimum expenses for October ended the month at $1,440.69 which brought my average for 2012 down to $1,519.96. My average total monthly expenses for October ended up right in line with September at $1,578.41. This brought my average monthly total expenditures for 2012 down to $1,691.36. My PRI for October was a pretty disappointing $25.47 which covered only 1.77% of my minimum expenses. This wasn't a total surprise because I knew that October would be a very light month for dividends. However, my FI made yet another move higher totaling $185.98 for the month based on the yield on the 30 year US treasury bond of 2.88%. This covers 12.91% of my minimum expenses for the month. October was a great month from income bringing in my second highest monthly total for the year.

*Minimum Expenses are only the expenses related to rent, utilities, car, food, minimum payment on debt and other necessities. In other words, the required amount of replacement income I would need for financial independence.

*Total Expenses are the total monthly outflow of money.

*Potential Retirement Income is income received from dividends, interest, cash back from credit card purchases and any other source of income not related to my job.

*FI is my liquid assets invested at the 30 year treasury bond yield at the end of each month divided by 12 to get monthly income.

*Minimum Expenses are only the expenses related to rent, utilities, car, food, minimum payment on debt and other necessities. In other words, the required amount of replacement income I would need for financial independence.

*Total Expenses are the total monthly outflow of money.

*Potential Retirement Income is income received from dividends, interest, cash back from credit card purchases and any other source of income not related to my job.

*FI is my liquid assets invested at the 30 year treasury bond yield at the end of each month divided by 12 to get monthly income.

| Category | Amount |

|---|---|

| Paycheck | $7,779.65 |

| Expense Check | $978.39 |

| TOTAL | $8,758.04 |

| Category | Budgeted Amount | Actual Amount | Subtotal |

|---|---|---|---|

| Rent | $480.00 | $480.00 | |

| Utilities | $270.00 | $217.06 | |

| Gas | $175.00 | $120.74 | |

| Car Insurance | $80.00 | $80.00 | |

| Groceries | $250.00 | $228.19 | |

| Restaurants | $130.00 | $126.47 | |

| Entertainment | $30.00 | $42.50 | |

| Cell Phone | $75.00 | $75.00 | |

| Other | $49.06 | $49.06 | |

| Miscellaneous | $50.00 | $84.39 | |

| Gifts | $0.00 | $0.00 | |

| EXPENSES SUBTOTAL | $1,503.41 | ||

| SAVINGS | |||

| Trip | $225.00 | $225.00 | |

| Roth IRA | $725.00 | $725.00 | |

| Emergency Fund | $93.98 | $179.63 | |

| Gifts | $50.00 | $50.00 | |

| FI savings | $6,000.00 | $6,000.00 | |

| Car Maint/Repair | $75.00 | $75.00 | |

| SAVINGS SUBTOTAL | $7,254.63 | ||

| TOTAL | $8,758.04 |

It looks like you had a solid month in terms of income and savings. Good job!

ReplyDeleteDGM,

DeleteIt was a great month. I'm looking forward to see how November ends since my income will be about the same amount as October.

Thanks for stopping by!

That's a huge month. Great job. You're income is off the charts. I can only dream of getting paychecks like that. Awesome!

ReplyDeleteGood job not letting your lifestyle inflate with the income. That's tough to accomplish on a long-term basis.

Keep up the great work!

Best wishes.

DM,

DeleteI'm definitely blessed to have an income as high as it is. There's times where I want to just go and blow a bunch of money on something but the urge passes pretty quickly. I'm away from home for work so it makes it easier to not go and buy any big boy toys (boats, ATV's...) since I'm not home enough to even get use out of them. The biggest thing that keeps me from inflating my lifestyle is that I really want early FI and with the income and amount that I can save I can be set up to still have a solid income from my DG investments and be free to do as I please.

Thanks for stopping by!

wow, massive income, and even better savings rate! If you keep having months like this, you'll reach early FI in no time!

ReplyDeleteI look forward to following your progress. You're doing great!

FI,

DeleteThat's the plan. I wish I had stumbled upon the job I have now right after graduating from college. I could retire in another two years probably. That'd be retiring at 30. But 40 is still earlier than most people so I guess I can't complain too much.

Thanks for stopping by!